Seagate Technology (NASDAQ:STX | STX Price Prediction) is the name lighting up screens this morning after a 17.13% earnings beat sent shares up roughly 13% after the close. The setup deserves a closer look.

The Seagate story has the shape every contrarian recognizes. The stock is up 613.7% over the past year and 110.63% year to date, with a 52.35% move in the last month alone. The fundamentals are real: revenue grew 44.07% year over year, non-GAAP gross margin expanded from 36.2% to 47.0%, and free cash flow hit $953 million. The trouble is what those numbers describe: a cyclical hard-drive maker at the absolute top of its pricing cycle, with build-to-order capacity already committed through mid-2026 and a P/E of 67.

The analyst consensus target sits at $549.16, below the current $579.03. Insiders have logged 123 recent transactions with net selling. Sentiment on r/wallstreetbets is registering 88 out of 100. When the crowd is that bullish on a commoditized HDD supplier riding one AI tailwind, the asymmetry has flipped against new buyers.

The AI Play That Actually Compounds

Redirect attention to Alphabet (NASDAQ:GOOGL), the AI infrastructure builder Seagate is selling parts to. Three reasons this is the better seat.

First, full-stack capture versus single-input exposure. Google sells the models, the cloud, the ads, and the chips. In Q4, Google Cloud revenue grew 48% year over year to $17.66 billion, with operating income more than doubling to $5.31 billion. Search delivered $63.07 billion, up 17%. Seagate captures one commoditized input. Alphabet captures the value chain.

Second, scale that funds itself. Alphabet crossed $400 billion in annual revenue for the first time, generated $164.7 billion in operating cash flow for the year, and is guiding to $175 billion to $185 billion in 2026 capex. That capex is what underwrites the storage demand Seagate is celebrating. Owning the customer is structurally better than owning the supplier.

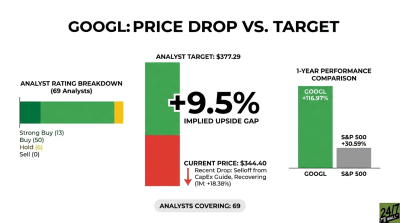

Third, multiple AI monetization paths at a defensible multiple. Gemini’s app sits at 750 million-plus monthly active users, processing 10 billion-plus tokens per minute through the API. YouTube clears $60 billion annually, Waymo is scaling, and consumer subscriptions exceed 325 million. The stock trades at a P/E of 32, with 63 buy ratings, no sells, and an analyst target of $378.50.

Year to date Alphabet is up a measured 11.83%, a steadier trajectory than STX’s vertical move. Prediction markets price a 95.9% probability of an earnings beat resolving today, and an 85.5% probability of Gemini reporting 800 million-plus monthly active users.

CEO Sundar Pichai called the quarter “a tremendous quarter for Alphabet” with “the launch of Gemini 3” as “a major milestone.” That is the AI compounding flywheel. Seagate is the cyclical pick-and-shovel trade priced like a software company.

For investors weighing AI exposure, Alphabet’s full-stack model and defensible multiple warrant a closer look on the research bench while the debate over hard-drive cyclicality continues.

Contact [email protected] for any questions or corrections.