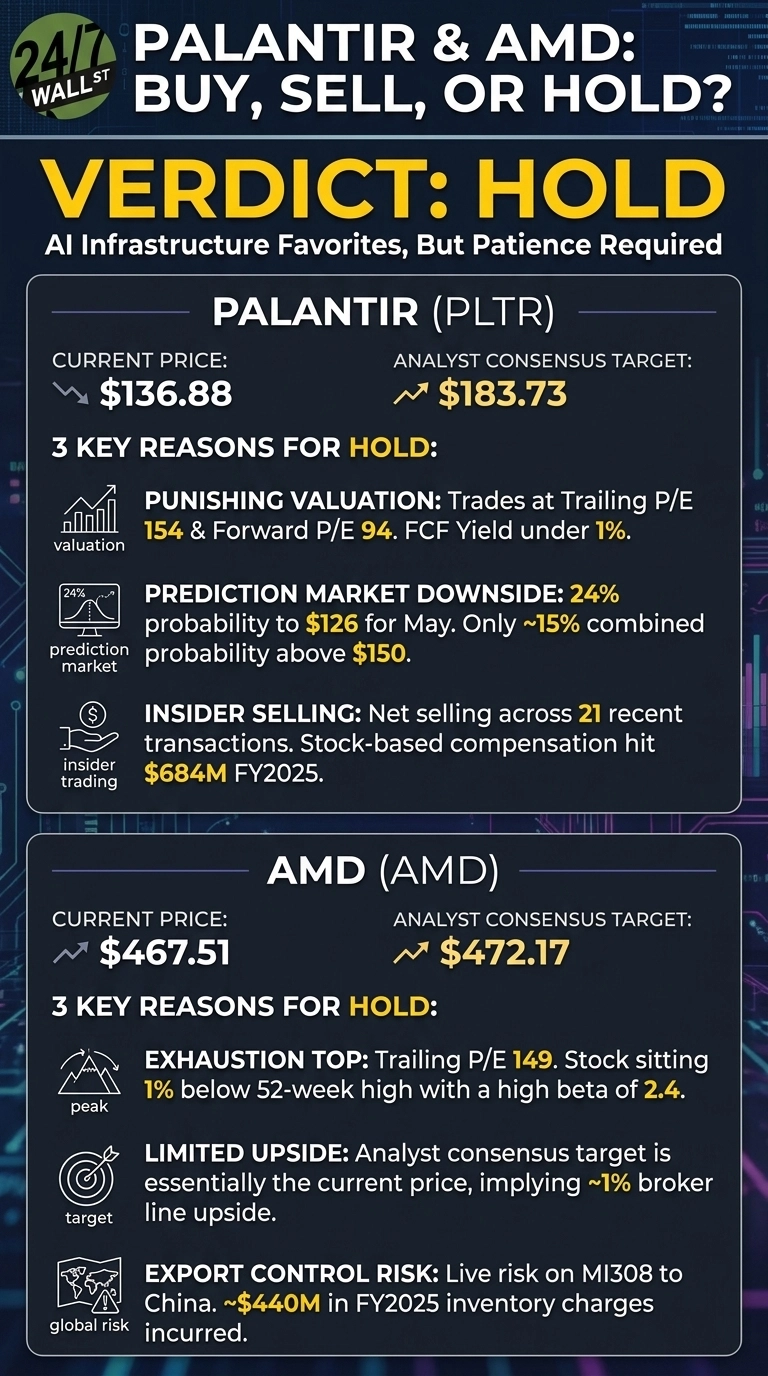

Palantir (NASDAQ:PLTR | PLTR Price Prediction) at $136.88 rates a hold, and AMD (NASDAQ:AMD) at $467.51 rates a hold, according to our analysis. Both are AI infrastructure favorites, but each has reached a price where the easy money has been made and the next leg requires fresh proof.

Palantir builds the operating layer for governments and large enterprises deploying AI. Its stock has cooled, falling 10.31% in the past month and 22.99% year to date, trailing the S&P 500’s roughly 9% YTD gain.

AMD, the GPU and EPYC challenger to NVIDIA, has gone the other way, surging 54.06% in a month and 322.28% over one year, parked within 1% of its 52-week high.

Palantir: Why Bulls Want In Here

Q4 2025 was a fundamental statement. Revenue grew 70% year over year to $1.406 billion, U.S. commercial revenue jumped 137%, and the Rule of 40 score hit 127%.

CEO Alex Karp called the company “an n of 1”. Guidance for 2026 calls for 61% revenue growth and U.S. commercial growth of at least 115%. Free cash flow guidance of $3.93 billion to $4.13 billion implies real, GAAP-profitable AI monetization.

Palantir: Why Bears See a Trap

The valuation remains punishing. PLTR trades at a trailing P/E of 154 and a forward P/E of 94, with FCF yield under 1%. The Polymarket crowd assigns a 24% probability to $126 for May and only roughly 15% combined probability to prices above $150. Insider activity is net selling across 21 recent transactions, and stock-based compensation hit $684 million for FY 2025.

Palantir: Why Waiting Wins

At $136.88, our analysis rates Palantir a hold. The business is executing at a level few software companies ever reach, but the multiple still demands flawless execution every quarter. The AI fair-value model pegs base case at $152.44, only modest upside, while the analyst consensus target of $183.73 implies about 34% upside, though targets remain estimates rather than certainties.

A pullback toward the prediction market’s $126 zone, or a clean Q2 beat with reaccelerating U.S. commercial TCV, would shift the setup more favorably. Until then, holding is reasonable while adding aggressively at these levels appears premature.

AMD: Why Bulls Are Still Loading

Q1 2026 was a step-change. Revenue rose 37.9% to $10.25 billion, Data Center revenue grew 57% to $5.78 billion, and free cash flow exploded 253% to $2.57 billion. The OpenAI and Meta partnerships for up to 6 gigawatts each of AMD GPUs, plus Oracle’s planned 50,000-GPU Helios supercluster, establish AMD as the second credible AI accelerator vendor. Q2 guidance of $11.2 billion points to 46% YoY growth.

AMD: Why Bears See an Exhaustion Top

The stock has tripled in a year and now trades at a trailing P/E of 149, sitting 1% below the 52-week high with a beta of 2.4. The prediction market’s implied target is $425.57, suggesting roughly 9% downside, while sentiment has weakened with a 7-day trend change of -16.78. Export-control risk on MI308 to China remains live after $440 million in FY2025 inventory charges.

AMD: Why the Right Move Is Patience

At $467.51, our analysis rates AMD a hold. The analyst consensus target of $472.17 is essentially the current price, leaving about 1% upside on the broker line despite 37 Buy and 13 Hold ratings with zero Sells. The AI base case projects $517.26, but the bear case is $391.41, a sharper drop than most holders are positioned for.

A Helios ramp ahead of schedule, MI450 share gains versus Blackwell, or a clean China-export resolution would improve the setup. A single soft Data Center quarter would meaningfully weaken it. Today sits between those outcomes.

Contact [email protected] for any questions or corrections.