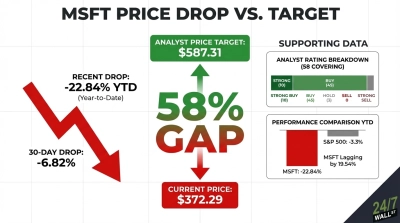

Microsoft’s (NASDAQ:MSFT | MSFT Price Prediction) fiscal third-quarter earnings report had every ingredient of a rally catalyst. Instead, the stock did the opposite. Shares are trading around $400 through midday on April 30, down nearly 6% since the company’s earnings call despite a fourth consecutive beat. The disconnect between fundamentals and the stock reaction deserves scrutiny, because on almost every line that matters for a long-duration cloud and AI franchise, this was a quarter to own.

The Numbers That Argue For A Rally

Start with the headline: EPS of $4.27 versus a $4.07 estimate, on revenue of $82.886 billion, up 18% year over year. Net income climbed 23% and operating cash flow expanded 26% to $46.679 billion. Intelligent Cloud rose 30%, and Azure accelerated to 40% growth.

The forward-demand signal was even stronger. Commercial remaining performance obligations reached $627 billion, nearly doubling year over year. That is a multi-year revenue backlog larger than the market cap of most S&P 500 components. CEO Satya Nadella anchored the call on the AI line item: “Our AI business surpassed an annual revenue run rate of $37 billion, up 123% year-over-year.”

What The Market Is Actually Worried About

The single uncomfortable number was CapEx. Microsoft spent $30.876 billion in the quarter, up 84% year over year. That figure is doing the heavy lifting on the bear thesis, and it shows up in sentiment data. A widely circulated r/stocks thread titled “Microsoft cloud revenue accelerates as spending growth cools” framed the tension cleanly, while r/investing’s most active post asked, bluntly, “What’s the Microsoft bull case?”

Composite prediction sentiment registered 58.36, neutral with medium confidence, with a 30-day change of -8.76 points. Translation: traders accept the growth, but they want to see operating margin hold while infrastructure dollars compound.

The Pattern, And Why It Matters

This reaction fits a clear pattern. Across the last five reports, all earnings beats, the average day-of move was -1%, with Q2 FY26 dropping 10% on a 8% beat. Investors are repricing the AI capex cycle in real time, even as Nadella argues that capacity is the binding constraint while demand keeps building.

At roughly 31 times trailing earnings with a backlog approaching two-thirds of a trillion dollars, the math says the quarter deserved a green candle. Keep an eye on the stock into next quarter, when the conversation shifts from how much Microsoft is spending to how quickly that spend converts to Azure revenue.

Contact [email protected] for any questions or corrections.