Synopsys (NASDAQ:SNPS | SNPS Price Prediction) has staged one of the more dramatic comebacks in semiconductor software, climbing 21.78% in the past month after a brutal stretch through late 2025. With the Ansys integration now showing up in the numbers and AI-driven chip design demand intact, our model points to further upside.

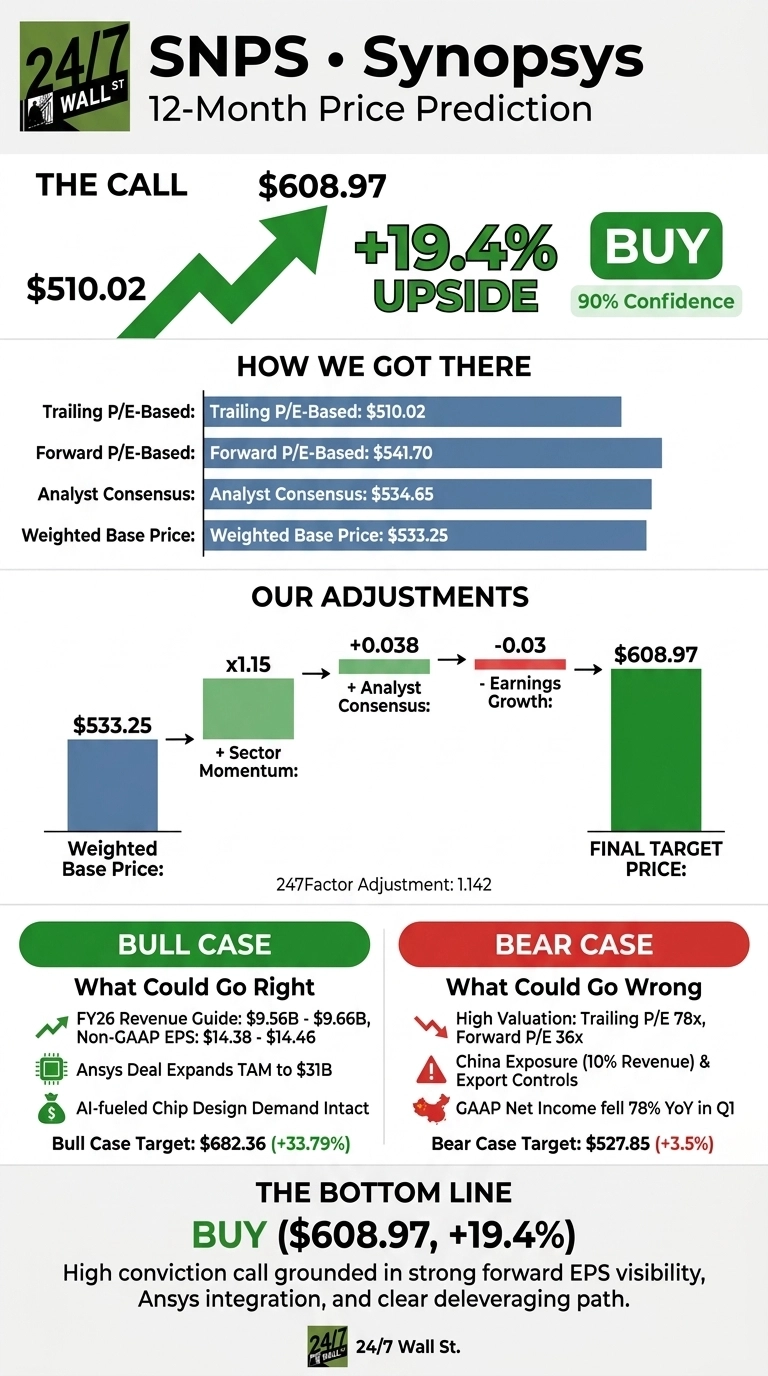

Our 24/7 Wall St. price target for Synopsys is $608.97, implying 19.4% upside from the current $510.02. We rate it a buy with 90% confidence, a high conviction call grounded in forward EPS visibility and a clear deleveraging path.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $510.02 |

| 24/7 Wall St. Price Target | $608.97 |

| Upside | 19.4% |

| Recommendation | BUY |

| Confidence Level | 90% |

From Q3 Selloff to a 22% One-Month Rally

Synopsys has whipsawed investors. The stock collapsed to $389.83 by November 2025 after a brutal Q3 FY25 miss, then clawed back to $510.02. Year to date, shares are up 8.58%, with the one-month surge of 21.78% reflecting renewed confidence in the Ansys story. The 52-week range runs from $376.18 to $651.73.

Q1 FY26, reported February 25, delivered revenue of $2.41 billion (up 65.4% YoY) and non-GAAP EPS of $3.77 against a $3.55 consensus, a 5.98% beat. Operating cash flow swung to $856.83 million from negative $67 million a year earlier, and management paid down $3.45 billion in long-term debt during the quarter.

Why Bulls See a Breakout Ahead

The bull case rests on FY26 guidance of revenue between $9.56 billion and $9.66 billion and non-GAAP EPS of $14.38 to $14.46, including roughly $2.9 billion in Ansys revenue.

CEO Sassine Ghazi said Synopsys has “the most compelling roadmap in our history” as AI fuels chip design R&D. The Ansys deal expanded the addressable market by 63% to $31 billion. Wells Fargo raised its target to $505 from $450 on May 14. Our bull scenario points to $682.36, a 33.79% total return.

The Risks Worth Watching

The bear case starts with valuation. Trailing P/E sits at 78, with forward P/E at 36. China accounts for roughly 10% of revenue and remains exposed to U.S. export controls. Morgan Stanley flagged growth deceleration, and Piper Sandler holds a Neutral rating with a $430 target.

GAAP net income fell 78.03% YoY in Q1, though bulls would argue this reflects $404 million in acquired intangible amortization and $118 million in restructuring, non-cash and non-recurring items that obscure underlying cash generation. The bear scenario lands at $527.85.

Synopsys Price Prediction 2026-2030

The 24/7 Wall St. price target of $608.97 reflects a buy rating at 90% confidence. The factor tipping the scale is cash flow visibility: $2.2 billion in expected FY26 operating cash flow plus a $2 billion repurchase replenishment.

The thesis strengthens if Q2 results land within the $2.225 to $2.275 billion revenue guide. It weakens if China export restrictions tighten further or Design IP margins fail to recover.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $608.97 |

| 2027 | $687.48 |

| 2028 | $745.00 |

| 2029 | $801.45 |

| 2030 | $880.97 |

These projections assume Synopsys continues executing on Ansys integration and AI-led EDA demand holds. Significant upside or downside could result from China export policy shifts or accelerated margin expansion through cost synergies.

Contact [email protected] for any questions or corrections.