Live: Will Palo Alto Networks Keep Soaring After Q3 Earnings Tonight?

Quick Read

-

PANW has beaten estimates 5 straight quarters yet still averages a 3% earnings-day decline, putting enormous pressure on tonight's forward guidance.

-

Next-Gen Security ARR is the key metric to watch, with a guided jump from $6.3B to nearly $8B reflecting the CyberArk acquisition close.

-

At a forward P/E near 83 with a 96% predicted beat probability, PANW may need to exceed already elevated expectations just to avoid a selloff.

Act now: the analyst who called NVIDIA in 2010 just named his top 10 AI stocks — and Palo Alto Networks didn't make the cut. Grab the names FREE today.

Live Updates

Palo Alto Networks Q3 Earnings Coverage Wrap-Up

That wraps up our initial coverage of PANW’s Q3 results. Thank you for stopping by!

Surprises That Came Out of Palo Alto's Q3 Earnings Results

What Wasn’t Priced In

Positive surprises. Revenue of $3.00B outran management’s own 28-29% growth guide, landing at 31.15%. NGS ARR hit $8.1B, up 60%, well above the 56% guided pace. Free cash flow jumped 40.61% to $788M, with TTM adjusted FCF margin expanding 430 basis points.

Negative surprises. GAAP operating income flipped to a $183 million loss from $219 million of profit a year ago. Gross profit grew just 21.46%, lagging revenue by nearly ten points and signaling acquisition-driven margin compression.

Adjustment to watch. CyberArk and Chronosphere added $388 million in revenue, meaning the organic-versus-inorganic split is the swing factor analysts will recut tonight.

PANW's Q4 Guidance Raise is Big News for Investors

Guidance Bombshell: The Q4 Raise That Matters

The headline surprise is acceleration, not deceleration. Q4 revenue was guided to $3.345B–$3.355B, implying 32% YoY growth, a step up from Q3’s 31.15% print. Q4 EPS of $0.96–$0.98 sits well above the Street’s implied Q4 setup.

The FY26 raise is the real bombshell. Revenue moved to $11.415B–$11.425B from $11.28B–$11.31B, EPS climbed to $3.77–$3.79 from $3.65–$3.70, and adjusted FCF margin lifted to 37.5% from 37%.

Key assumptions: accelerating organic bookings, CyberArk and Chronosphere integrating ahead of plan, and AI security urgency. Q4 NGS ARR guidance of $8.90B–$8.95B sustains the 60% YoY trajectory, the metric bulls needed to see extended into FY27.

Does PANW's 8% Pop After Q3 Earnings Make Sense?

Does the 8% Pop Make Sense?

The reaction looks stretched relative to the magnitude of the beat. Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) topped revenue by 2% and EPS by 6%, solid but not blowout numbers for a stock already up 65.94% in a month with an RSI of 83.71.

Context matters: The average earnings-day move across the last five beats was -3.35%, and prediction markets barely budged, with the $8.5B Next-Gen Security ARR threshold holding at 2.7%.

The analyst consensus target sits at $230.82, well below the $323 price the stock soared to after earnings. It’s likely analysts will adjust their price targets higher following these strong Q3 results, but much of the good news may already be priced into the stock.

The market is focused on 31% revenue growth and CyberArk-fueled acceleration, treating this as a guidance-raise event.

PANW's Q4 Guidance Tops Street Estimates as Earnings Call Kicks Off

With the earnings call starting at 4:30 PM ET, attention shifts to the forward setup. Management guided for Q4 revenue to reach $3.345B–$3.355B, implying 32% YoY growth, with non-GAAP EPS of $0.96–$0.98 and NGS ARR reaching $8.90B–$8.95B. Full-year FY26 revenue was set at $11.415B–$11.425B with adjusted FCF margin of 37.5%, on track toward the 40% target by FY28.

CEO Nikesh Arora framed the quarter as evidence that “AI frontier advancements“ are reshaping cyber demand. Investors will listen for cadence on CyberArk and Chronosphere integration, plus commentary on the $517 million share-based comp charge weighing on GAAP profitability.

What Investors are Looking for PANW's Q3 Earnings Call to Deliver

The Palo Alto Networks (NASDAQ:PANW) 4:30 PM ET call is where guidance does the heavy lifting. Management already lifted FY26 revenue to $11.415B–$11.425B and EPS to $3.77–$3.79, with Q4 NGS ARR pegged at $8.90B–$8.95B. CEO Nikesh Arora typically guides conservatively, then raises, a pattern visible across three sequential FY26 hikes.

Bullish call commentary: organic bookings growth quantified above the $388M M&A contribution, FCF margin tracking toward the 40% FY28 target, and an AI security TAM expansion.

