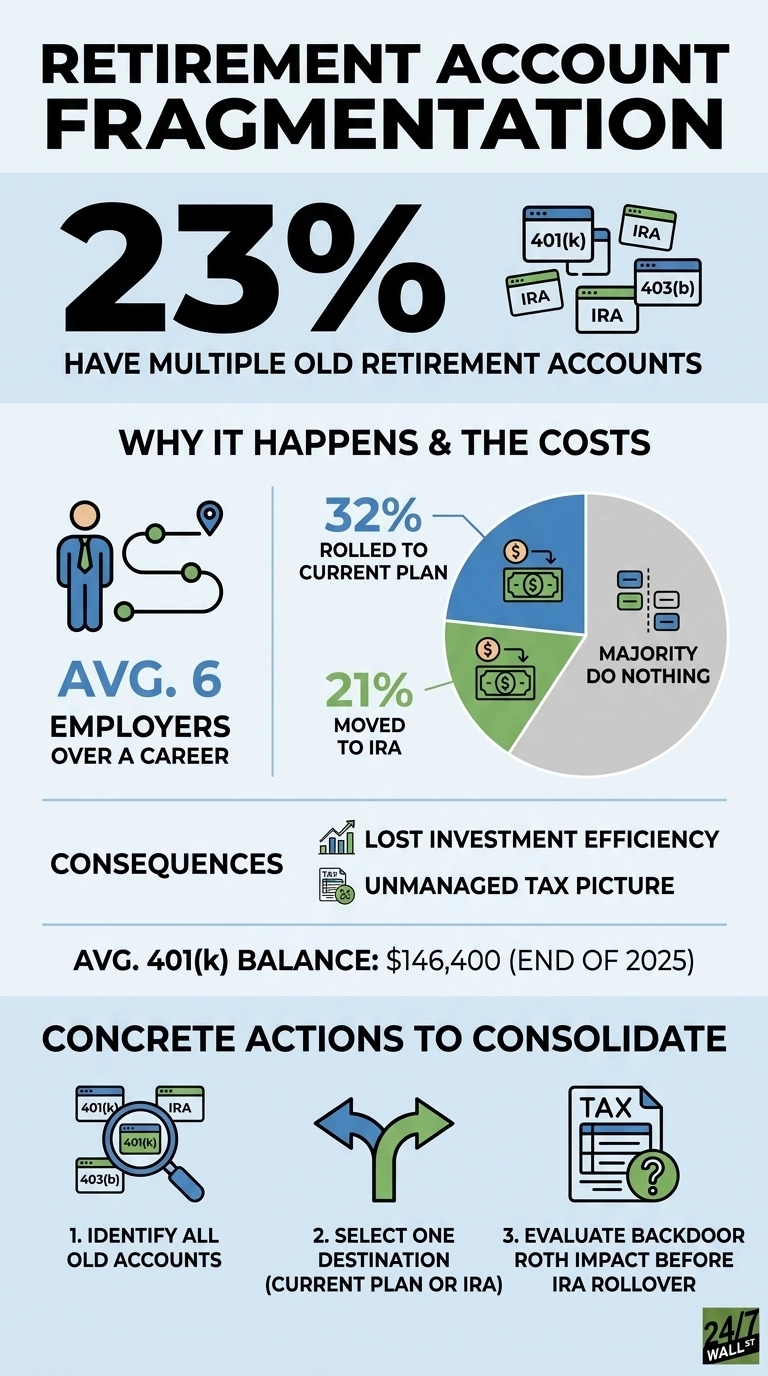

The typical American worker now passes through six employers over a career, and each job change leaves behind a retirement account to keep track of. Fidelity’s 2026 study found that 23% of Americans with retirement accounts still have multiple balances sitting in old or current workplace plans. That fragmentation is the quiet drag on retirement readiness that most people never put on their financial to-do list, and it carries two costs that compound the longer they go unaddressed: lost investment efficiency and a tax picture that nobody is actively managing.

The Fragmentation Problem

Old 401(k) accounts do not disappear when a worker moves on. They sit in whatever investment lineup their previous employer offered, often in a default target-date fund or, worse, in a stable-value option chosen years ago and never revisited. The average 401(k) balance ended 2025 at $146,400, up 11% over the prior year, and balances rose for the third straight year in double digits. Compounding at that pace matters, but only if a participant’s full retirement asset base is actually invested in line with their plan. When pieces are scattered across three or four legacy accounts, the allocation a worker thinks they have is almost never the allocation they actually own.

Fidelity reports average 401(k) balances of $270,800 for Boomers, $222,100 for Gen X, $83,700 for Millennials, and $17,900 for Gen Z. A Gen X worker with a $222,100 current balance plus two forgotten $40,000 accounts from earlier jobs is running a portfolio that looks nothing like the one in their head, and the misalignment grows every year the accounts stay separate.

What People Have And Have Not Done

Among Americans with retirement accounts, only 32% have rolled over a previous balance into a current workplace plan, and 21% have moved one to a personal IRA. That leaves a majority who have done nothing with the accounts they left behind. The reasons are familiar: rollovers require paperwork, plan administrators on both ends, and a decision about where the money should land. None of that is urgent in any given week, so it does not happen.

The cost shows up in two places. The first is investment drift. A 2014 target date fund picked at a 2014 job is not the same product a participant would choose today, and contribution dollars are no longer flowing in to rebalance the mix. The second is fees: small legacy balances often sit in plan tiers with higher expense ratios than those available in a current employer’s plan or a low-cost IRA, and that fee differential compounds against the participant for the rest of their working life.

The Tax Coordination Most People Skip

Fragmentation also breaks tax planning, with only 12% of Americans saying consolidation is part of their tax approach, and just 15% have completed a Roth conversion. Coordinating pre-tax, Roth, and taxable balances is hard enough with one of each. Doing it across four 401(k) accounts at different recordkeepers is something almost no household actually attempts. Roth conversions, in particular, are sensitive to the size and location of pre-tax balances, and the pro rata rule treats all traditional IRA dollars as a single pool. A worker who rolls over a pre-tax 401(k) into an IRA without considering the backdoor Roth strategy can unintentionally close that door.

Fidelity found that Americans with a written retirement plan are more than twice as likely as their peers to feel confident about their prospects, and among current retirees, 81% of those with a plan say they have enough money to last their lifetime, compared with 45% of those without one. Consolidation is the step that makes a written plan possible.

Closing The Gap

Three concrete steps tend to close most of the gap for households in this position. The first is identifying every retirement account opened under a Social Security number, including accounts from jobs held a decade ago; the Department of Labor’s abandoned plan search can help locate accounts when a former employer is hard to track down. The second is selecting a destination, typically either a current workplace plan that accepts rollovers and offers low-cost index options or a single IRA at a major custodian.

The third is evaluating whether a future backdoor Roth strategy is relevant before any rollover into an IRA, since moving pre-tax 401(k) dollars into an IRA can affect that calculation for years. The savings rate hit 3.7% in the first quarter of 2026, down from 5.2% a year earlier, which means new contributions are doing less of the heavy lifting than they used to. Getting the existing balances to work together is where the leverage lies.

Contact [email protected] for any questions or corrections.