Meta Platforms (NASDAQ:META | META Price Prediction) just reported one of the strangest quarters in mega-cap tech. Revenue grew 33.08% to $56.31 billion, advertising surged 33% year-over-year, and CEO Mark Zuckerberg told investors “We’re on track to deliver personal superintelligence to billions of people.”

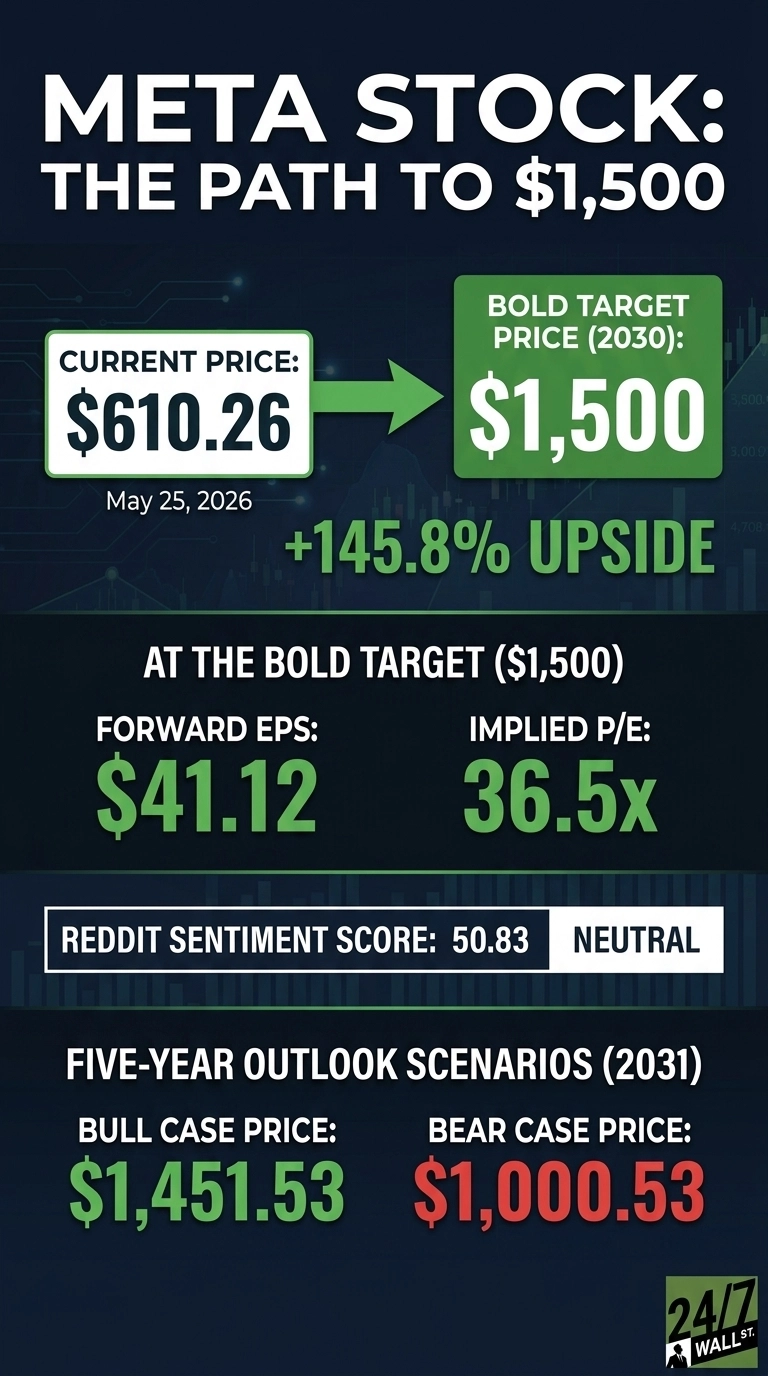

Yet shares are down 7.47% year-to-date and sit at $610.26. The question I want to answer: can Meta reach $1,500 by 2030?

What’s Holding Meta Back Right Now

The headwind is the capex bill. Meta raised its 2026 capital expenditure guide to $125 to $145 billion, up from the prior $115 to $135 billion range. That is a massive step up from $72 billion in 2025. Add in $162 to $169 billion in total 2026 expenses and Reality Labs bleeding another $4.03 billion in Q1 alone, and the market gets nervous.

The price action reflects that anxiety. Shares are down 9.55% over the past month and 3.84% over one year. With a beta of 1.243, every wobble in AI sentiment gets amplified here. Youth-related litigation trials in 2026 and EU regulatory pressure on personalized advertising add to the overhang.

Wall Street Sees 35% Upside. Our Model Sees More

The Street is loud and bullish. Nine Strong Buys, 47 Buys, seven Holds, and zero Sells. 89% of analysts sit bullish, with a consensus target of $826.60.

Our model goes further on a five-year horizon. The base case lands at $1,561.57 by May 2031, with the bull scenario at $1,451.53 and bear at $1,000.53. Confidence is rated high.

My read: analysts are anchoring on a one-year target while underweighting the cumulative effect of 62.4% earnings growth compounding through 2030.

The Path to $1,500 Per Share

Reaching $1,500 from today’s price of $610.26 would require a gain of 145.8%. Spread over roughly four years to 2030, that works out to a mid-20s annualized return. Aggressive but credible.

Here is the P/E math. With forward EPS of $41.12, a $1,500 price implies a forward P/E of 37x. Our base case already implies 18x, meaning the bold target requires roughly 18x of additional multiple expansion. That is the heavy lift.

The case for multiple expansion rests on EPS scaling faster than the market expects. Q1 EPS hit $10.44, a 56.79% beat. Zuckerberg called Q1 “a milestone quarter with strong momentum across our apps and the release of our first model from Meta Superintelligence Labs.”

If Superintelligence Labs monetizes, multiple expansion follows. The primary risk is Reality Labs and capex execution swamping ad-business cash flow.

Where Meta Trades Today vs Its Earnings Power

At $610.26, Meta trades at a forward P/E of roughly 15x. That is cheap for a business compounding revenue at 33% with 41.4% operating margins. Shares sit 4% off the 52-week high of $794.38 and well above the $520.26 low. The 10-year return is 422.52%. If you believe AI capex translates into durable EPS, today’s multiple is the entry point that makes 2030 math work.

Is $1,500 Realistic? Here’s My Take

Reaching $1,500 by 2030 requires a 145.8% gain. My honest verdict: a stretch, but a credible one.

Three things need to go right. Advertising growth has to stay in the high teens or better, Meta Superintelligence Labs needs to produce a real monetizable product, and capex digestion must not crater free cash flow.

A youth litigation verdict or a regulatory mandate against personalized ads would derail it fast. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Meta Platforms could reach $1,500 in 2030.

Contact [email protected] for any questions or corrections.