Bearish: any hedging on CyberArk (NASDAQ:CYBR) integration, share-based comp creep beyond $517M, or NGS ARR commentary that fails to extend the 60% YoY trajectory into FY27. At 83x forward earnings, the stock has high expectations baked into the price.

PANW's Backlog Just Hit $18.4 Billion

Palo Alto Networks ended the quarter with $18.4 billion in remaining performance obligations, up 36% year over year. Management expects that figure to climb to as much as $21.0 billion next quarter.

Revenue increased 31% year over year to $3.0 billion, while management guided for another quarter of roughly 32% revenue growth. Palo Alto’s position at the center of enterprise AI security spending continues to strengthen as companies deploy AI at scale.

The company’s backlog is growing faster than revenue, providing strong visibility into future growth. Next-Generation Security ARR reached $8.1 billion, up 60% year over year, as customers expanded spending across cloud, security operations, AI, and identity security offerings.

Palo Alto Networks Q3 Earnings Are Out - Stock Rips 12% Following Results

Palo Alto Networks just reported earnings, with shares initially rising about 12% following the release. Here are the key numbers:

- Revenue: $3.00B vs. $2.94B expected

- Adjusted EPS: $0.85 vs. $0.80 expected

Quick read:

- Palo Alto delivered a double beat, topping revenue expectations by 2% and earnings estimates by 6%.

- Revenue grew 31% year over year to $3.0 billion, showing continued strong demand for the company’s cybersecurity platform despite an already large scale.

Customer Consolidation is Becoming Increasingly Meaningful for Palo Alto Networks

Palo Alto Networks’ strategy is increasingly shifting to becoming the primary cybersecurity vendor for large enterprises, replacing multiple point solutions with a single platform.

That strategy appears to be gaining traction. Last quarter, the number of customers spending more than $5 million annually grew 48%, while customers spending over $10 million rose 50%. Those figures suggest some of the largest enterprises are standardizing on Palo Alto’s platform rather than spreading spending across multiple vendors.

For investors, that matters because larger platform relationships tend to be stickier, create more cross-selling opportunities, and make it harder for competitors to win business.

Palo Alto's $16 Billion Backlog Suggests Demand Remains Strong

One of the most important numbers to watch in Palo Alto Networks’ Q3 earnings report tonight will be remaining performance obligations, or RPO.

The cybersecurity giant exited last quarter with roughly $16 billion in RPO and more than $6.3 billion in annual recurring revenue, providing visibility into future growth. Strong RPO growth would signal that customers continue to sign larger, longer-term contracts, even as the company has grown into one of the largest players in cybersecurity.

Investors are increasingly looking for evidence that AI-driven security spending is translating into real customer commitments. If Palo Alto can continue to grow its backlog faster than revenue, it would reinforce the bull case that demand remains strong heading into fiscal 2027.

Palo Alto Networks' Technical Setup Ahead of Tonight's Q3 Earnings

Technical Setup Into the Close

Palo Alto Networks (NASDAQ:PANW) trades at $294.34, down 2.04% from Monday’s $300.48 close, sitting well above its 50-day SMA of $194.03 and 200-day SMA of $190.03. The gap underscores how stretched this rally has become after a 65.94% one-month gain.

The 14-day RSI sits at 83.71, deep in overbought territory, and has been elevated above 80 for most of the past two weeks. Near-term resistance is the round $300 level, with initial support sitting at last week’s $260 breakout zone, with the $256.75 May 26 base below that.

The average earnings-day move across the last five beats was -3.35%. This shows that even strong Q3 results could lead to a share price decline after hours.

Bull vs Bear Case for Palo Alto Networks Ahead of Q3 Earnings Tonight

With Palo Alto Networks (NASDAQ:PANW) shares at $293.81 and up 65.94% over the past month, this is what the Bull vs Bear case looks like ahead of tonight’s Q3 earnings:

Bull Case

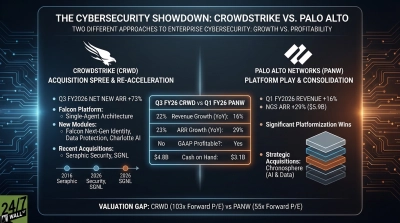

- Q3 guidance implies acceleration to 28-29% revenue growth with CyberArk (NASDAQ:CYBR) contribution.

- NGS ARR guided to $7.94-$7.96B (56% YoY); Polymarket pegs an ARR beat above $7.5B at 99.5%.

- Wedbush lifted its target to a Street-high $325, citing platformization momentum.

- CEO Nikesh Arora bought 67,985 shares in late March near $147.

Bear Case

- Valuation is stretched at a forward P/E of 83 with analysts’ consensus price target at just $230.82.

- EVP Lee Klarich offloaded shares May 22 at $250-$261.

