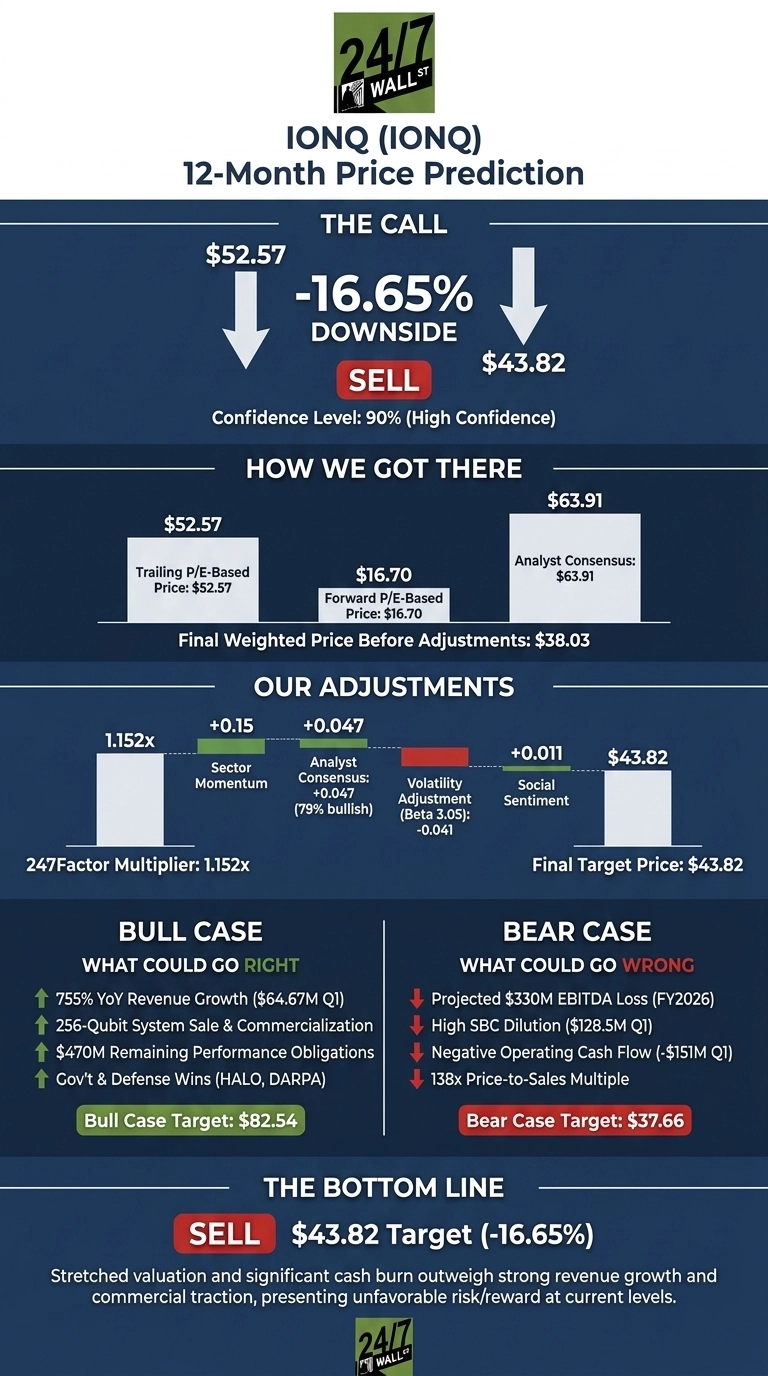

I’m going to lead with the verdict. Our 24/7 Wall St. price target for IonQ (NYSE:IONQ | IONQ Price Prediction) is $43.82 over the next 12 months, against a current price of $52.57. That implies -16.65% downside, and our model assigns this call a 90% confidence score, which I read as high conviction. The recommendation is sell, but as you’ll see, the bull case here is genuinely strong.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $52.57 |

| 24/7 Wall St. Price Target | $43.82 |

| Upside/Downside | -16.65% |

| Recommendation | SELL |

| Confidence Level | 90% |

Why We Could Be Wrong

Before going further, I want to be honest: our price target sits below where IonQ trades today, and IonQ is one of the most divisive names in tech. Real upside could come from the 256-qubit system commercialization ramp, or from the Polymarket-tracked question of whether the US federal government takes a stake, currently priced at 47.5%. Treat our target as one datapoint. A full bull case follows below.

A 755% Revenue Beat and a Guidance Raise

IonQ shares jumped 9.52% on May 6, 2026 after Q1 2026 revenue landed at $64.67 million, up 755% year over year and 30% above the midpoint of guidance. Management raised full-year revenue guidance to $260 million to $270 million. The stock is up 79.79% in the past month and 78.69% over the past year, though it remains 24% below the 52-week high of $84.64. Adjusted EPS was -$0.34, with adjusted EBITDA loss of $96.75 million.

The Case for $80+

Bulls have a real story. Remaining performance obligations grew 554% year over year to $470 million, providing rare visibility for a quantum company. Roughly 60% of revenue now comes from commercial customers, signaling the long-promised shift away from pure government dependence.

Defense wins include a $39 million Space Development Agency HALO contract and DARPA’s HARQ selection. Of 14 covering analysts, 11 rate it Buy or Strong Buy with a consensus target of $63.91. Our bull-case scenario reaches $82.54 over 12 months.

The Risks Worth Watching

The bear case starts with cash burn. Operating cash flow ran -$151 million in Q1 alone, and full-year adjusted EBITDA loss is guided to ($330) million to ($310) million. Stock-based compensation hit $128.52 million, nearly double revenue, which is meaningful dilution. The price-to-sales multiple of 138x leaves little room for any execution stumble.

Bulls would counter that R&D spending of $125.74 million reflects deliberate investment in 256-qubit scaling and the pending SkyWater fab acquisition, not bloat. Still, our bear-case 12-month price is $37.66, and Reddit sentiment on options desks has skewed bearish at a 35 score.

The Bottom Line on IonQ

The 24/7 Wall St. price target of $43.82 reflects a sell recommendation with 90% model confidence. The decisive factor is valuation. A 138x sales multiple on a company guiding to a $300M+ EBITDA loss leaves the math unforgiving. The thesis would strengthen if commercial revenue mix pushes past 75% and cash burn narrows by year-end. The bear case holds if SBC remains above revenue and the SkyWater integration slips. After a 79.79% one-month run, the risk/reward looks stretched at current levels.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $48.00 |

| 2027 | $43.82 |

| 2028 | $42.50 |

| 2029 | $41.20 |

| 2030 | $40.18 |

These projections assume IonQ executes against current guidance and the quantum sector continues its multi-year normalization off frothy 2025 multiples. Significant upside could result from a federal government stake or commercial-scale 256-qubit deployments outpacing our base case.

Contact [email protected] for any questions or corrections.