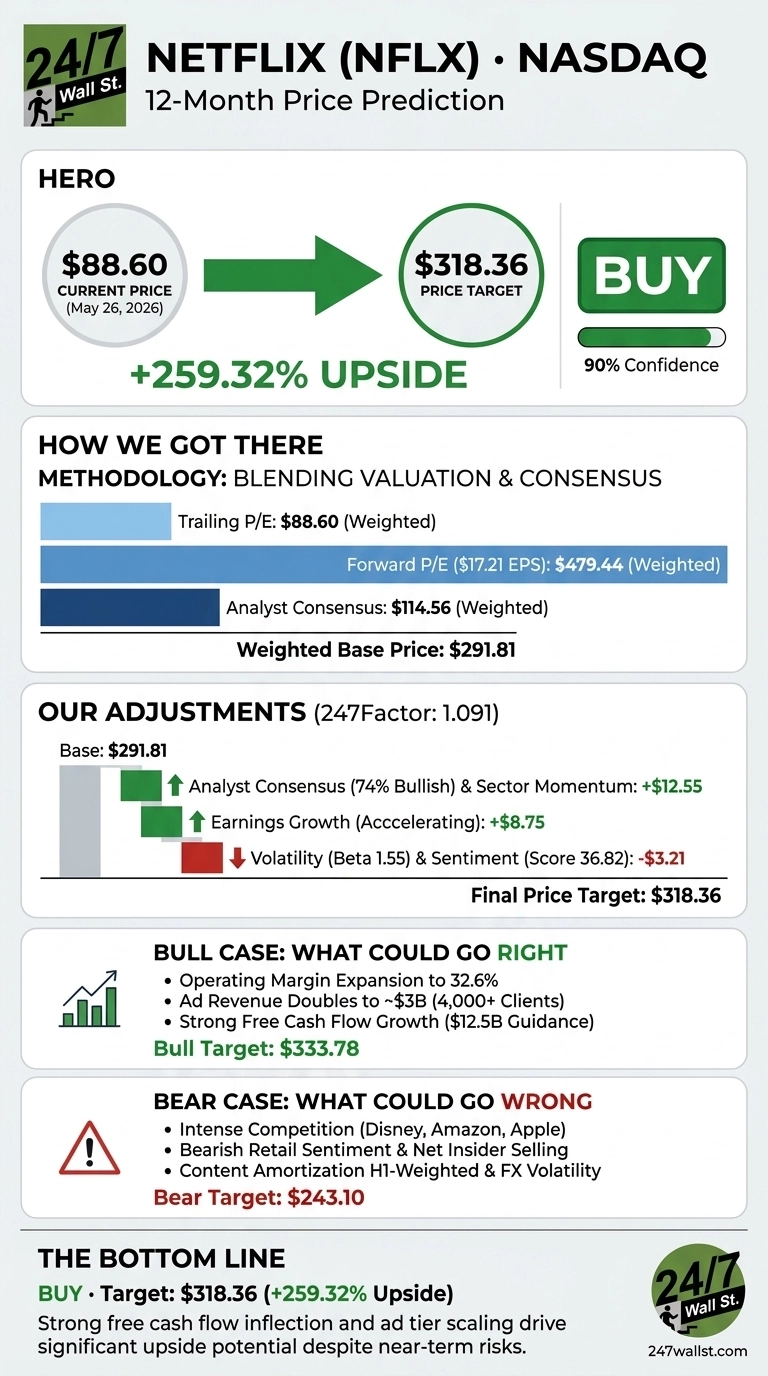

Netflix (NASDAQ:NFLX | NFLX Price Prediction) trades at $88.60, well off its 52-week high of $134.12, and our proprietary model sees substantial room to run as the advertising tier scales and free cash flow inflects.

Our 24/7 Wall St. price target for Netflix is $318.36 over the next 12 months, implying 259.32% upside from current levels. Our recommendation is buy, with a 90% confidence score reflecting strong analyst consensus and accelerating earnings power.

| Metric | Value |

|---|---|

| Current Price | $88.60 |

| 24/7 Wall St. Price Target | $318.36 |

| Upside | 259.32% |

| Recommendation | BUY |

| Confidence Level | 90% |

From $134 Down to $88: What Just Happened to Netflix

Netflix has been a tough hold. Shares are down 25.42% over the past year and 5.5% year-to-date, bottoming at $77 in February before clawing back.

The Q1 2026 earnings report on April 16, 2026 showed revenue of $12.24B, up 16.19% YoY and beating the $12.173B consensus. EPS of $1.23 missed the $1.345 estimate, but the headline obscures the story: Netflix walked away from Warner Bros. and pocketed a $2.80B termination fee, pushing free cash flow to $5.094B for the quarter.

Management raised 2026 free cash flow guidance to $12.5B from $11B, reaffirmed full-year revenue of $50.7B to $51.7B, and guided operating margin to 31.5%. Advertising is on track to roughly double to $3B, with advertiser count up 70% YoY to 4,000+ clients.

The Case for a Breakout Above $300

The bull case rests on operating leverage. Q1 2026 operating income hit $3.957B, up 18.23%, and Q2 guidance calls for a 32.6% operating margin. The ad tier accounted for over 60% of sign-ups in ads markets, and live programming (boxing, NFL, WBC Japan) is widening the moat.

Our bull scenario lands at $333.78 over 12 months. Wall Street consensus sits at $114.56, with 8 Strong Buy and 29 Buy ratings, leaving room for upward revisions if ad revenue and free cash flow continue to beat.

The Risks Worth Watching

The bear case starts with sentiment. Reddit activity on r/wallstreetbets flipped to very bearish on May 21, and insider activity shows net selling across 119 recent transactions. Polymarket traders assign just $85 probability and only $120 by month-end, well below our trajectory.

Competition from Disney, Amazon, Apple, and Alphabet is intense, the Brazilian tax matter cost $619M in Q3 2025, and walking away from Warner Bros. limits content acceleration. Our bear case marks the stock to $243.10. Bulls would counter that the EPS miss and margin compression in recent quarters reflect non-recurring items (the Brazilian tax charge, content amortization weighted to H1) rather than structural weakness.

Netflix Price Prediction 2026-2030

Our 24/7 Wall St. price target of $318.36 carries a 90% confidence score and a buy rating. The tipping factor is free cash flow: management raised 2026 guidance to $12.5B, and the buyback machine restarted with $6.8B remaining.

The bull thesis holds if ad revenue doubles as guided and margins hold above 31%. The thesis weakens if Q2 margins disappoint or if subscriber growth in mature markets stalls.

Looking further ahead, here is where our model projects Netflix could trade, assuming current growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $188.35 |

| 2027 | $510.84 |

| 2028 | $1,149.52 |

| 2029 | $2,074.39 |

| 2030 | $3,111.34 |

These projections assume Netflix continues executing on advertising scale, margin expansion, and disciplined capital returns. Significant upside or downside could result from a major content arms race, regulatory pressure on streaming, or a recessionary hit to advertising budgets.

Contact [email protected] for any questions or corrections.