The Alerian MLP ETF (NYSEARCA:AMLP) is the kind of income vehicle that gets ignored at retirement planning meetings, even though it pays more than twice the 4.6% available on a 10-year Treasury. For a 65-year-old with $300,000 earmarked for income, AMLP is the rare retail-accessible ETF that turns pipeline economics into a quarterly check. The reason most retirees overlook AMLP is simple: master limited partnerships sound like tax paperwork, and energy still scares people who lived through 2015 and 2020.

What AMLP actually owns

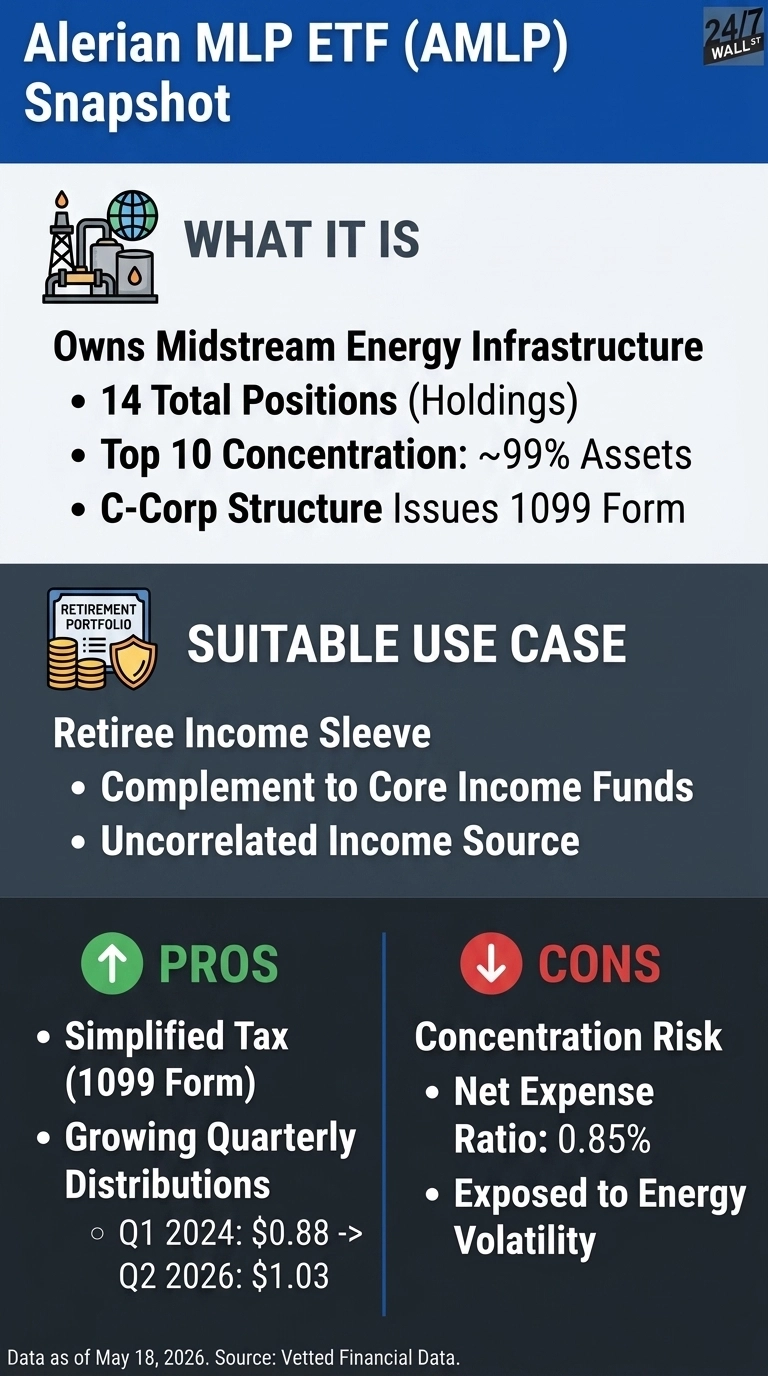

AMLP holds master limited partnerships that own physical midstream energy infrastructure: pipelines, storage terminals, and processing plants. These are partnerships rather than corporations, and they earn fee-based cash flows from moving hydrocarbons regardless of the commodity price on a given day. The fund is highly concentrated, but don’t worry if it all sounds complicated.

As far as specific ownership, Plains All American Pipeline, Sunoco, Energy Transfer, MPLX, Western Midstream, and Enterprise Products Partners each account for between 12% and 14% of assets, and the top 10 names account for 99% of net assets. There are 14 positions in total, so buying AMLP is essentially buying a handful of large pipeline operators in a wrapper.

That wrapper is the product’s real innovation. Owning MLPs directly forces investors to deal with complex K-1 partnership tax forms, multi-jurisdictional state filings, and dreaded unrelated business taxable income inside retirement accounts. AMLP bypasses that entire headache by structuring itself as a C-corporation. The fund absorbs the partnership paperwork internally and issues a clean 1099 to shareholders. This structural workaround is precisely why financial advisors who routinely veto K-1 investments are perfectly comfortable placing client capital into this fund.

Does the income story actually deliver

The cash flow is completely real. AMLP just wrapped up its latest distribution on May 13, 2026, handing investors 1.03 a share right on the heels of the 1.01 payout from February. When you add up the last four quarters, you are looking at 4.02 a share in total cash, which sets the trailing yield right at a juicy 7.5%.

That distribution growth has been on a really steady upward march. Payouts started at 0.88 in early 2024 and have climbed to today’s 1.03. The stock price has played along beautifully, too, mostly because WTI crude has been riding high in the triple digits, around 101 a barrel.

Pipeline volumes usually hold up just fine even when the economy hits a bump, but investor mood in this sector always hitches a ride with oil prices. Enjoy the run, but remember that a big part of recent gains is thanks to a crude tailwind that will eventually run out of steam.

The tradeoffs that matter

The structural cost of the 1099 wrapper is the biggest one. Because AMLP is a C-corp for tax purposes, it pays corporate-level tax on its share of MLP income, which creates a drag relative to owning the partnerships directly. The 0.85% net expense ratio is only the visible fee. The other realities:

- Concentration risk. Six names drive roughly four-fifths of the portfolio. A regulatory or operational problem at Energy Transfer or Enterprise Products Partners moves the fund meaningfully.

- Energy cyclicality. AMLP is equity exposure to the oil and gas value chain. It is not bond-like. Drawdowns during commodity dislocations can be severe.

- Tax character. Roughly 95% of distributions are ordinary income, with about 5% being returns of capital, which makes AMLP a better fit for tax-advantaged accounts than taxable brokerage accounts for high earners.

Who AMLP actually fits

AMLP makes sense as a 5% to 10% income sleeve for retirees who already hold a core dividend fund like Schwab U.S. Dividend Equity ETF (NYSEARCA:SCHD) or a covered-call product like JPMorgan Equity Premium Income ETF (NYSEARCA:JEPI) and want a third income source uncorrelated with the broad equity market. Investors who need stability of principal or cannot stomach a 30% drawdown when oil rolls over should look at shorter-duration bond funds instead.

Ultimately, the big takeaway is that the 7% yield is genuine, as is the energy-equity risk underlying it.

Contact [email protected] for any questions or corrections.