Capital Southwest Corporation (NASDAQ:CSWC) currently trades at roughly a price-to-book ratio of 1.40x, which translates to a premium of roughly 32% above its book value of $16.75 per share. For a business development company whose job is to lend money and pass income to shareholders, that gap depends on the durability and level of the income stream.

How CSWC Generates Income

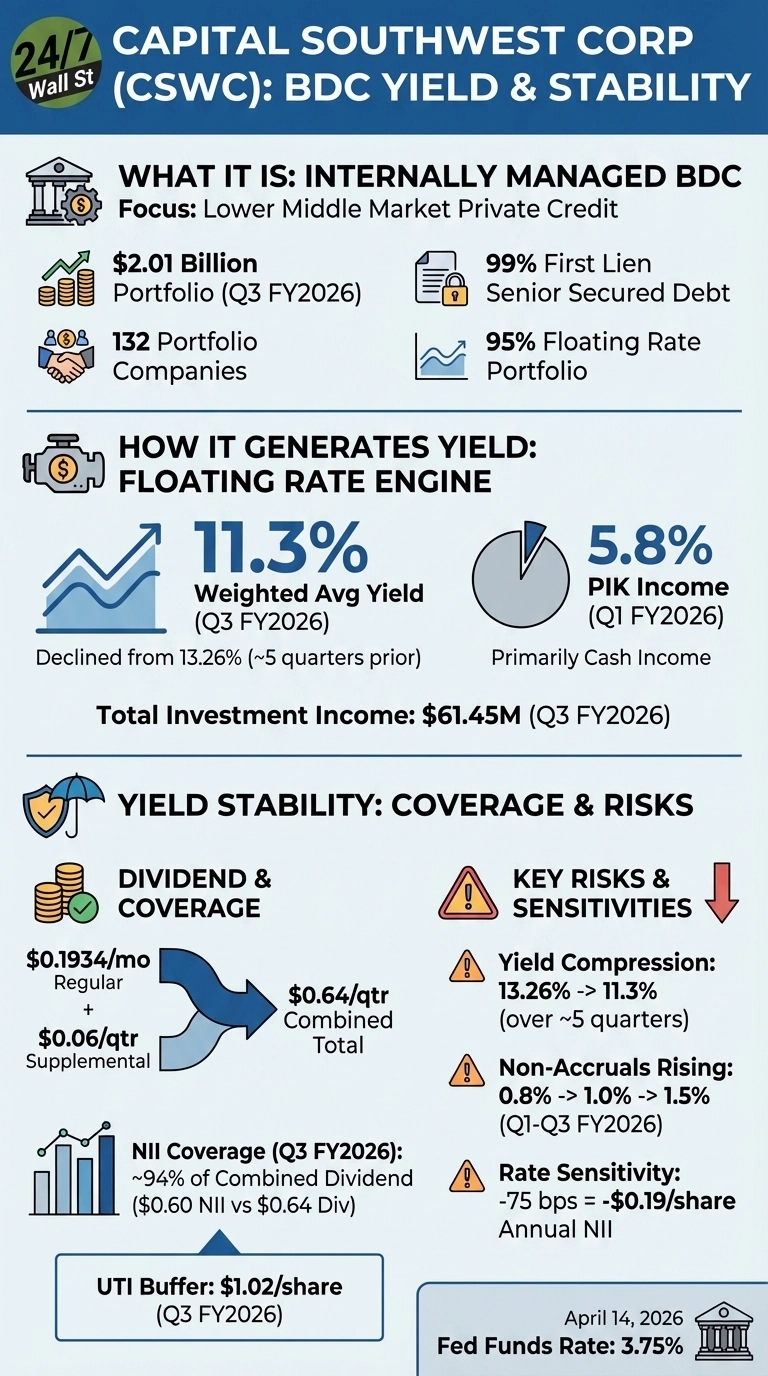

Capital Southwest is an internally managed BDC that provides loans to lower-middle-market companies and earns interest on those loans. It borrows at lower rates, lends at higher rates, and passes the spread through to shareholders as income. Its $2.01 billion investment portfolio is spread across 132 companies, with 99% in first-lien senior secured debt and 95% in floating-rate loans. The floating-rate structure allows income to rise when interest rates are high and fall when rates decline.

NII Coverage Relative to the Combined Payout

Pre-tax net investment income per share has been running between $0.59 and $0.61 in recent quarters. Against the combined $0.64 quarterly payout, overall NII coverage sits at roughly 94%. The regular monthly dividend is solidly covered at about 104% on a trailing twelve-month basis, while the supplemental portion relies on the company’s undistributed taxable income buffer.

That buffer currently stands at $1.02 per share, up from $0.79 per share at the end of FY2025. It provides a healthy cushion, covering approximately 17 quarters of the current supplemental dividend. This structure allows CSWC to maintain its payout even when quarterly NII slightly lags the total distribution.

Rate Environment Is the Core Risk

The Fed funds rate currently sits at 3.75%, down 75 basis points from 4.5% a year ago. The compression is reflected in CSWC’s portfolio yield, which has declined from 13.26% roughly five quarters ago to 11.3% in Q3 FY2026. Each 75-basis-point further decline in the rate would reduce annual NII by approximately $11.1 million, or $0.19 per share.

A 200 basis-point decline from current levels would reduce annual NII by roughly $31.9 million, or $0.56 per share, eliminating NII coverage entirely and accelerating the drawdown of the UTI buffer. The Fed has held rates steady since December 2025, providing near-term stability, but the direction over the past year has been downward.

Credit Quality Has Slipped

Non-accruals have risen steadily from 0.8% of the portfolio in Q1 FY2026 to 1.0% in Q2 and 1.5% in Q3. The level has nearly doubled over the past three quarters.

On a positive note, only 5.8% of total investment income comes from PIK interest, which means the vast majority of borrowers are still paying cash. Portfolio leverage remains moderate, with a weighted-average debt-to-EBITDA of 3.4x across the portfolio companies.

Valuation at a 1.4x Price-to-Book Multiple

Capital Southwest Corporation currently trades at roughly a 1.4x price-to-book ratio, with the stock up about 37% over the past year. The company has consistently raised equity through its ATM program at healthy premiums to NAV, most recently at 127% of NAV in Q3 FY2026. These issuances are accretive to existing shareholders. Its internally managed structure keeps operating expenses lower than those of externally managed peers, supporting a higher valuation multiple.

Analyst consensus points to a price target of $24.40, modestly above current levels, with four analysts rating the stock bullish and three neutral. Some DCF models cited in research suggest a fair value closer to $17.02, meaning the current premium largely reflects strong income expectations rather than book value alone.

CSWC has also expanded its reach through two recent joint ventures, including a $100 million partnership with Trinity Capital focused on first-out senior secured debt. These off-balance-sheet structures increase origination capacity without adding leverage to CSWC’s own balance sheet.

Rate Sensitivity and Dividend Coverage Outlook

The regular monthly dividend is currently well covered by net investment income at today’s interest rate levels. The supplemental dividend, however, depends on the company’s $1.02-per-share undistributed taxable income (UTI) buffer, which is real but finite.

The biggest risk going forward is further Fed rate cuts. The portfolio yield has already declined by nearly 200 basis points from its peak, and every additional cut puts additional pressure on coverage.

The main variables to watch are upcoming Fed decisions, credit quality trends across the portfolio, and how origination volume compares with repayments. While the UTI buffer provides a cushion for the supplemental dividend, the long-term health of the regular dividend will depend on maintaining adequate NII in a lower-rate environment.

Contact [email protected] for any questions or corrections.