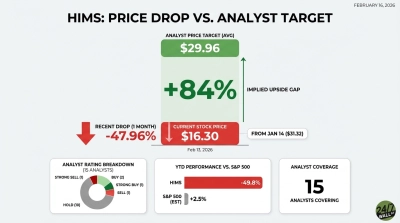

Hims & Hers Health (NYSE:HIMS) just got a fresh look from Bank of America, which raised its price target on the stock to $25 from $21 while maintaining a Neutral rating. The catalyst: the FDA took a procedural step to begin evaluating several wellness peptides that are currently restricted under FDA guidance. It’s an early-stage development, but one that could open meaningful new revenue doors for the telehealth platform.

BofA frames this as “an initial small step and not a final approval or bulks-list addition.” Still, the analysts view the move as positive for Hims & Hers because it creates optionality around new revenue streams and could allow the company to repurpose existing GLP-1 manufacturing capacity toward other peptides.

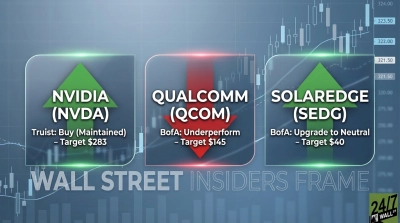

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| HIMS | Hims & Hers Health | Bank of America | Price Target Raised | Neutral | Neutral | $21 | $25 |

The Analyst’s Case

BofA’s revised target reflects the incremental optionality the FDA’s peptide review creates for Hims & Hers. The company could repurpose GLP-1 capacity toward other peptides, which aligns with its pipeline ambitions around longevity, sleep, and preventative medicine. That’s a meaningful operational advantage if the regulatory door opens wider.

The upgrade arrives at an interesting moment for HIMS stock. Shares have surged 29% over the past week, recovering from a rough stretch that saw HIMS stock fall 25% year-to-date entering into mid-April. The stock trades near the new $25 target, so BofA’s Neutral rating signals this is a “watch and wait” call rather than a chase.

Company Snapshot

Hims & Hers operates a multi-specialty telehealth platform connecting consumers with licensed healthcare professionals. The company ended 2025 with over 2.5 million subscribers, up 13% year-over-year, generating $83 per average subscriber per month, up 11% year-over-year.

Full-year 2025 revenue came in at $2.35 billion, up 59% year-over-year, with management guiding for $2.7 billion to $2.9 billion in 2026 revenue. Hims & Hers CEO Andrew Dudum stated, “More than 2.5 million subscribers now rely on us for a healthcare experience that is both accessible and deeply personal.”

Why the Move Matters Now

Hims & Hers has been actively building peptide manufacturing capabilities. The company operates a California-based peptide manufacturing facility and has a longevity specialty planned featuring peptides, coenzymes, and GLP/GIP treatments. If the FDA’s review progresses, Hims & Hers is positioned to move quickly. This is why growth stocks finding analyst support tend to reward investors who pay attention to the regulatory pipeline, not just quarterly numbers.

The risks remain real, however. Hims & Hers’ 2026 guidance assumes continued compounded semaglutide access, and gross margins have compressed roughly 500 basis points year-over-year in recent quarters. Free cash flow turned negative in Q4 2025 at -$2.57 million, a detail long-term investors shouldn’t overlook.

What It Means for Your Portfolio

BofA’s price target raise acknowledges a real emerging catalyst, but the Neutral rating signals the risk-reward is roughly balanced at current levels. HIMS stock trades near the new $25 target, so near-term upside from this call is limited.

If you believe the FDA’s peptide review accelerates and Hims & Hers successfully diversifies beyond GLP-1 compounding, the longer-term case becomes more compelling, especially given the company’s 2030 revenue target of at least $6.5 billion. However, if regulatory headwinds intensify or margin pressure deepens, the current valuation leaves little cushion. Watch for whether the FDA’s peptide evaluation advances from procedural review to formal approval consideration.

Contact [email protected] for any questions or corrections.