Netflix (NASDAQ:NFLX | NFLX Price Prediction) just walked away from a Warner Bros. deal with a $2.80 billion termination fee in its pocket, raised free cash flow guidance to roughly $12.5 billion for 2026, and doubled its advertising business toward $3 billion. So why are shares down 4.38% year to date and 24.76% off where they sat a year ago? Can this streamer stage a comeback to $350 by 2027?

Why Netflix Shares Are Stuck Despite Record Cash Flow

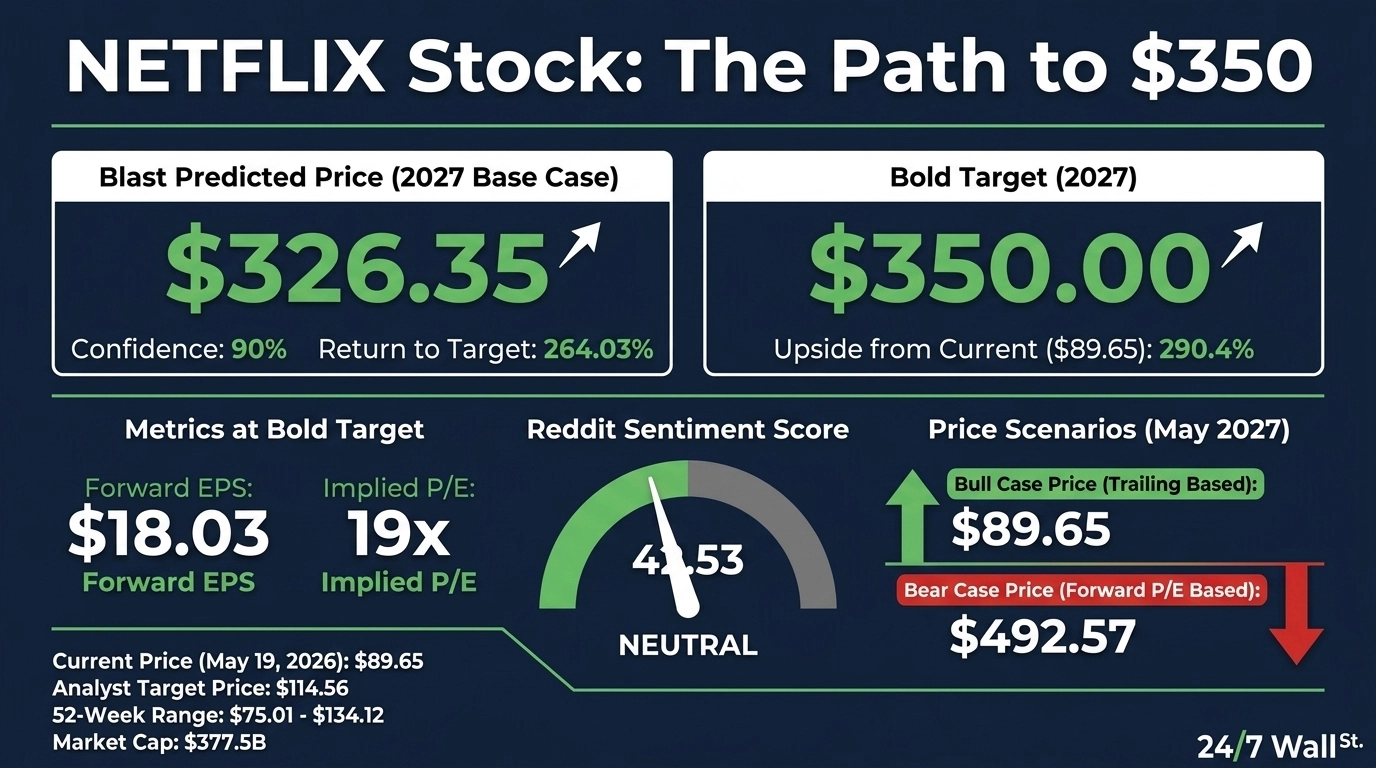

Netflix delivered Q1 revenue of $12.25 billion, up 16.2% YoY, with free cash flow surging 91.44%. Yet shares trade at $89.65, down 7.87% over the past month.

Three factors weigh on the stock. Q1 EPS of $1.23 missed the $1.345 estimate by 8.55%, even with the Warner Bros. windfall. The stock carries a beta of 1.548, so mega-cap tech weakness hits NFLX harder. The Warner Bros. walk-away removed a content acceleration catalyst some investors had priced in. The stock sits 15% below its 52-week high of $134.12.

Wall Street Sees 28% Upside. Our Model Says Far More

The Street’s average target sits at $114.56, supported by 8 Strong Buy, 29 Buy, 12 Hold, and 1 Strong Sell ratings. Bullish sentiment runs at 74%.

The base case prediction is $326.35 with a 90% confidence score, the bull case is $341.95, and the bear case lands at $248.70. Analysts are anchored to trailing earnings while forward EPS of $18.03 reflects operating leverage from advertising and planned 31.5% operating margin. The Street is too conservative on monetization.

The Path to $350 Per Share

Reaching $350 from today’s price of $89.65 requires a gain of 290.4%. That stretches even Netflix’s 10-year history.

With forward EPS of $18.03, a price of $350 implies a forward P/E of 19x. Our base case of $326.35 already implies 6x, meaning the bold target requires roughly 13x additional multiple expansion off depressed implied earnings.

That math works only if three things happen. First, the ad tier must scale: management says it was 60%+ of Q1 sign-ups in ad markets, with advertiser count up 70% YoY to 4,000+ clients.

Second, the content slate (Greta Gerwig’s Narnia, David Fincher, Denzel Washington films, One Hundred Years of Solitude S2) must drive engagement.

Third, the $6.8 billion buyback authorization must keep compressing the share count. Primary risk: a content stumble that lets Disney, Amazon, or Apple steal share.

Where Netflix Trades Today vs Its Earnings Power

At $89.65 against forward EPS of $18.03, shares trade at roughly 5x forward earnings on the model’s estimates, with trailing P/E at 28. The stock sits between the 52-week low of $75.01 and high of $134.12. Over ten years, NFLX has returned 869.29%. That long-term compounding shows what’s possible when streaming economics turn.

Is $350 Realistic?

$350 by 2027 means a 290.4% gain. I’d call that a long shot relative to the base case. Three things must go right: ad revenue must clear $3 billion and accelerate, free cash flow must beat the $12.5 billion raised guide, and the buyback must stay aggressive.

Multiple expansion back toward streaming peers does the rest. A content miss or recessionary ad pullback would derail it. We’ve outlined the blueprint for how Netflix could reach $350 in 2027.

Contact [email protected] for any questions or corrections.