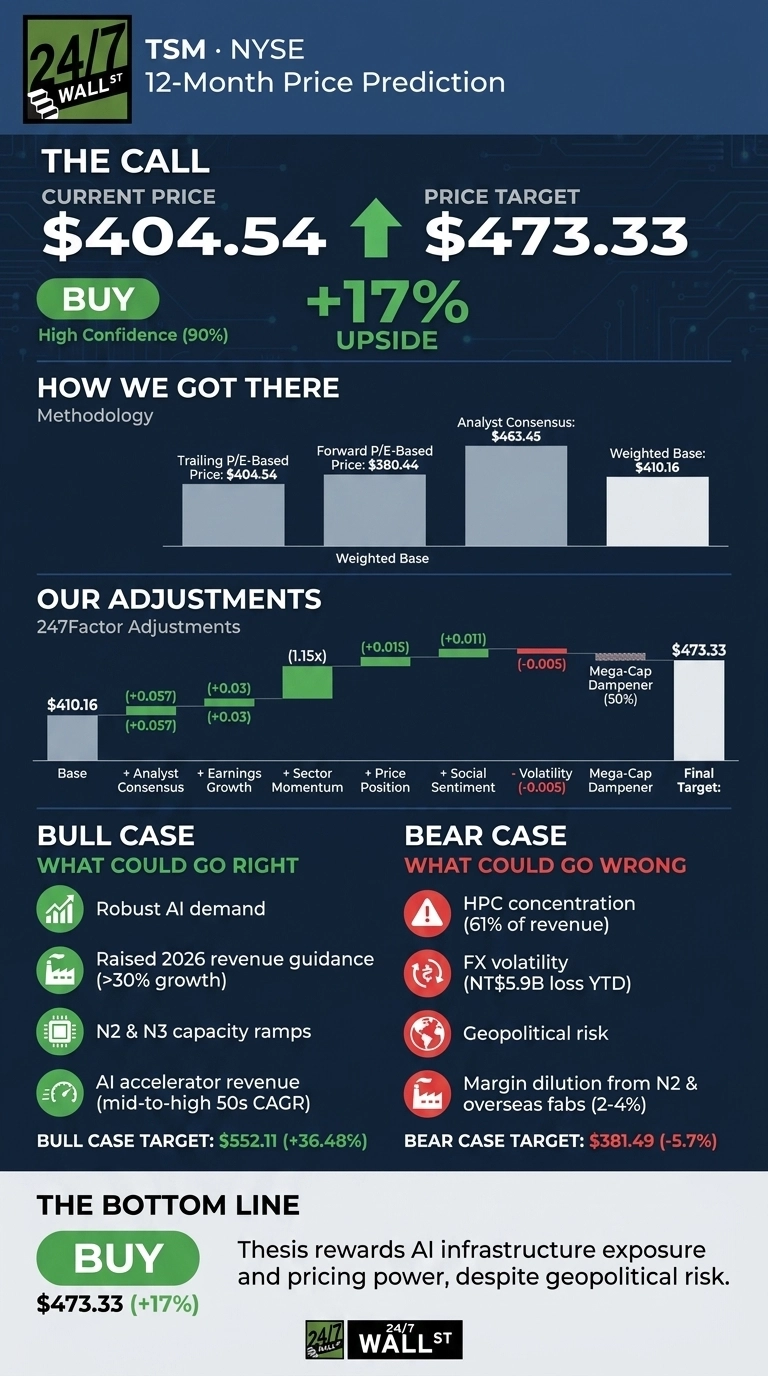

Let me cut to the chase. Taiwan Semiconductor Manufacturing (NYSE:TSM | TSM Price Prediction) trades at $404.54, and our 24/7 Wall St. price target for TSMC is $473.33 over the next 12 months. That implies 17% upside, and our recommendation is buy with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $404.54 |

| 24/7 Wall St. Price Target | $473.33 |

| Upside | 17% |

| Recommendation | BUY |

| Confidence Level | 90% |

An AI-Driven Run That Just Keeps Compounding

TSMC has been one of the megacap leaders of 2026. Shares are up 33.49% year to date, 9.16% over the past month, and a stunning 131.93% over the past year. The stock sits roughly 10% below its 52-week high of $420, with a 14-day RSI of 59.63, which leaves room to run without overbought stress.

The Q1 2026 earnings report on April 16 was the catalyst. TSMC delivered EPS of $3.49 against a $3.362 estimate, revenue of $35.9 billion growing 35.1% year over year, and gross margin of 66.2%, well above the guided 63% to 65% band. April monthly revenue ran NT$410.73 billion, up 17.5% year over year, with cumulative January through April revenue up 29.9%.

The Case for $552 and Higher

The bull case writes itself. C.C. Wei told investors that “AI-related demand continues to be extremely robust” and that the shift from generative to agentic AI is driving another step-up in token consumption. Management raised full-year 2026 revenue guidance to above 30% growth in U.S. dollar terms and now expects 2026 capex toward the high end of the $52 billion to $56 billion range.

N2 entered high-volume manufacturing in Q4 2025 with good yields, and AI accelerator revenue is tracking a mid- to high-50s CAGR through 2029. Our bull case price is $552.11, a 36.48% total return. Eighteen of nineteen covering analysts rate TSMC Buy or Strong Buy with zero sell ratings.

The Risks Worth Watching

HPC concentration is a real exposure. The segment is now 61% of total revenue, meaning any AI capex pause hits TSMC squarely. FX losses on expired forward contracts reached NT$5.9 billion year to date, and outstanding U.S. subsidiary guarantees total NT$519 billion.

Geopolitics around Taiwan remains the perennial unquantifiable risk. Margin dilution from N2 ramp will run 2% to 3% for full-year 2026, with overseas fabs adding another 2% to 3%. Bulls would counter that N3 gross margin is expected to cross the corporate average in the second half of 2026, offsetting much of that drag. Our bear case lands at $381.49, a 5.7% drawdown.

Taiwan Semiconductor Price Prediction 2026-2030

The 24/7 Wall St. price target on TSMC is $473.33, buy rated, confidence 90%. What tips the scale is the durability of the AI capex cycle combined with TSMC’s 72.3% foundry market share and pricing power on leading-edge nodes. The thesis rewards investors who can stomach Taiwan headline risk and want compounding exposure to AI infrastructure. The setup looks less attractive if a U.S. recession threatens 2027 hyperscaler capex or if cross-Strait tensions spike.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $473 |

| 2027 | $525 |

| 2028 | $575 |

| 2029 | $620 |

| 2030 | $666 |

These projections assume TSMC continues executing on N2 and A14 ramps and that AI capex remains the dominant demand driver. Significant upside or downside could result from accelerated Arizona fab economics, a China-Taiwan flashpoint, or a sudden cooling in hyperscaler AI spend.

Contact [email protected] for any questions or corrections.