Apple (NASDAQ:AAPL | AAPL Price Prediction) just delivered its best March quarter ever, raised the dividend, and authorized a fresh $100 billion buyback. Our model thinks the rally has more room to run.

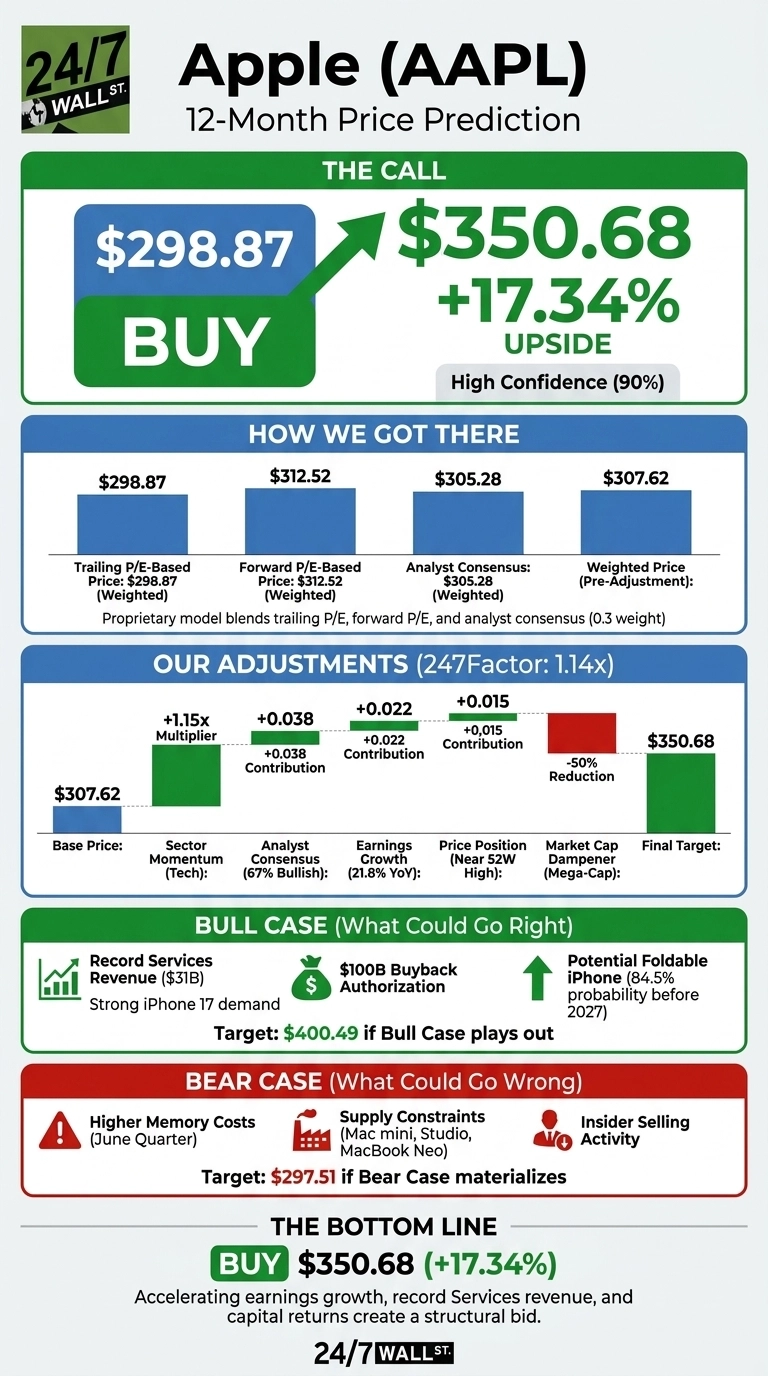

The 24/7 Wall St. price target for Apple is $350.68 over the next 12 months, implying 17.34% upside from the current price of $298.87. Our recommendation is buy, with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $298.87 |

| 24/7 Wall St. Price Target | $350.68 |

| Upside | 17.34% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Blowout March Quarter Reset the Story

Apple has gained 4.05% over the past week, 15.41% over the past month, and 40.92% over the trailing year. The stock trades just under its 52-week high of $300.92, well above the $192.70 low set last spring.

Q2 FY26 results, reported April 30, drove the move. Revenue hit $111.184 billion, up 16.6% YoY, with EPS of $2.01 beating the $1.94 estimate. iPhone revenue jumped to $56.994 billion on what Tim Cook called “extraordinary demand for the iPhone 17 lineup“, and Services set an all-time record at $30.976 billion. Greater China revenue surged to $20.497 billion, with management noting first-half China growth of 33%. That makes eight consecutive quarters of EPS beats.

The Case for $400+

Bulls have plenty to work with. The iPhone 17 family is, per Cook, “the most popular lineup in our history” with 99% US customer satisfaction. The installed base exceeds 2.5 billion active devices, feeding a 76.7%-gross-margin Services engine. June-quarter guidance calls for revenue growth of 14% to 17% and gross margin of 47.5% to 48.5%.

Polymarket assigns a 84.5% probability to a foldable iPhone before 2027, a potential super-cycle catalyst. Our bull-case scenario targets $400.49 within 12 months on faster Services monetization and a sustained China rebound.

Evercore ISI raised the firm’s price target on Apple to $365 from $330 and keeps an Outperform rating on the shares.

The Risks Worth Watching

The bear case starts with valuation. Apple trades at a P/E of 39, well above its historical norm. Cook flagged “significantly higher memory costs” in the June quarter, and supply constraints persist on Mac mini, Mac Studio, and MacBook Neo. Insider activity has skewed toward selling across 48 recent transactions.

Trade and tariff exposure remain wildcards. That said, bulls would counter that buyback flow of $90.71 billion in FY25 and the fresh $100 billion authorization should absorb much of that supply. Our bear-case scenario sees the stock drifting to $297.51, essentially flat over the next year.

Our Take

The model output: Buy, with a 24/7 Wall St. price target of $350.68 and 90% confidence. The tipping factor is the combination of accelerating earnings growth, record Services revenue, and a capital return program that creates a structural bid.

The bull thesis strengthens if Services keeps compounding in the mid-teens and June-quarter gross margin holds the 47.5% guidance floor. The thesis weakens if memory cost pressure pushes Products gross margin below 38% or China growth rolls over.

Apple Price Prediction 2026-2030

Looking further ahead, here is where our model projects Apple could trade, assuming current growth and capital-return trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $350.68 |

| 2027 | $385 |

| 2028 | $420 |

| 2029 | $455 |

| 2030 | $495 |

These projections assume Apple continues executing on iPhone, Services, and AI integration. Significant upside could come from a foldable iPhone launch or aggressive Apple Intelligence monetization; downside risk centers on sustained memory cost inflation, tariff escalation, or a stumble in the John Ternus CEO transition slated for September.

Contact [email protected] for any questions or corrections.