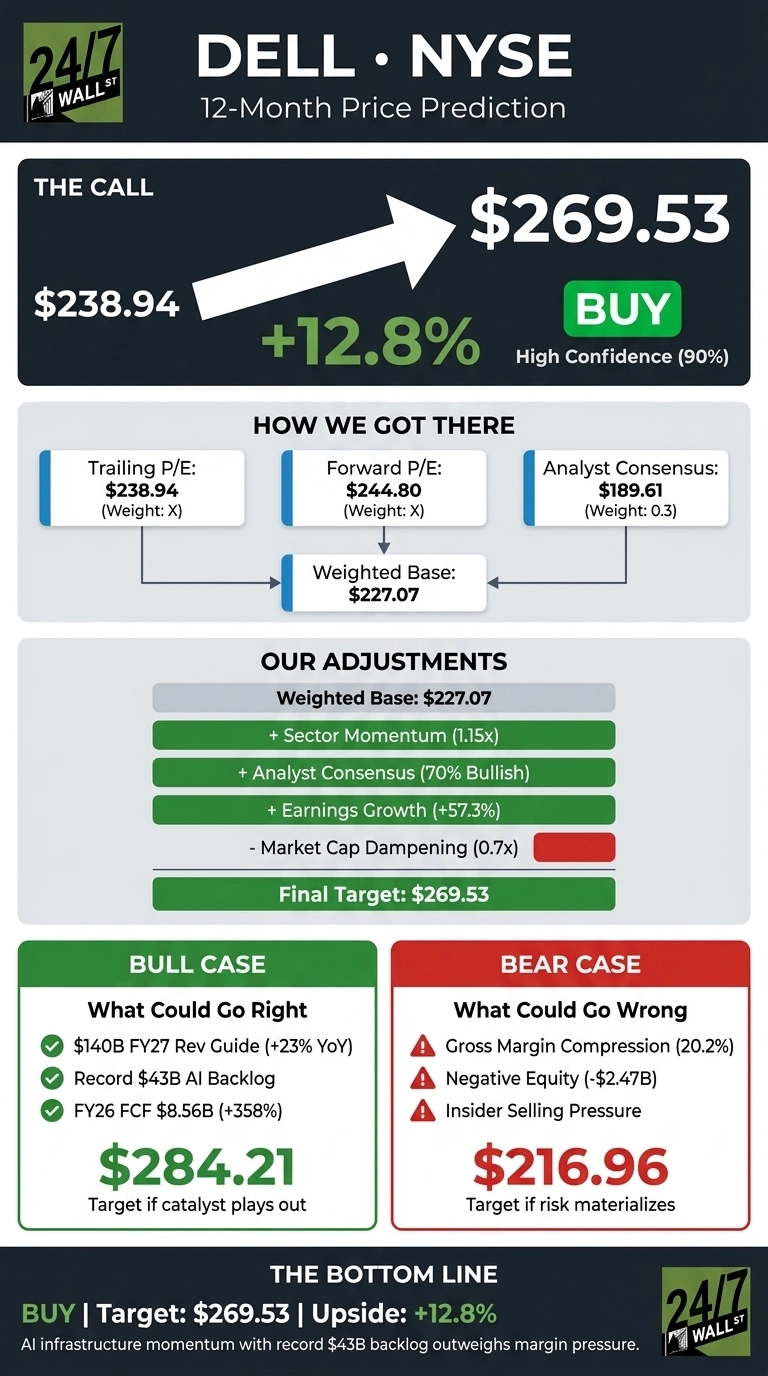

Dell Technologies (NYSE:DELL | DELL Price Prediction) has become one of the defining AI infrastructure trades of 2026, and our proprietary model sees room to run. Shares trade at $238.94 as of May 12, 2026, up 91.28% year to date and 134.62% over the past year. Our 24/7 Wall St. price target for Dell is $269.53, implying 12.8% upside over the next 12 months. The recommendation is buy with high confidence (90% on our scale).

| Metric | Value |

|---|---|

| Current Price | $238.94 |

| 24/7 Wall St. Price Target | $269.53 |

| Upside | 12.8% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Record Run Meets a Profit-Taking Wobble

Dell printed a record high before a 3.28% pullback on May 12, triggered by Jim Cramer’s “smell the reversal” warning on crowded AI trades. Even with that dip, DELL is up 10.46% in the past week and 34.79% in the past month, sitting 28% from its 52-week high of $263.99.

Fundamentals justify the rerating. Fiscal Q4 FY26 revenue hit $33.379 billion (+40.21% YoY), with non-GAAP EPS of $3.89 topping consensus expectations. AI-optimized server revenue exploded 342% YoY to $8.952 billion, and management exited the year with a record $43 billion AI backlog. Recent catalysts include a $1.44 billion Boost Run AI cloud agreement and the Pangea 5 supercomputer project with TotalEnergies and NVIDIA.

The Case for $284 and Beyond

The bull case rests on AI server economics compounding. Dell’s FY27 guidance calls for $138 to $142 billion in revenue (+23% YoY), with AI-optimized server revenue roughly doubling to $50 billion. Non-GAAP EPS guidance of $12.90 at the midpoint (+25% YoY) would support a re-rating toward our bull scenario of $284.21, an 18.95% one-year return.

Jim Cramer identified Dell as a core “AI factory” infrastructure provider, and a DCF model cited by Sahm Capital implies fair value of $265.66. Free cash flow tells the same story: FY26 FCF surged 357.73% to $8.555 billion, funding a 20% dividend hike and a $10 billion buyback expansion.

The Risks Worth Watching

The bear scenario maps to $216.96, a 9.2% decline. UBS already downgraded DELL from Buy to Neutral, citing how much AI is already in the price. Wall Street’s consensus target sits at just $189.61, which would imply real downside if multiple compression takes hold.

Gross margin compression is the structural worry: GAAP gross margin slid to 20.2% in Q4 FY26 from 23.7% from 18.3% a year earlier. Shareholders’ equity remains negative at -$2.470 billion.

Insider selling has been notable, with COO Jeffrey Clarke selling 116,000 shares at $182.48 in April. Bulls counter that margin pressure reflects deliberate volume capture in a hyperscaler land grab, and operating cash flow of $11.185 billion (+147.4%) proves the model works at scale.

The Bottom Line

The 24/7 Wall St. price target of $269.53 reflects a buy rating with 90% confidence. The deciding factor is the $43 billion AI backlog, which gives Dell multi-quarter revenue visibility that few hardware peers match.

The constructive read is that the $43 billion backlog and FY27 guide of $140 billion in revenue underwrite multi-quarter visibility, while the cautious read hinges on AI server gross margins compressing below 17% and forcing a forward multiple reset toward analyst consensus.

Here is where our model projects Dell could trade, assuming continued AI infrastructure execution.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $269.53 |

| 2027 | $271.21 |

| 2028 | $295.19 |

| 2029 | $325.18 |

| 2030 | $333.16 |

These projections assume Dell continues executing on AI server demand and protects free cash flow generation. Significant upside or downside could result from hyperscaler capex cycles, NVIDIA GPU allocation dynamics, or a sharper-than-expected commercial PC refresh.

Contact [email protected] for any questions or corrections.