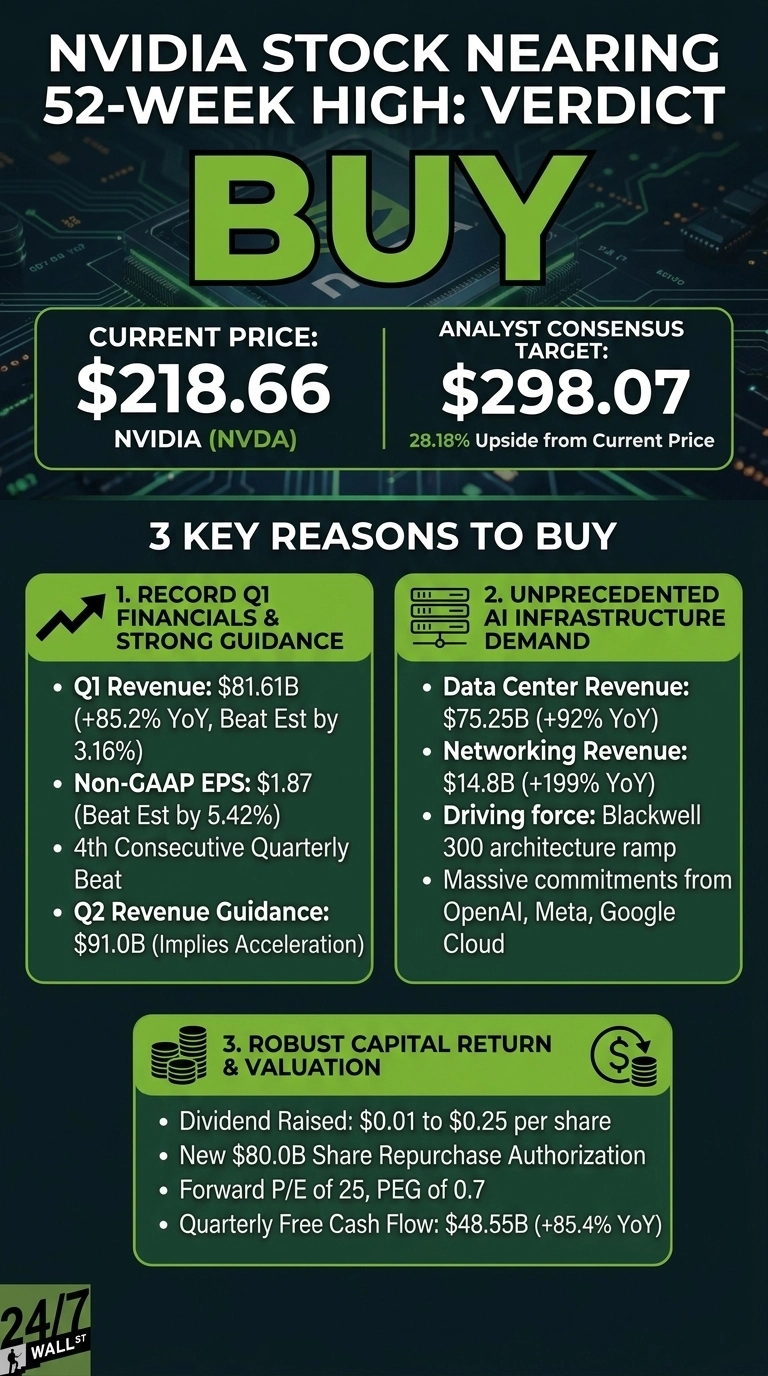

NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) trades at $218.66. With shares pressing toward a 52-week high of $236.26, the question is whether the AI infrastructure story still has room to run or whether expectations have caught up to the business.

Nvidia designs the GPUs, networking fabric, and software platforms powering virtually every serious AI deployment globally. The company sits at the center of what CEO Jensen Huang calls “the largest infrastructure expansion in human history,” with hyperscalers, sovereign clouds, and enterprises racing to build compute capacity.

Shares are up 17.38% year to date and 54.29% over the past year, driven by a Blackwell ramp that has reaccelerated revenue growth four quarters running.

Why the Blackwell Cycle Still Has Legs

Q1 FY2027 revenue hit $81.61 billion, up 85.2% year over year, beating the $79.12 billion estimate. Non-GAAP EPS of $1.87 topped the $1.77 consensus. Data Center revenue reached $75.25 billion (+92% YoY), and networking exploded 199% YoY to $14.8 billion.

Forward guidance is louder. Nvidia guided Q2 to $91 billion in revenue, excluding China Data Center compute. Management raised the dividend from $0.01 to $0.25 and authorized an $80 billion buyback. Multi-gigawatt commitments from OpenAI, Anthropic, Meta, and Google Cloud on Vera Rubin signal structural rather than cyclical demand.

Valuation is the surprise. Shares trade at a forward P/E of 25 and a PEG of 0.7, cheap for a company compounding earnings at this pace.

Why the Top May Already Be In

Concentration is the core risk. Roughly 50% of Data Center revenue comes from hyperscalers simultaneously building custom silicon. Amazon’s Trainium has scaled to a multi-billion-dollar business, and supply commitments now total $119 billion, a liability if AI capex flattens.

China is effectively zero. Q1 had no H20 shipments, versus $4.6 billion a year prior, and Q2 guidance assumes nothing from Chinese Data Center compute. Retail sentiment is flashing yellow: the Michael Burry “Fugazi” thread has recurred 20-plus times this month, and reports of H200 GPU rental prices falling 38% hint at softening spot demand.

Insider activity is unambiguous. Over the past three months, all 52 recent insider transactions were disposals, with a director still selling at $214 on May 27.

Why Patience Has Its Own Case

A Hold view is defensible. Polymarket’s most active June 2026 contract places the highest single probability (63.5%) on a $208 print, below today’s level. The composite sentiment index reads 63.49 (bullish, low confidence), and reasonable investors might wait for Q2 confirmation before adding.

What the Targets Say

Shares currently trade at $218.66 against an analyst consensus target of $298.07, implying 28.18% upside. Of 61 covering analysts, 58 rate it Buy, 2 Hold, and 1 Sell.

Valuation sits at a trailing P/E of 33 and a forward P/E of 25 on a $5.30 trillion market cap. NVDA’s 54.29% one-year return dwarfs the S&P 500’s roughly 28% gain over the same span, and the 11.4% one-month move shows momentum reaccelerating into the earnings report.

The Verdict

At $218.66, the bull case on NVIDIA looks well-supported by the fundamentals.

The path to appreciation is concrete. Q2 guidance of $91 billion implies sequential acceleration with zero China contribution. If Nvidia delivers and reiterates Rubin demand commentary, the stock could revalue toward the $298 consensus on the same forward multiple it carries today.

Risk/reward appears favorable for owners. A forward P/E of 25 on a business growing earnings 214.5% with 75% gross margins, $48.55 billion of quarterly free cash flow, and an $80 billion buyback is not stretched. The dividend hike from a penny to $0.25 signals management confidence in forward cash generation.

What could invalidate the thesis: a Q3 guide showing hyperscaler capex flattening, custom-silicon share gains turning material, or supply commitments outpacing bookings. Worth watching as Rubin sampling progresses and China policy evolves.

At $218.66, investors are paying a reasonable multiple for the platform every serious AI builder is standardizing on, with the next catalyst already on the calendar.

Contact [email protected] for any questions or corrections.