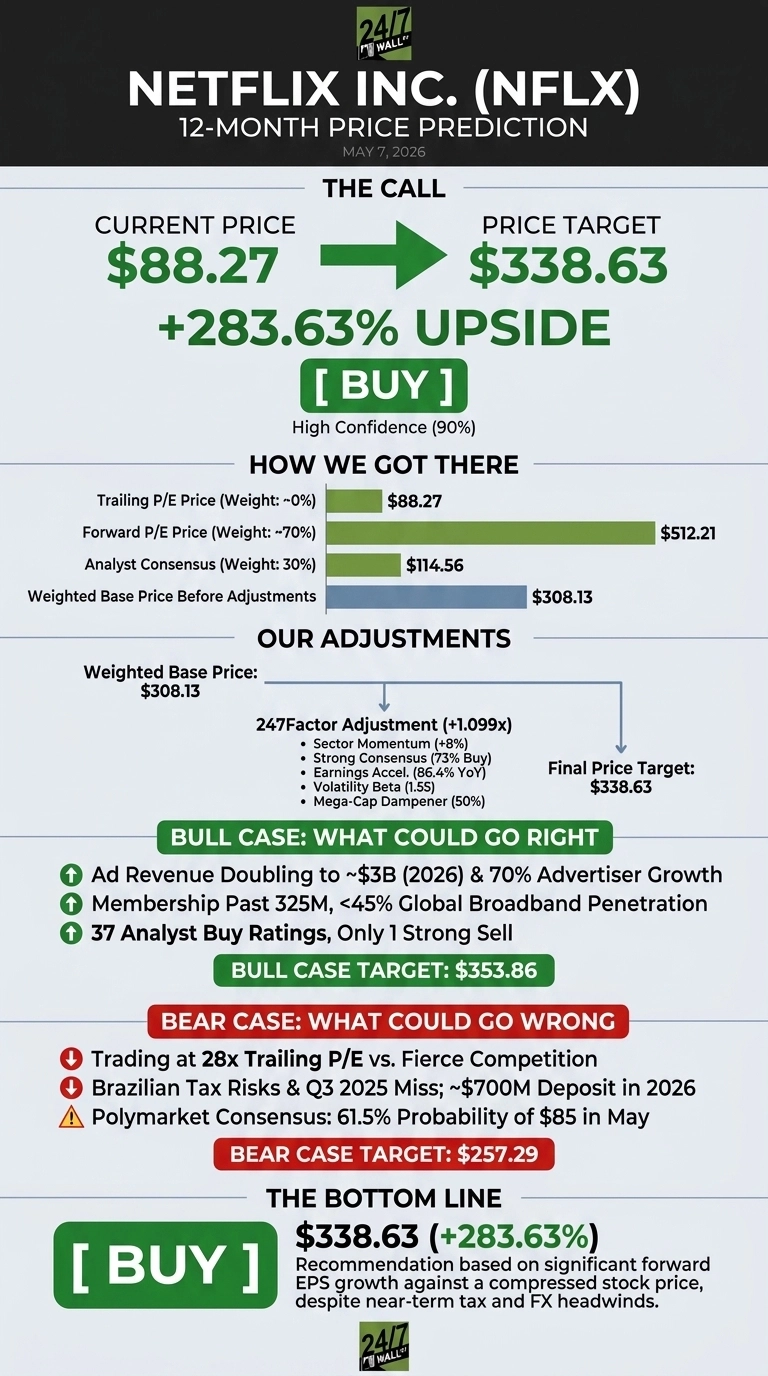

Few stocks have whipsawed investors in 2026 the way Netflix (NASDAQ:NFLX | NFLX Price Prediction) has. Shares plunged from $126.03 in July 2025 to a $77 trough in February 2026, then clawed back to $88.27 as of May 6. Our 24/7 Wall St. price target for Netflix is $338.63, implying 283.63% upside. The recommendation is buy at 90% confidence.

| Metric | Value |

|---|---|

| Current Price | $88.27 |

| 24/7 Wall St. Price Target | $338.63 |

| Upside | 283.63% |

| Recommendation | BUY |

| Confidence | 90% |

From a $77 Trough to a Q1 Beat

Netflix shares are down 10.78% over the past month, 5.86% year to date, and 22.41% over the trailing year, sitting 15% below the $134.12 52-week high. The selloff accelerated after the April 16, 2026 Q1 earnings report, where shares fell from $107.99 at filing to $97.86 within an hour.

Q1 revenue hit $12.25 billion, up 16.19% YoY and beating estimates by 0.63%. EPS of $1.23 came in light versus the $1.34 consensus, missing expectations by 8.55%. Net income of $5.28 billion was inflated by the $2.80 billion Warner Bros. termination fee, but free cash flow of $5.09 billion still grew 91.44%. Management raised 2026 free cash flow guidance to $12.5 billion and reaffirmed an operating margin target of 31.5%.

The Case for $350+

The bull thesis rests on Netflix’s ad business doubling to $3 billion in 2026, with over 60% of Q1 sign-ups in ad markets choosing the cheaper tier and advertiser count up 70% YoY to over 4,000. Membership crossed 325 million, yet penetration sits at less than 45% of broadband households globally.

Live events (NFL, Tyson Fury vs. Anthony Joshua), Netflix Playground gaming, the InterPositive GenAI acquisition, and a content slate including Greta Gerwig’s Narnia and David Fincher projects extend the runway. Of 51 covering analysts, 37 rate it Buy or better with only one Strong Sell. Our bull case scenario points to $353.86.

What Could Go Wrong

The bear case is real. NFLX trades at a 28x trailing P/E against fierce competition from Alphabet, Amazon, Apple, Disney, and TikTok. Q3 2025 EPS missed by 15.79% on a $619 million Brazilian tax charge, and another $700 million deposit shifts into 2026.

Polymarket traders assign a 61.5% probability that NFLX hits $85 in May 2026, with only 18% odds of finishing the week above $90. The EPS miss reflects investment timing and Brazilian tax noise, with operating income still growing 18.23%. Our bear case still pegs the 12-month outcome at $257.29.

What to Watch From Here

Our price target of $338.63 reflects a buy rating at 90% confidence. The tipping factor is forward EPS of $18.03 against a stock that has compressed nearly 22% over the past year despite a raised $12.5 billion FCF guide. The bullish path requires the ad tier to scale as guided and content amortization to ease in the back half. The cautious path holds if FX and Brazilian tax overhangs prove stickier than management signals.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $338.63 |

| 2027 | $680 |

| 2028 | $1,400 |

| 2029 | $2,500 |

| 2030 | $4,410.71 |

These projections track our base case five-year scenario and assume Netflix continues compounding ad revenue, expanding margins toward the 31.5% guide, and protecting pricing power. Material upside or downside hinges on the ad tier ramp, live event monetization, and FX.

Contact [email protected] for any questions or corrections.