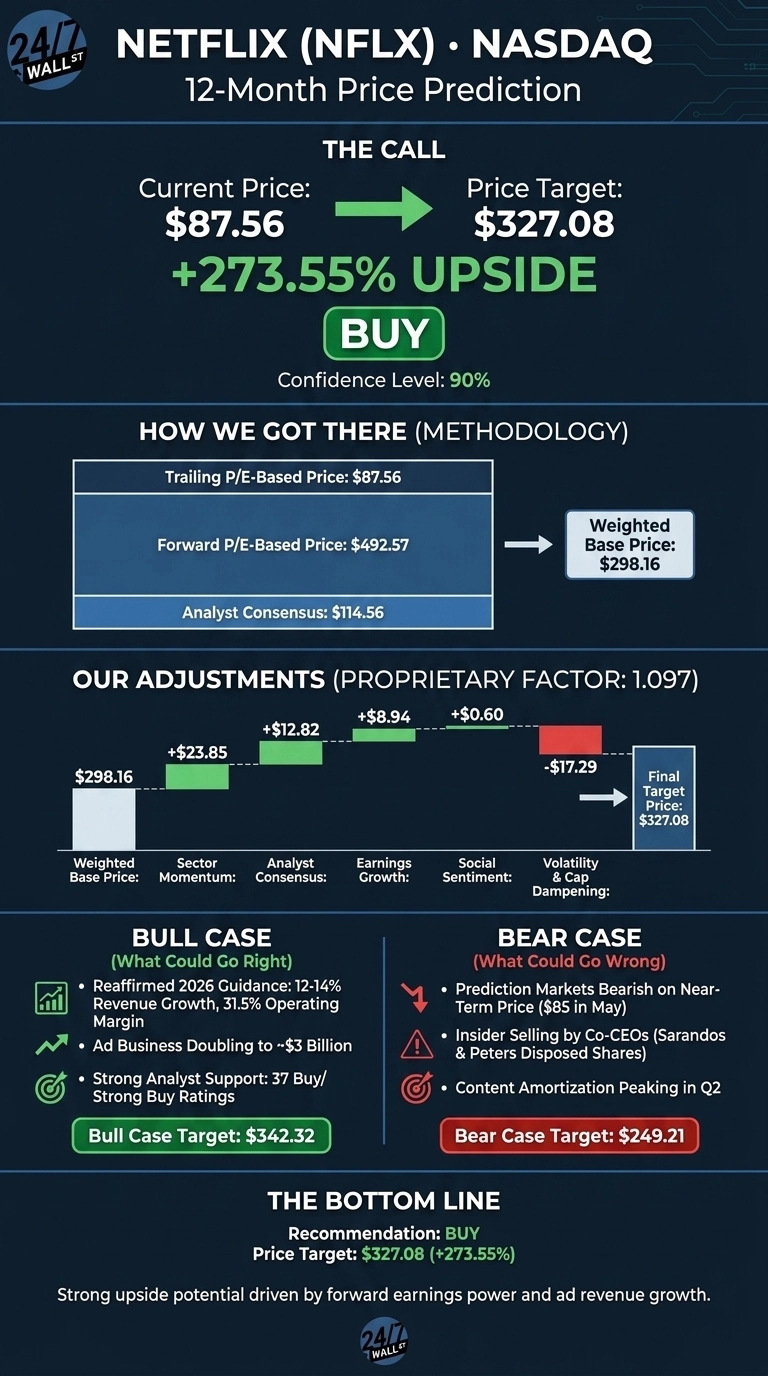

Our Netflix (NASDAQ:NFLX | NFLX Price Prediction) 24/7 Wall St. price target is $327.08, well above where shares trade after a brutal April reset. With NFLX at $87.56, the implied upside of 273.55% is steep, and we rate the name a buy. Confidence in the call is 90%, reflecting strong analyst consensus, accelerating earnings, and a forward EPS profile the market appears to be mispricing after a sharp post-earnings drawdown.

| Metric | Value |

|---|---|

| Current Price | $87.56 |

| 24/7 Wall St. Price Target | $327.08 |

| Upside | 273.55% |

| Recommendation | BUY |

| Confidence Level | 90% |

Why Netflix Stock Tumbled Below $90

Netflix has had a rough run. Shares are down 15.12% over the past month, 6.61% year to date, and 23.09% over the past year. NFLX now sits 15% below its 52-week high of $134.12.

The slide accelerated after the April 16 Q1 2026 report, when revenue of $12.25 billion rose 16.2% YoY and edged consensus, while EPS of $1.23 missed the $1.34 estimate even with a $2.80 billion Warner Bros. termination fee flowing through other income. Free cash flow guidance was raised to approximately $12.5 billion for 2026, and ad-tier sign-ups exceeded 60% of all sign-ups in ads markets.

The Case for $342 and Beyond

Bulls have a lot to work with. Management reaffirmed 12% to 14% revenue growth and a 31.5% operating margin for 2026, with the ad business expected to roughly double to approximately $3 billion. Advertiser count climbed over 70% year over year to more than 4,000 clients, and APAC posted 20% YoY revenue growth behind the World Baseball Classic, which co-CEO Ted Sarandos called “the most-watched program we have ever had in Japan”.

Sell-side support is firm with 37 buy or strong buy ratings versus a single strong sell. If margin expansion sticks and the ad ramp compounds, our bull case extends to $342.32 on a 12-month view.

JPMorgan reiterates an Overweight rating on Netflix with a $118 price target following the company’s fourth annual advertising upfront. JPMorgan is positive on Netflix’s reach, content strategy, and improving advertising technology.

What Could Go Wrong

The bear case is real. Prediction markets are pricing a 61.5% probability that NFLX hits $85 in May 2026, with composite sentiment scoring a bearish 35.71. Insiders have been net sellers, with co-CEOs Sarandos and Peters disposing of 81,600 and 55,597 shares respectively in early May at prices between $87.97 and $92.06.

Content amortization is set to peak in Q2, competition from Disney, Amazon, YouTube, and TikTok remains fierce, and a roughly $700 million Brazilian tax deposit shifted into 2026. To be fair, the May insider selling correlated with scheduled RSU vesting on May 4 rather than fresh discretionary exits, so the signal is softer than it looks. Our bear case lands at $249.21, still above today’s price.

I’d Buy It Here

The 24/7 Wall St. price target on Netflix is $327.08, the recommendation is buy, and confidence is 90%. The tipping point is the gap between forward earnings power and a trailing multiple that has compressed too far. I’d be a buyer here if Q2 2026 earnings on July 16 confirm the 32.6% Q2 operating margin guide and ad revenue tracks toward the $3 billion run rate. I’d stay sidelined if margins slip or the ad ramp stalls.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 (year-end) | $185 |

| 2027 | $327 |

These projections assume Netflix continues compounding revenue in the low-to-mid teens and expanding operating margins toward the mid-30s. Significant upside or downside could result from ad-tier monetization, live-event execution, or a step-change in content amortization.

Contact [email protected] for any questions or corrections.