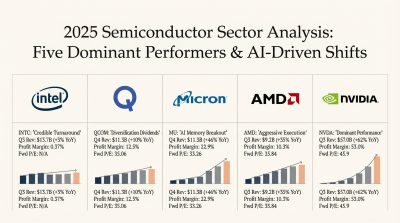

Intel (NASDAQ:INTC | INTC Price Prediction) is the chip story everyone is shouting about, with the stock up 159.57% year to date on a Lip-Bu Tan turnaround narrative wrapped around AI inference and a NVIDIA DGX Rubin host CPU win. But here is what you should actually be watching.

The Intel Trade Is Already Crowded, and Cracked

Intel just dropped 3.85% in a single session on May 4, after running 90.12% in a single month. That is the textbook signature of a narrative trade running out of fresh buyers. The fundamentals underneath the headline are uglier than the tape suggests. Q1 FY26 produced a GAAP net loss of $3.73 billion driven by a $4.07 billion restructuring charge tied to a Mobileye goodwill impairment, with free cash flow of negative $3.87 billion and capex of $4.96 billion. Intel Foundry posted a $2.51 billion operating loss in Q4 2025. Headcount has been cut from 108,900 to 85,100. The U.S. government now holds a meaningful equity stake, and management has flagged the potential pause or discontinuation of Intel 14A if customer demand falls short. Q2 26 non-GAAP EPS guidance of $0.20 is a sequential decline from $0.29. Reddit captured the mood crisply with the most-upvoted Intel post of the period, “Shorting this dumbass company (INTEL),” which pulled in over 12,000 upvotes. Hot trades end this way.

The Picks-and-Shovels of AI Packaging

Advanced packaging is where AI silicon actually gets stitched together into useful product. Three names monetize this without Intel’s foundry bleed.

Amkor Technology (NASDAQ:AMKR) just reported its fourth consecutive EPS beat, with Q1 FY26 non-GAAP EPS of $0.33 versus $0.24 consensus on revenue of $1.68 billion, up 27.5% YoY. Advanced Products revenue expanded from $1.06 billion to $1.37 billion. CEO Kevin Engel framed it cleanly: “Amkor delivered a strong start to 2026 with record first quarter revenue driven by broad-based end market demand.” Q2 EPS guidance of $0.42 to $0.52, full-year capex of $2.5 billion to $3.0 billion, and a fresh $300 million share repurchase authorization approved April 23, 2026 give shareholders capital discipline Intel cannot offer.

ASE Technology Holding (NYSE:ASX) is showing operating leverage that Intel investors can only fantasize about. Q1 FY26 ATM revenue rose 29.7% YoY, gross margin expanded to 20.1% from 16.8%, and computing applications climbed to 27% of ATM revenue from 22%. Advanced packaging now represents 49% of ATM revenues. LEAP services are projected to double from $1.6 billion to $3.2 billion in 2026. The stock is up 100.5% year to date on real numbers.

Kulicke & Soffa (NASDAQ:KLIC) carries the highest gross margin of the group at 49.6%, with non-GAAP operating margin of 12.6%, up from 6.6%. Q1 FY26 EPS of $0.44 beat the $0.33 consensus. Q2 guidance points to ~$230 million in revenue and ~$0.67 EPS, a sharp acceleration. The company repurchased 2.4 million shares for $96.5 million in FY25 and pays a quarterly dividend of $0.205.

Three takeaways frame the redirect. First, every packaging name has direct AI compute exposure without foundry losses or 14A risk. Second, every one is expanding margins while Intel’s GAAP line bleeds. Third, all three are returning capital to shareholders while Intel’s dividend is suspended and the U.S. government dilutes the equity stack.

Investors looking past the Intel headline can research the packaging trio that is already monetizing the buildout: Amkor, ASE, and Kulicke & Soffa.

Contact [email protected] for any questions or corrections.