SoFi CEO Anthony Noto has been quietly putting his own money to work in his company’s stock all spring. According to Form 4 filings, Noto made open-market purchases of SoFi Technologies (NASDAQ: SOFI | SOFI Price Prediction) common stock on March 2, March 17, May 8, and May 11, 2026, accumulating a total of 116,323 shares at prices ranging from $15.73 to $17.88. The most recent buys, two purchases of roughly $250,000 each in mid-May, came as the stock traded near multi-month lows.

The pattern matters because Noto bought lower each time. He paid $17.8842 in early March, then stepped in again at $15.7305 on May 8 and $16.0039 on May 11. With SoFi down 38.24% year to date through May 27 and closing at $16.17, the CEO has been adding into the selloff with conviction. Routine RSU vesting and tax-withholding sales by other executives in March and May are standard compensation mechanics, distinct from discretionary signals.

The Thesis Noto Appears to Be Underwriting

Q1 2026 results gave him plenty to point to. Revenue hit $1.10 billion, GAAP net income jumped 134.45% year over year to $166.7 million, and adjusted EBITDA reached $339.9 million at a 31% margin. Loan originations set a record at $12.18 billion, up 68% year over year. Members grew 35% and cross-buy reached 43%, the metric Noto prioritizes most because it reduces customer acquisition costs.

On the Q1 call, Noto framed the company’s position bluntly: “Our strategy and execution continue to be unmatched by any company I can think of at our scale and put SoFi in a class of one.” He also flagged the digital-assets push, noting that “Our strategic entry into new areas like digital assets alongside the strong growth in our existing businesses are strengthening and diversifying our platform.” SoFiUSD, the Mastercard settlement partnership, and Big Business Banking turn the deposit base (now $40.24 billion) into an enterprise platform.

The catch is the guidance. Management held FY2026 adjusted EPS at about $0.60 partly because the macro setup deteriorated. Noto told CNBC’s Mad Money on April 29: “We did not raise the full year guidance because when we originally gave it, we were anticipating at least 2 Federal Reserve rate cuts. Now we’re assuming no rate cuts.”

The Real Risks

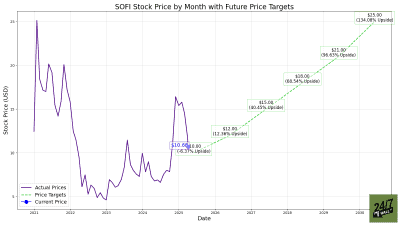

The bear case is credible. The Technology Platform segment fell 27% year over year after a large client departure, personal loan charge-offs ticked up to 3.03% from 2.80%, and the consensus analyst price target stands at just $21.10, with 12 hold and 4 sell or worse ratings versus 8 buy ratings. The forward P/E of 26 already prices in growth, and a beta of 2.126 means any macro wobble hurts.

Verdict

Noto’s buying is a credible signal backed by his own cash; he is purchasing shares while the stock trades well below its 200-day moving average of $23.33, and the operating numbers back the conviction. For a retirement-focused investor, the real question is whether the thesis (durable deposit funding, accelerating cross-buy, and an optionality kicker from stablecoin infrastructure) justifies owning a high-beta financial through a no-rate-cut year. The risk/reward improves at these prices, but position sizing should respect the volatility Noto himself is buying into.