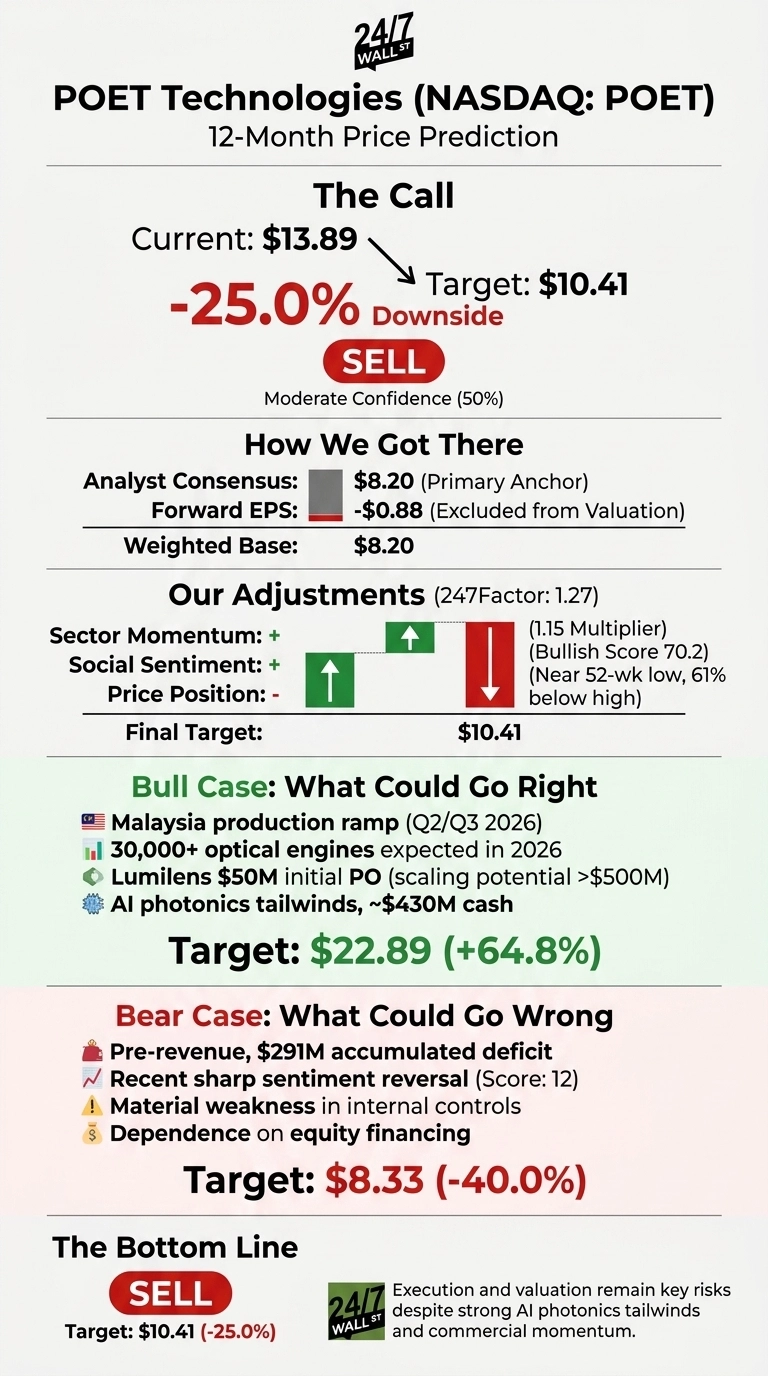

POET Technologies (NASDAQ:POET) trades at $13.89 as of June 2, 2026. Our 24/7 Wall St. price target for POET is $10.41 over the next 12 months, implying 25% downside from current levels.

Our recommendation is sell with moderate confidence of 50%, reflecting mixed signals between bullish analyst sentiment and a stretched price after a sharp May spike.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $13.89 |

| 24/7 Wall St. Price Target | $10.41 |

| Upside/Downside | -25.0% |

| Recommendation | SELL |

| Confidence Level | 50% |

Why We Could Be Wrong on POET

Our $10.41 Price Target sits below current levels. POET is one of the most divisive names in AI photonics, and real value could come from $50 million Lumilens purchase order scaling toward its $500 million potential or on-time 800G ramp in Malaysia. Treat our target as one datapoint among many.

From $4 to $14: A Year of Whiplash

POET is up 220.42% over the past year and 119.43% year to date, including a 90.01% surge in the past month. Shares spiked to roughly $15.97 in mid-May 2026 before pulling back to 61% below its 52-week high of $20.81.

The Q1 2026 report showed revenue of $503,389, beating consensus by 44.66%, while EPS came in at -$0.08 against a -$0.04 estimate.

The Case for $22 and Beyond

Our bull scenario lands at $22.89, a 64.8% return. The thesis rests on Malaysia executing on schedule: high-volume light source production in Q2 2026 and 800G optical engines in Q3 2026, with a target of 30,000+ optical engines shipped this year.

CEO Suresh Venkatesan called Lumilens “an important commercial milestone… supporting frontier AI infrastructure.” POET sits on roughly $430 million in cash, addressing an 800G transceiver market projected at $9.8 billion by 2032.

What Could Drag POET Back to $8

Our bear case lands at $8.33, a 40% drawdown. Revenue still measures in the hundreds of thousands per quarter, and POET carries a $291 million accumulated deficit with a material weakness in internal controls flagged in the 2024 audit.

Bulls counter that recent EPS misses are distorted by non-cash derivative warrant charges, including a $30.69 million Q4 charge that planned U.S. redomiciliation should largely eliminate. Even so, the gap between current revenue and a $2.4 billion market cap remains wide.

POET Price Prediction 2026-2030

Our 24/7 Wall St. price target is $10.41, recommendation is sell, and confidence is moderate at 50%. The key factor is the gap between POET’s current price and the lone analyst target of $8.20 after a 90% one-month run.

The bull thesis would gain traction if Malaysia hits its Q3 2026 800G milestone and Lumilens converts toward the $500M tier, while the bear thesis strengthens if shipment guidance slips or warrant accounting volatility returns.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $10.41 |

| 2027 | $9.60 |

| 2028 | $9.10 |

| 2029 | $8.75 |

| 2030 | $8.49 |

These projections assume POET continues executing on its current strategy. Significant upside could come from Lumilens scaling beyond $500 million, while downside risk hinges on Malaysia execution and continued equity dilution.

Contact [email protected] for any questions or corrections.