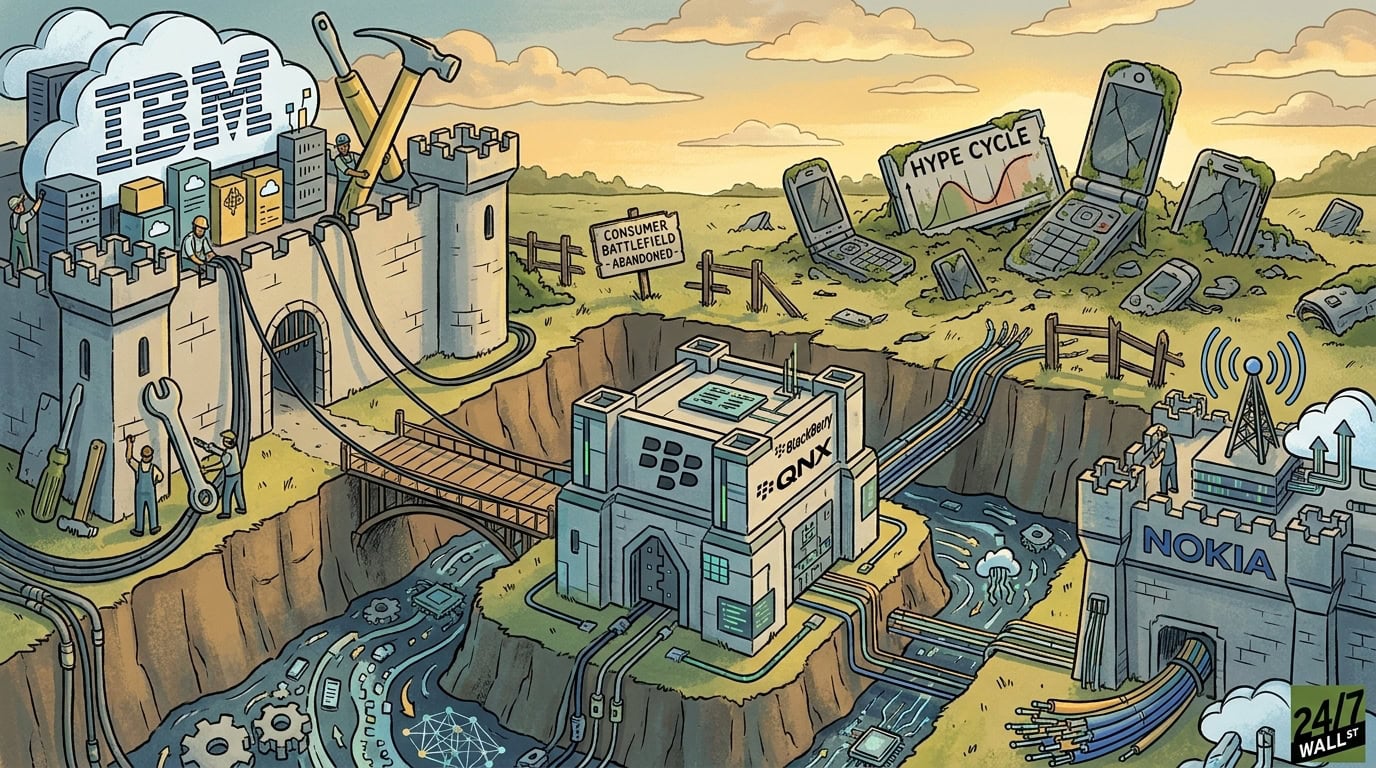

Although Wall Street typically buries its dethroned category kings without ceremony, three former tech titans have spent the past year clawing their way back into the investor conversation. BlackBerry (NYSE: BB) has vaulted 172.8% year to date, Nokia (NYSE: NOK | NOK Price Prediction) has piled on 114.8%, and International Business Machines (NYSE: IBM) still commands a $242.7 billion market capitalization after divesting Kyndryl and rebuilding around hybrid cloud. But the long memory of public markets says only one type of comeback actually endures. The historical pattern is unforgiving: fallen tech leaders survive when they abandon the consumer battlefield and rebuild around an enterprise moat, and they fail when they chase the next consumer hype cycle.

