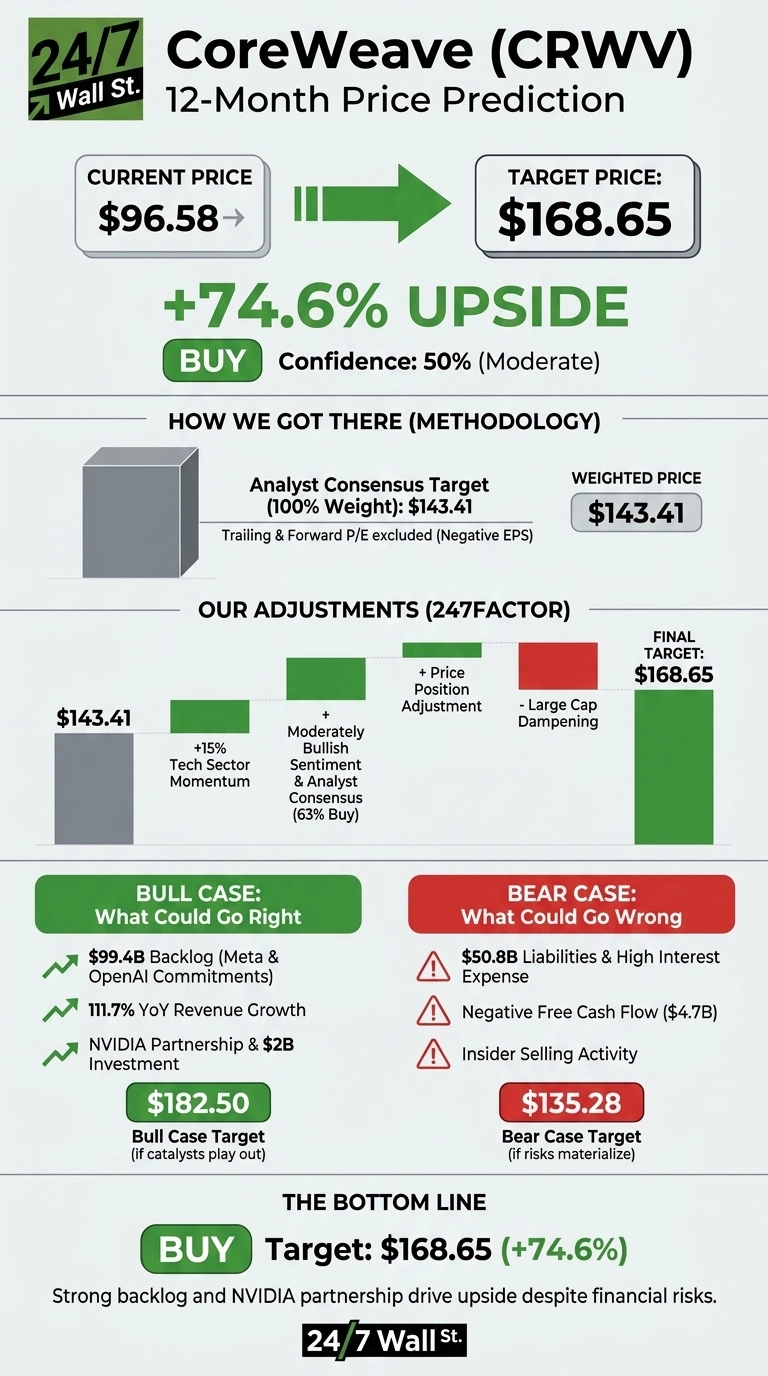

CoreWeave (NASDAQ:CRWV) has had a violent ride since its March 2025 IPO, and the recent pullback has reset the risk/reward in shareholders’ favor. With the stock at $96.58 after a 18.12% drop over the past week, our 24/7 Wall St. price target for CoreWeave is $168.65, implying roughly 74.62% upside over the next 12 months. The model rates the stock a buy with moderate conviction.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $96.58 |

| 24/7 Wall St. Price Target | $168.65 |

| Upside | 74.62% |

| Recommendation | BUY |

| Confidence Level | 50% |

A Rough Summer Has Created the Setup

CoreWeave is down 38.9% over the past year, yet still 34.87% higher year to date.

The Q1 2026 report on May 7, 2026 showed revenue of $2.08 billion, up 111.69% YoY and beating estimates, though EPS of -$1.40 missed the -$1.2042 consensus on a $740 million net loss.

Since then the stock has absorbed Nasdaq-100 inclusion on June 22, 2026, a $3.25 billion senior notes offering, and persistent insider selling by CEO Michael Intrator, including 307,692 shares for $32.87 million on June 23.

Why Bulls See a Breakout Ahead

The bull thesis is built on backlog. CoreWeave ended Q1 2026 with $99.4 billion in revenue backlog, including a $21 billion Meta (NASDAQ:META | META Price Prediction) commitment and total OpenAI commitments of $22.4 billion. Jim Cramer floated on June 19, 2026 that the real backlog could be materially larger than disclosed.

Active power surpassed 1 GW, with management targeting more than 8 GW by 2030. NVIDIA (NASDAQ:NVDA) has a $2 billion equity stake and $8.5 billion delayed draw term loan signal an unusually deep strategic partnership. Cantor Fitzgerald reiterated a Buy with a $167 target on June 12, 2026. A bull-case path takes shares to $182.50 within 12 months.

The Risks Worth Watching

The bear case starts with the balance sheet. Total liabilities sit at $50.81 billion, quarterly interest expense doubled YoY to $536 million, and free cash flow ran to -$4.71 billion on $7.7 billion in capex. A securities fraud class action over alleged data center construction delays remains outstanding, and insider sales across the C-suite have been heavy.

Bulls would counter that the capex is the business: each new gigawatt is contracted revenue, and operating cash flow already swung to $2.98 billion in Q1. Still, a bear-case path of $135.28 assumes margin recovery slips and rates stay elevated.

The Setup Here, With Eyes Open

The 24/7 Wall St. price target of $168.65 is a buy call at 50% confidence, and the tipping factor is the backlog-to-power conversion story that no peer can match.

The bull thesis strengthens if Q2 shows adjusted EBITDA margins holding above 60% and interest coverage stabilizing. The thesis weakens if insider selling accelerates further or the class action produces damaging discovery. On balance, the risk/reward near $96 has improved relative to the IPO-era valuation.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $168.65 |

| 2027 | $215.00 |

| 2028 | $285.00 |

| 2029 | $360.00 |

| 2030 | $440.00 |

These projections assume CoreWeave continues converting backlog into revenue and reaches its 8 GW power target. The 2030 figure aligns with our 5-year base-case model output of $440.66. Significant downside could result from an AI capex slowdown or refinancing stress.

Contact [email protected] for any questions or corrections.