Quantum computing has minted few clean winners, but IonQ (NYSE:IONQ | IONQ Price Prediction) is making the strongest case for category leadership after a Q1 that blew past every line of guidance. Our 24/7 Wall St. price target reflects a model that combines forward earnings power with proprietary factor adjustments, and on IONQ the signal is unusually loud.

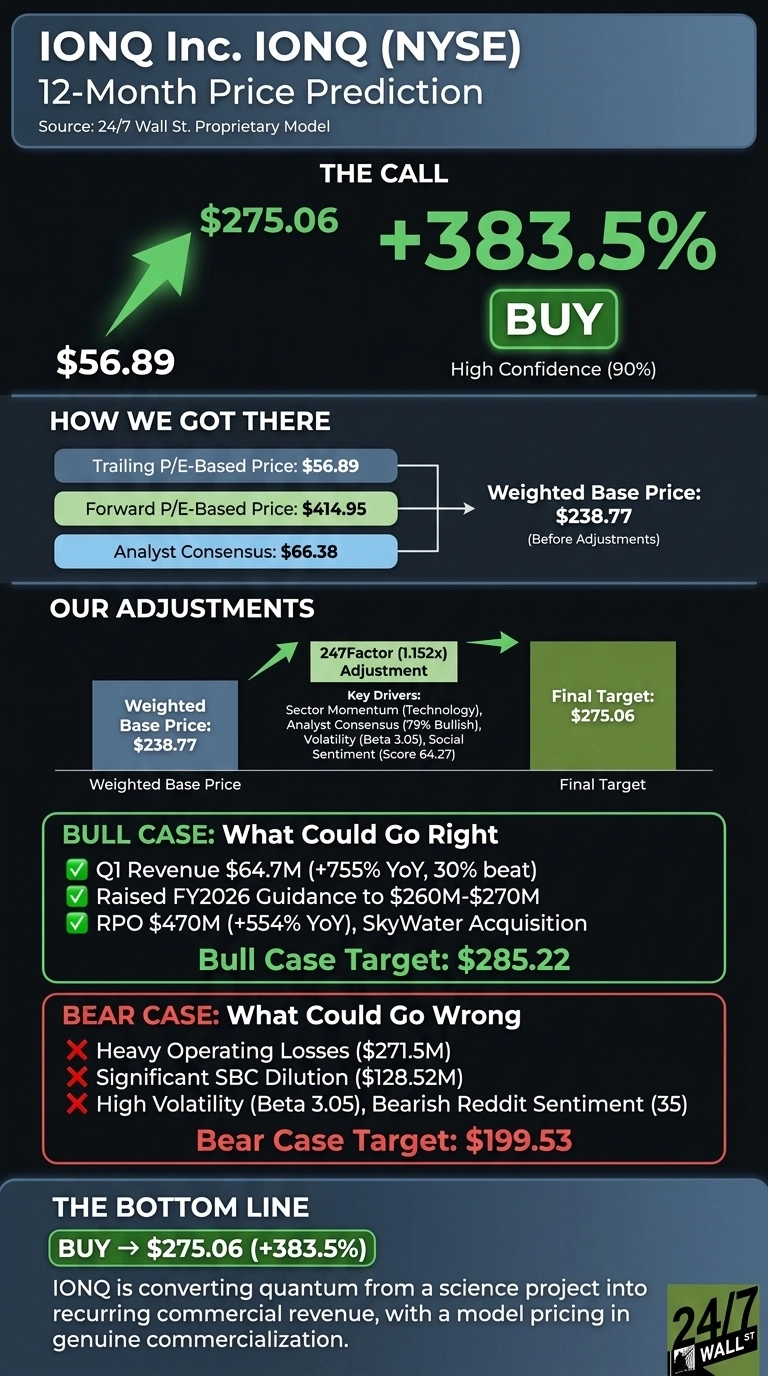

The 24/7 Wall St. price target for IonQ is $275.06 over the next 12 months, implying 383.5% upside from $56.89. Our recommendation is buy with high confidence (90%). The model is pricing in genuine commercialization.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $56.89 |

| 24/7 Wall St. Price Target | $275.06 |

| Upside | 383.5% |

| Recommendation | BUY |

| Confidence Level | 90% |

A 755% Revenue Quarter Reset the Story

IonQ has run hard. The stock is up 24.35% in the past week, 97.6% in the past month, and 81.93% over one year, yet still sits 22% below its $84.64 52-week high.

On May 6, 2026, IonQ reported Q1 revenue of $64.7 million, growth of 755% year-over-year and 30% above the guidance midpoint, with adjusted EPS of -$0.34.

Remaining performance obligations jumped to $470 million, up 554% year-over-year, and management raised full-year 2026 revenue guidance to $260 million to $270 million. The first 256-qubit system was presold to the University of Cambridge, and IonQ won a $39 million Space Development Agency HALO contract.

Why Bulls See a Breakout Ahead

The bull thesis is straightforward: IonQ is the first quantum pure-play to scale revenue meaningfully. CEO Niccolo de Masi told investors this was “our fourth consecutive quarter of record-breaking results”, with $64.7 million of GAAP revenue… more than 8x what we delivered in the same period last year.” Commercial customers now drive 60% of revenue, international markets 35%, and IonQ has sold into over 30 countries.

Analyst consensus is 11 buys, 3 holds, 0 sells, with a consensus target of $66.38. Our bull-case scenario points to $285.22 over 12 months. With $3.1 billion of cash and the pending SkyWater acquisition pulling the manufacturing roadmap forward, the runway is real.

The Risks Worth Watching

IonQ is still burning cash at scale. Q1 operating loss was $271.5 million, adjusted EBITDA loss was $96.75 million, and stock-based compensation hit $128.52 million, nearly 2x revenue. Bulls would counter that R&D of $125.74 million grew 215% and, per CFO Inder Singh, “exceeded the entire reported R&D in the quantum industry” last year, framing the burn as a moat investment.

Beta of 3.05 means drawdowns are violent: IONQ traded as low as $25.89 in the last 12 months. Reddit sentiment has cooled to 35 (bearish), and our bear-case scenario lands at $199.53.

IonQ Price Prediction 2026-2030

Our price target of $275.06, a buy rating, and 90% confidence rest on one fact: IonQ is converting quantum from a science project into recurring commercial revenue. The thesis strengthens if guidance keeps climbing and the 256-qubit chip stays on track. It weakens if cash burn accelerates beyond the $330 million EBITDA loss ceiling or SkyWater closing slips.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $275.06 |

| 2027 | $650 |

| 2028 | $1,450 |

| 2029 | $3,100 |

| 2030 | $6,340.38 |

These projections assume IonQ executes on its roadmap to 2 million qubits by 2030 and that commercial revenue continues compounding above 100%. Significant downside could result from quantum competition from NVIDIA partners, encryption-timeline slippage, or dilution from further equity raises.

Contact [email protected] for any questions or corrections.