Synopsys (NASDAQ:SNPS | SNPS Price Prediction) runs the software that designs nearly every advanced chip on the planet. The electronic design automation leader sits at the center of the AI buildout, yet its stock has barely moved over the past year. It trades at $524.74, up 11.71% YTD but still 17% below its 52-week high.

CEO Sassine Ghazi told investors the company enters “2026 with an expanded portfolio, leadership positions across the business, and the most compelling roadmap in our history.” The market disagrees. Can shares hit $700 this year?

What’s Holding Synopsys Back

The Ansys acquisition broke the chart. Shares plunged from $617.91 in August 2025 to $389.83 by November as investors absorbed the debt load and Q3 FY2025 IP segment weakness. Ghazi admitted, “our IP business underperformed expectations.” Layer on U.S. export restrictions on China chip design software (~10% of revenue) and the stock faces a trust deficit.

One-year return: just 4.22%. Long-term debt sits at roughly $10 billion post-Ansys. With a beta of 1.245, this name swings hard on macro headlines. The recent 9.95% one-month bounce is encouraging, but trust must be earned back.

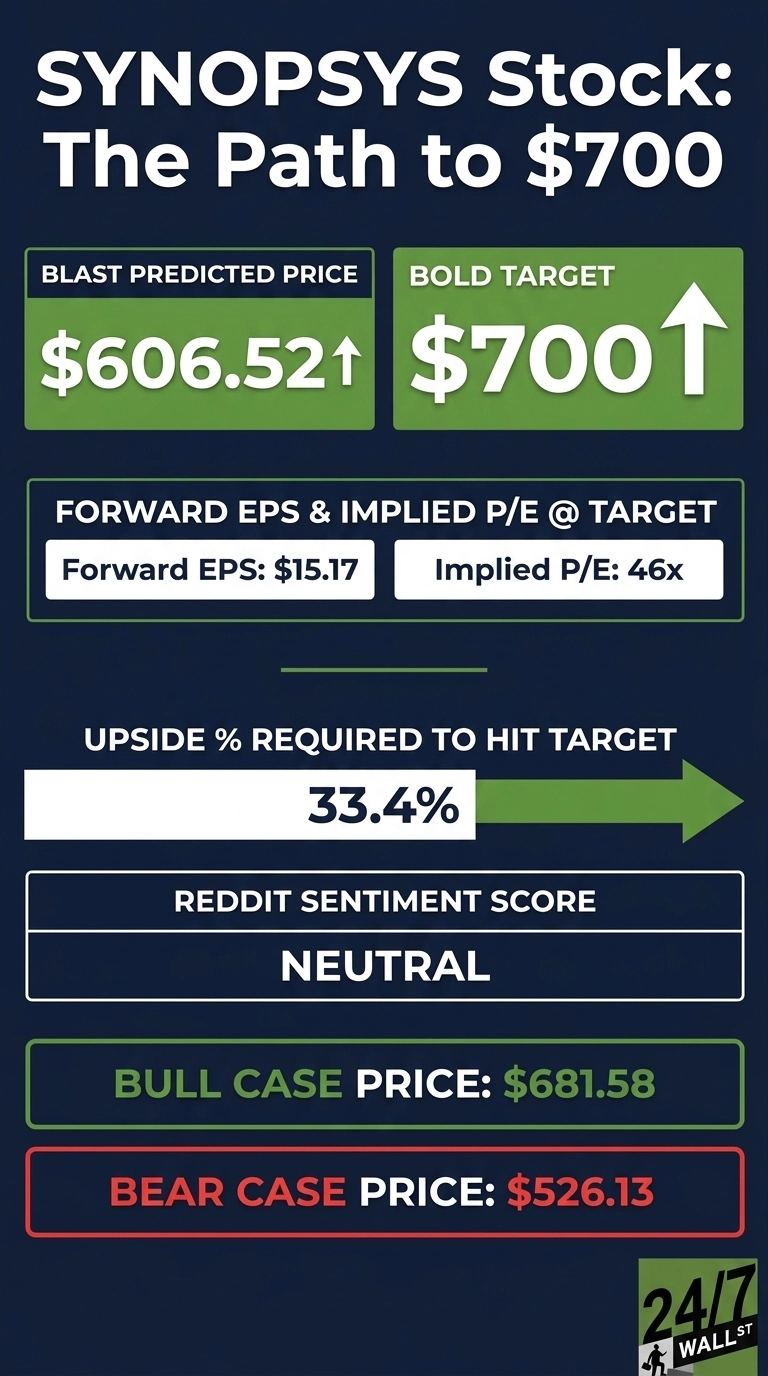

Wall Street Sees 3% Upside. Our Model Says 16%

Consensus target sits at $539.69, barely above today’s price. Ratings split: 2 Strong Buy, 15 Buy, 7 Hold, 1 Strong Sell. That works out to 68% bullish sentiment, constructive but not aggressive.

Our model is more optimistic. Base case lands at $606.52, implying 15.58% upside with a 90% confidence score. Bull case stretches to $681.58. Analysts appear anchored to past disappointments rather than the FY2026 earnings ramp. The $11.3 billion backlog is doing work that consensus ignores.

The Path to $700

Reaching $700 from $524.74 requires a 33.4% gain. That’s a big lift but within the stock’s historical volatility band.

With forward EPS of $15.17, a price of $700 implies a forward P/E of 46x. Our base case of $606.52 already implies 38x, meaning the bold target needs roughly 8x additional multiple expansion.

Is that achievable? The adjustment factor of 1.142 reflects strong technology sector momentum plus moderate analyst optimism. The bigger catalyst is product.

Ghazi described the NVIDIA partnership as delivering “15 to 20 times performance improvement for GPU versions” of EDA tools. He also stated, “AI isn’t disrupting our business; it’s amplifying our strategic advantage.” Q1 FY2026 showed 65.4% YoY revenue growth with EPS of $3.77, beating consensus by 5.98%. If Ansys synergies hit the $400 million revenue run rate target, EPS compression alone closes part of the gap.

Primary risk: any expansion of China export controls hits revenue and shatters the multiple expansion thesis.

Valuation Today vs Earnings Power

At $524.74 against forward EPS of $15.17, SNPS trades at roughly 35x forward earnings. The trailing P/E of 81 looks steep, but acquired intangible amortization ($504 million annually) distorts GAAP.

Shares sit mid-range against a 52-week band of $376.18 to $651.73. SNPS has returned 925.28% over ten years. The forward multiple is reasonable for a mission-critical AI infrastructure name with a $9.6 billion revenue run rate.

Berenberg raised the firm’s price target on Synopsys to $633 from $540 and keeps a Buy rating on the shares.

Is $700 Realistic?

$700 requires a 33.4% gain from here. It’s a stretch for calendar 2026, but not a fantasy.

Three things need to go right. First, Ansys cross-sell must show measurable revenue traction at the March Converge conference. Second, China revenue must stabilize rather than deteriorate. Third, agent engineer monetization must show up in deferred revenue. A deeper China crackdown would derail the thesis. We’ve outlined the blueprint for how Synopsys could reach $700 in 2026.

Contact [email protected] for any questions or corrections.