The textbook precedent is IBM itself. When Lou Gerstner arrived in 1993, the company was hemorrhaging cash as the PC era eroded the mainframe’s pricing power. His pivot away from boxes and toward services, software, and consulting became the template every fallen tech name has tried to copy. Satya Nadella ran a similar playbook at Microsoft a generation later by stepping away from the Windows-phone war and rebuilding around Azure. Apple’s 1997 reinvention stands as the rare consumer-side exception, and exceptions do not make policy. The verdict that the record delivers is consistent: picks-and-shovels enterprise suppliers tend to survive, while consumer-comeback bets usually do not.

IBM: The Original Blueprint, Running It Again

IBM is now attempting Gerstner 2.0. Arvind Krishna shed Kyndryl, paid $34 billion for Red Hat in 2019, and re-anchored the company on hybrid cloud, mainframes, and generative AI. Q1 2026 revenue rose 9.5% year over year, and the IBM Z mainframe line grew 51% as enterprises retooled for AI workloads. The stock trades at 23 times trailing earnings with a 2.6% dividend yield, and the company has raised its payout for 31 consecutive years. Over the past five years, IBM shares have returned 84.0%, a measured rerating rather than a euphoric one. Analysts carry an average price target of $293.89.

BlackBerry: The Cleanest Break From the Old Battlefield

BlackBerry sold its handset business long ago and re-emerged as an embedded-software and secure-communications pure play. Q1 FY27 revenue jumped 25.6% to $152.9 million, with the QNX segment delivering $72.3 million at an 86% adjusted gross margin. QNX now sits inside more than 275 million vehicles with a royalty backlog near $950 million, and the company has partnered with Nvidia on QNX OS for Safety 8.0 integrated with Nvidia IGX Thor. CEO John Giamatteo told investors, “We are no longer a company in transition. We are a growth company.” The catch lives in the multiple. BlackBerry trades at 96 times trailing earnings and 53 times forward earnings, against an analyst consensus price target of $6.43 while the stock changes hands above $10. The business is improving, but the valuation has run ahead of it.

Nokia: True Reinvention or Cyclical Telecom Rebound?

Nokia sold its handset arm to Microsoft in 2014, divested HERE maps, and now positions itself as a telecom and AI-infrastructure supplier. Q4 2025 revenue of $7.12 billion beat consensus by 17.0%, with Optical Networks revenue of $2.8 billion, soaring on AI and cloud demand following the Infinera acquisition. Nvidia took a $1 billion equity stake as part of an AI-RAN partnership. The reinvention case, however, is only partial. FY25 net income still fell 49% to $737 million, and the stock trades at 87 times trailing earnings against an analyst price target of $14.89. The optical and IP-routing lines look structural; the mobile-networks legacy still moves with carrier capex cycles.

The Ranked Verdict

Score each name against the Gerstner survivor profile, the test of whether a company has abandoned the old consumer field and rebuilt around a durable enterprise moat—and a ranking emerges:

- IBM. Closest match. It wrote the playbook, scaled it, and is running it for a second cycle with mainframes and generative AI as the wedge. A 35.8% return on equity and three decades of dividend hikes are the receipts.

- BlackBerry. The cleanest narrative break from its old consumer identity, but the smallest scale and the richest multiple. The QNX thesis has substance; the price now demands flawless execution. Recent filings show a genuine business inflection.

- Nokia. Mid-pivot. Optical and AI-RAN are the right adjacencies, yet the mobile-networks legacy still trades on telco capex. Treat part of the rerating as cyclical until the structural mix proves otherwise.

Long term, Wall Street still rewards companies that pick a durable enterprise lane and stay in it. The historical record says investors who confuse a cyclical bounce with a structural reinvention tend to learn the difference the expensive way. The past three decades of fallen-titan comebacks suggest the survivor profile is built quarter by quarter, not bought in a single rerating.

Contact [email protected] for any questions or corrections.