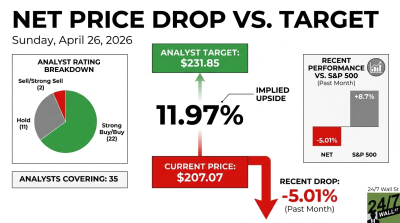

Susquehanna analyst Shyam Patil raised his price target on Cloudflare (NYSE:NET | NET Price Prediction) to $200 from $190 while maintaining a Neutral rating. The price target raise follows a Q1 FY2026 beat and the company’s announcement of a sweeping workforce restructuring tied to an “AI-first” operating model.

NET stock closed at $196.13 on May 8 after sliding from $249 at the time of the earnings filing. The new target sits just above current levels, signaling that Susquehanna views the pivot as strategically sound rather than a thesis-changing event.

| Ticker | Company | Firm | Action | Old Rating | New Rating | Old Target | New Target |

|---|---|---|---|---|---|---|---|

| NET | Cloudflare | Susquehanna | Price Target Raise | Neutral | Neutral | $190 | $200 |

The Analyst’s Case

Patil characterized the period as a “fine quarter,” with Cloudflare beating on both the top and bottom line and continuing to show strong growth, especially with large customers. He also flagged the “more prudent guidance” for Q2 FY2026 as a notable wrinkle.

The headline catalyst is the company’s significant headcount reduction as it pivots toward an AI-first operating structure. The retained Neutral rating signals patience: operating leverage from the restructuring still needs to prove out before Susquehanna commits more aggressively.

Company Snapshot

Cloudflare reported Q1 FY2026 revenue of $639.755 million, up 34% year over year, topping consensus of $622.611 million. Non-GAAP EPS reached $0.25 versus $0.23 expected, while free cash flow climbed to $84.074 million.

CEO Matthew Prince announced a reduction of more than 1,100 employees and restructuring charges of $140 to $150 million, primarily in Q2 2026. Prince asserted that AI is “shaping up to be the biggest tailwind we’ve ever seen in Cloudflare’s history.”

Why the Move Matters Now

Management guided Cloudflare’s full-year 2026 revenue to $2.805 to $2.813 billion and non-GAAP EPS to $1.19 to $1.20. Q2 revenue is forecast at $664 to $665 million.

Cloudflare’s valuation remains rich, with a P/FCF of 193 and price-to-book of 43. An AI-first operating model, in practice, means agents handling support tickets, AI-augmented engineering, and leaner sales operations. The bet is that productivity gains, with 97% of engineers using AI coding tools, translate into durable margin expansion.

What It Means for Your Portfolio

For prudent investors, Susquehanna’s measured raise captures the two-sided debate on Cloudflare stock. The bulls point to security growth, Workers AI traction, and meaningful operating leverage from a leaner cost base. The bears focus on multiple compression risk and execution risk on the workforce transition, with NET stock down 10% over the past week despite the earnings beat.

Watch for whether Cloudflare’s Q2 FY2026 results show productivity gains converting into margin expansion. The company’s June 9 Investor Day should provide deeper color on unit economics, and position sizing and patience may matter more here than chasing a single analyst note.

Contact [email protected] for any questions or corrections.