From Dead Money to AI Darling

For most of the past decade, Nokia (NYSE: NOK | NOK Price Prediction) was the patience trade nobody wanted. The Finnish telecom equipment maker spent years restructuring under former CEO Pekka Lundmark, cutting costs, and watching Ericsson, Huawei, and Samsung carve up the 5G market while shareholders received a thin dividend and not much else.

The pivot started in 2024 with the announcement of the acquisition of Infinera, a U.S. optical networking player that gave Nokia real exposure to data center connectivity. The deal closed in February 2025, and weeks later Justin Hotard, a former Intel data center executive, took over as CEO and repositioned the company around an “AI connectivity supercycle.” The real catalyst came in Q4 2025, when Nvidia made a $1.0 billion equity investment alongside an AI-RAN partnership. The stock reached three-year highs, and the narrative shifted.

Your $1,000, Three Different Stories

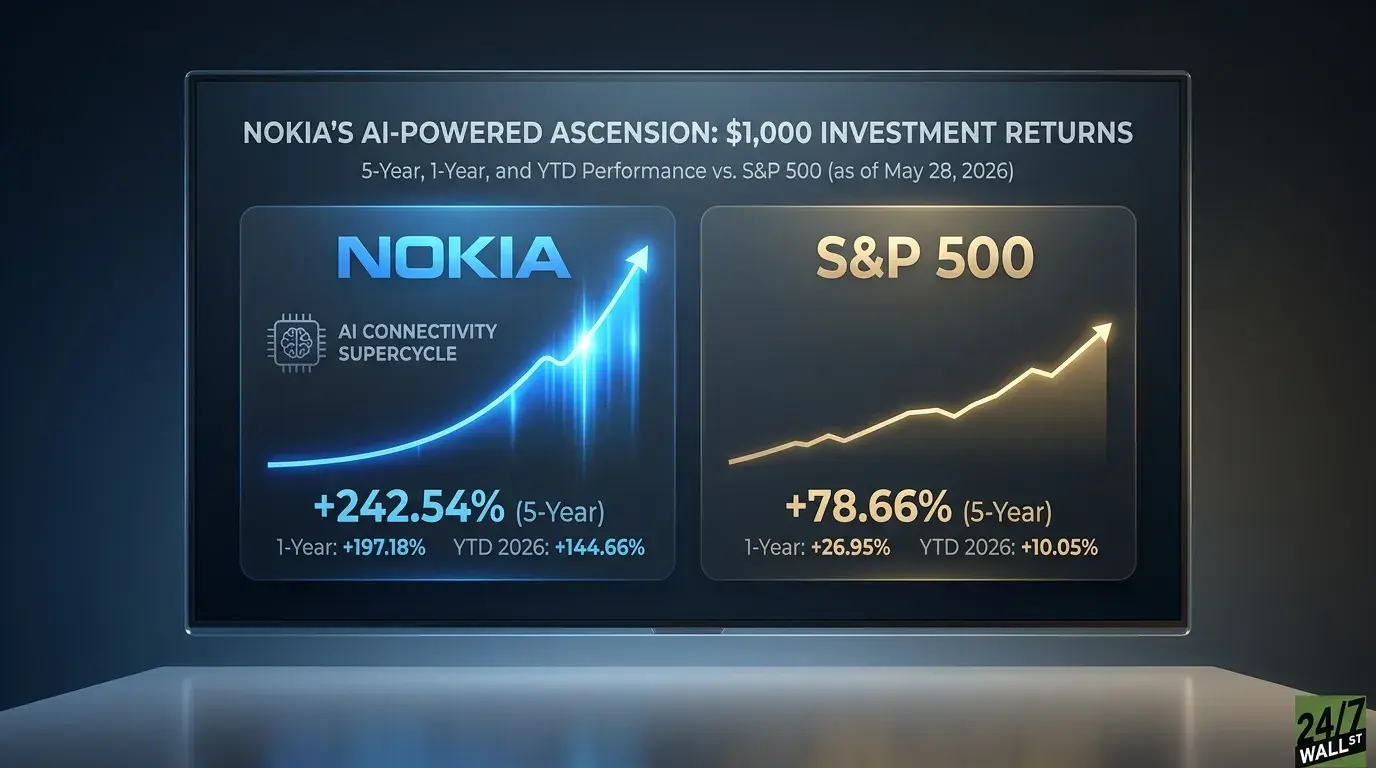

Here is what $1,000 invested in Nokia would be worth as of May 27, 2026:

| Time Period | Total Return | Value Today | S&P 500 Return |

|---|---|---|---|

| 5-Year | 242.54% | $3,425 | 78.66% |

| 1-Year | 197.18% | $2,972 | 26.95% |

| YTD 2026 | 144.66% | $2,447 | 10.05% |

Nokia crushed the S&P 500 across every window, but the win is heavily back-loaded. Almost all the five-year gain came in the past 12 months as the AI thesis took hold. Investors who held through years of flat trading were rewarded, while latecomers chasing the 46.3% one-month surge are paying significantly higher prices.

The Bull And Bear Case From Here

The bull case for Nokia rests on the AI-RAN partnership with Nvidia converting into hyperscaler design wins, Optical Networks continuing to compound (up 17% in constant currency in Q4 2025), and management hitting its 2028 target of €2.7 billion to €3.2 billion comparable operating profit. Ultimately, the bull case hinges on a re-rating from a telecom multiple to an AI infrastructure multiple.

The bear case centers on a trailing P/E near 98 and an analyst consensus price target of $12.90, which is well below the current price. Currency headwinds, declining Greater China revenue, and Infinera integration risk are all ongoing concerns, and the 52-week low of $4.00 serves as a reminder of how quickly sentiment can shift.

The investment thesis is compelling, even if the current entry point looks stretched. Watch the July 24, 2026, Q2 earnings report as the next key test of this valuation.

Contact [email protected] for any questions or corrections.