Wall Street can’t stop talking about Intel (NASDAQ:INTC | INTC Price Prediction), the once-faded chipmaker now sporting a 168.75% year-to-date rally on the back of an NVIDIA $5 billion equity injection, a U.S. government stake, and breathless turnaround chatter. Here is what the data actually shows.

The Intel Trade Is Crowded, Capital-Hungry, and Mispriced for This Rate Regime

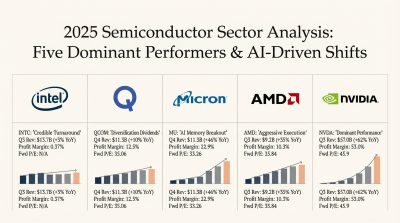

The June 5 jobs print pushed the 10-year Treasury yield to 4.47%, sitting in the 93.5th percentile of its 12-month range. That is the worst possible backdrop for a company spending $4.96 billion in a single quarter on capex while bleeding negative $3.87 billion in free cash flow. Intel posted a GAAP net loss of $3.73 billion in Q1 FY26, its Foundry segment shed roughly $2.5 billion in operating losses in Q4 25 alone, and trailing EPS sits at -$0.60. The forward multiple? A laughable 123x. Shares already cracked 13.52% lower in the past week, and analysts carry a consensus target of $89.32, below the current $99.17. The crowd is paying turnaround-success prices for a company still mid-restructuring while capital costs stay higher for longer.

The redirect is obvious: Alphabet (NASDAQ:GOOGL), down 7.41% over the past month on the same yield scare that punished Intel, but for entirely different reasons. Here are three.

1. The Cheapest Hypergrowth Story in Mega-Cap AI

Google trades at a forward P/E of 26 while delivering 82% year-over-year earnings growth and 21.8% revenue growth. Q1 FY26 EPS of $5.11 exceeded the $2.63 estimate, the fourth consecutive beat. You are paying a market multiple for a company compounding earnings at hyperscaler rates. Intel offers no comparable yardstick because it has no earnings to multiply.

2. Actual AI Monetization at Scale

Google Cloud revenue grew 63% to $20.03 billion in Q1, with backlog nearly doubling quarter-over-quarter to over $460 billion. Gemini is processing 16 billion tokens per minute via API, up 60% QoQ. Paid subscriptions hit 350 million, and Waymo is logging over 500,000 fully autonomous rides per week. CEO Sundar Pichai summarized it bluntly: “Our AI investments and full stack approach are lighting up every part of the business.” Operating margin of 36.1% is what AI monetization looks like in practice.

3. A Fortress Built for Higher-for-Longer

While Intel borrows aggressively to fund its foundry buildout, Alphabet runs with a debt-to-equity ratio of 0.14 and interest coverage of 903x. FY25 free cash flow reached $73.27 billion, return on equity stands at 38.9%, and management just authorized a 5% dividend hike to $0.22 per share quarterly. The recent $80 billion equity and convertible preferred structure front-loads AI compute spend without straining the underlying engine. Reddit’s most-upvoted GOOGL post this week framed it plainly: “For those who keep asking for a ‘one buy and hold for the next 10 years’ the opportunity is here: it’s GOOGL.” Analysts agree, with 57 buy ratings, zero sells, and a consensus target of $431.19.

The Action

For investors weighing the two, the setup favors Alphabet’s cash-generative model over Intel’s capital-intensive rebuild while yields stay elevated. Watch the 10-year yield, Intel’s Foundry segment losses, and Google Cloud’s backlog conversion for confirmation of the divergence thesis.

Contact [email protected] for any questions or corrections.