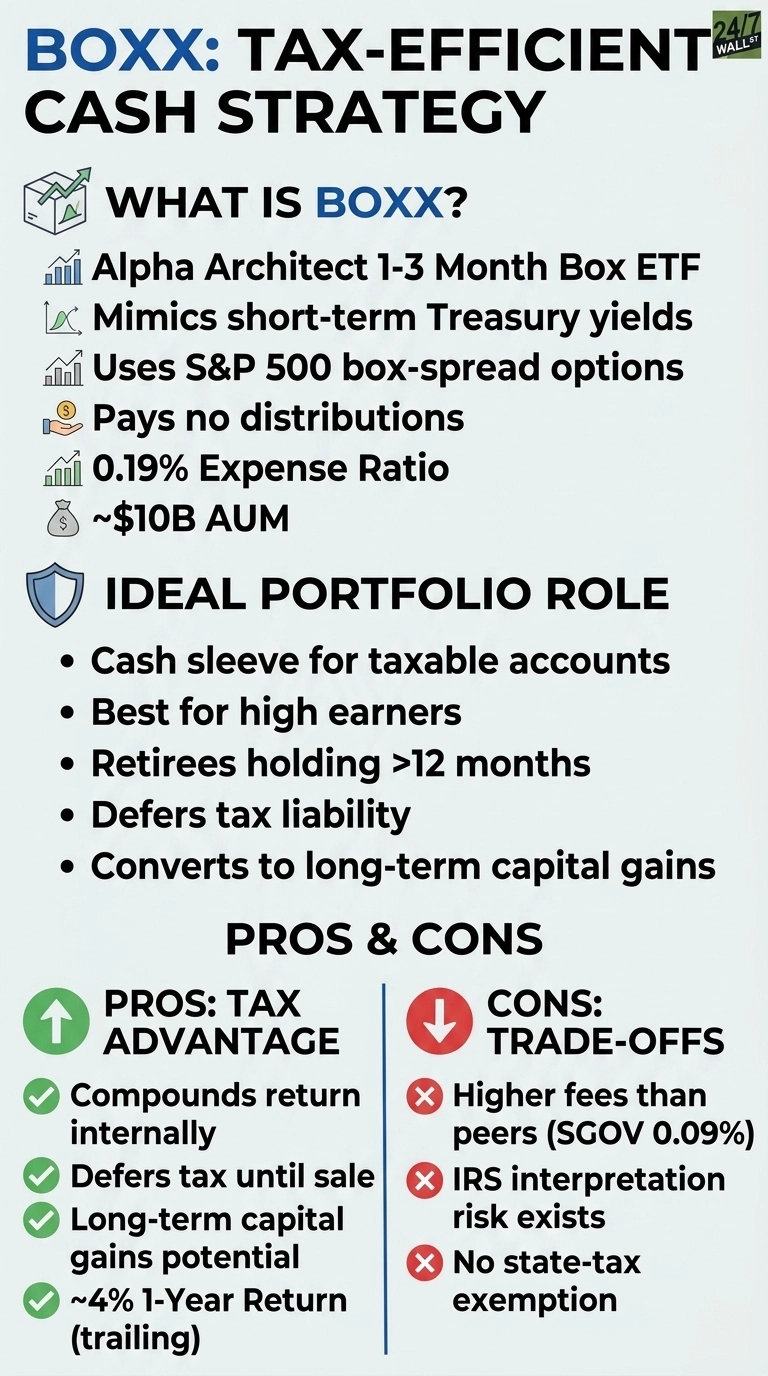

For a high earner sitting on idle cash, the choice between a money market fund and a Treasury bill ETF usually comes down to a few basis points of yield. Alpha Architect 1-3 Month Box ETF (NYSEARCA:BOXX) reframes the question by targeting the tax bill rather than yield. BOXX replicates short-term Treasury rates using S&P 500 options box spreads, then refuses to pay any distributions, allowing the entire return to compound in the share price until the investor sells. For a California retiree in a 50% combined marginal bracket, that structural quirk is what makes BOXX worth understanding.

The cash problem BOXX is built to solve

A retiree parking $500,000 in a traditional money market fund yielding 5% continuously generates ordinary income taxed at the highest federal and state rates every single year. SGOV and direct Treasury bills successfully strip out the localized state tax burden but still distribute monthly interest payments that are subject to heavy federal taxation. BOXX, with roughly $11.87 billion in total assets under management and a 0.19% expense ratio, instead uses long and short SPY option combinations carefully engineered so that the ultimate payoff at expiration matches the risk-free cash rate. Because these structural gains remain encapsulated within the fund and get systematically scrubbed through in-kind redemptions with authorized participants, retail shareholders never trigger an annual 1099-DIV. Holding positions for longer than twelve months converts that embedded yield entirely into highly favorable long-term capital gains.

How BOXX tracks short-term rates

Over the trailing year, BOXX returned about 4%, with shares moving from about $112 to almost $117. The iShares 0-3 Month Treasury Bond ETF (NYSEARCA:SGOV) returned about 4% over the same window, with an expense ratio of just 0.09%. The 3-month Treasury bill yields almost 4%, and the Fed funds upper bound sits at almost 4% after 75 basis points of cuts over the past year. BOXX is tracking the short end of the curve as advertised, with a slight edge from the box-spread structure, capturing rates closer to broker-financing levels than to T-bills.

The tax arithmetic is where the fund pulls ahead. Using the prompt’s California example, ordinary income tax on $25,000 of annual yield runs about $12,500, while the same gain harvested after a year inside BOXX is taxed as long-term capital gains at roughly $5,500. The annual savings of about $7,000 on a $500,000 position scale linearly with the position. At $1 million, the after-tax advantage works out to $10,000 to $20,000 per year compared with a money market fund.

What the holder gives up

- Higher fees than the cheapest cash ETF. SGOV’s 0.09% expense ratio is less than half of BOXX’s 0.19%. For a taxable account in a low-tax state, that fee gap can erode most of the benefit.

- IRS interpretation risk. Box-spread ETFs use a tax structure that has drawn regulatory attention, and the Treasury has periodically flagged listed-option strategies designed to convert ordinary income. A future ruling reclassifying the gains as section 1258 ordinary income would neutralize the core advantage.

- No state tax exemption. SGOV and direct T-bills are exempt from state income tax. BOXX is not. A muni money market like VMSXX may offer a higher after-tax yield to residents of California or New York in the very high tax brackets.

Who BOXX fits

BOXX functions beautifully as a specialized cash allocation sleeve for taxable brokerage accounts controlled by ultra-high earners in top-tier state and federal brackets, particularly retirees who can safely cross the 12-month boundary to process programmatic redemptions that carefully isolate their realized capital gains. Conversely, individuals deploying capital within IRAs, living in zero-tax states, or landing comfortably below the 24% federal tax threshold are inherently better served by using SGOV or structured Treasury ladders, where raw management-fee savings and direct local tax exemptions easily outpace the fund’s synthetic compounding mechanics. The product precisely executes its stated objective. The ultimate decision depends exclusively on whether an investor’s true marginal bracket warrants the structural friction of targeting pure tax alpha.

Contact [email protected] for any questions or corrections.