- Active exploitation of CVE-2026-0257 in GlobalProtect adds a fresh headwind.

- Polymarket sees only 2.7% odds of ARR clearing $8.5B, signaling a modest beat is already priced in.

Guidance Will Determine PANW's Move After Q3 Earnings Tonight

Wall Street consensus is calling for $0.80 EPS against management’s Q3 guide of $0.78–$0.80. Investors want to see FY2026 revenue raised above $11.31B, NGS ARR lifted past $8.62B, and FCF margin held at 37%.

CEO Nikesh Arora‘s team typically guides conservatively, then raises. Polymarket pegs NGS ARR above $8.0B at a 92% probability, but only 2.7% at $8.5B.

Bullish: FY26 NGS ARR raised above $8.62B, EPS path to $3.70+, CyberArk integration ahead of schedule.

Bearish: Light Q4 implied guidance, NGS ARR growth slipping below 50%, or margin compression from acquisition dilution. At 156x earnings, anything short of a raise risks the rally.

4 Wildcards Not Fully Factored Into PANW's Consensus Estimates

Four Wildcards Not in Consensus

1. CyberArk integration cost shock. The $2.3 billion cash outlay in Q3 plus 112 million shares issued could pressure margins beyond the 28.5–29.0% guide.

2. Next-Gen Security ARR setting a near-impossible bar. Polymarket prices Above $8.5B at just 2.7%, yet the Q3 guide already implies 56% YoY growth.

3. Chronosphere accretion surprise. Already $200 million in ARR, well above plan, with a nine-figure expansion deal from a leading AI model provider.

4. Valuation. With shares at $293.81 and analysts’ average price target at $230.82, any soft commentary on long sales cycles or share-based comp could trigger another sell-the-news drop.

PANW Q3 Pre-Earnings: Market's Looking for Strong Forward Guidance

Palo Alto Networks has developed a habit of beating expectations, topping estimates in each of the past five quarters. The challenge is that investors increasingly expect it. Despite that streak, the stock’s average earnings-day reaction over that period has been a 3.35% decline.

With shares already up more than 15% over the past week, the bar heading into this report looks particularly high. Investors will be watching for signs that the company’s CyberArk acquisition can accelerate growth and support a higher FY2026 outlook.

Management likely needs to raise expectations again to keep the rally going.

I’m watching Palo Alto Networks (NASDAQ: PANW) ahead of its fiscal third-quarter results due today, June 2, after the market closes at around 4:05 PM ET. With shares up 63.13% year-to-date, expectations are high heading into earnings.

A Rally Built on Platformization

Last quarter, Palo Alto delivered $2.59 billion in revenue, up 14.91% year-over-year, with non-GAAP EPS of $1.03 beating the $0.9389 consensus by 9.7%. Next-Gen Security ARR hit $6.30 billion, up 33%, while non-GAAP operating margin held at 30.3% for a third straight quarter above 30%.

Last quarter, CEO Nikesh Arora announced the pending CyberArk identity-security deal and the Chronosphere observability acquisition, both of which underpin guidance for Q3 revenue growth accelerating to 28 to 29%. Shares have run 65.94% in the past month alone.

Consensus Estimates

| Metric | Q3 FY26 Guide | YoY Growth |

|---|---|---|

| Revenue | $2.941B–$2.945B | 28–29% |

| Non-GAAP EPS | $0.78–$0.80 | Roughly flat vs. $0.80 |

| NGS ARR | $7.94B–$7.96B | 56% |

| RPO | $17.85B–$17.95B | 32–33% |

| FY26 Revenue | $11.28B–$11.31B | 22–23% |

| FY26 Non-GAAP EPS | $3.65–$3.70 | N/A |

The ARR Step-Up Will Set the Tone

The headline number I’m watching with Palo Alto tonight is Next-Gen Security ARR. Management guided to $7.94-$7.96 billion, a massive step up from Q2’s $6.30 billion. That jump reflects the expected CyberArk close, so investors will be watching for confirmation of timing and contribution math. Polymarket traders price NGS ARR above $7.5B at 99.5%, but above $8.5B at just 2.7%, framing the zone of anticipated outcomes.

Investors will also watch margin durability. Holding non-GAAP operating margin near the FY26 guide of 28.5 to 29.0% while absorbing two acquisitions is the real test. Integration costs from Chronosphere, with $160M+ ARR growing triple digits, could pressure near-term profitability.

The third focus is platformization commentary. Arora described customers as “keen to both modernize and normalize their cybersecurity stack,” citing AI as the accelerant. Investors will be looking for a sharper count of platform deals and AI-security attach rates. Prediction markets imply a 96.4% beat probability, so even meeting expectations may underwhelm a stock trading at a forward P/E near 83.

Thomas Richmond is a financial writer and content strategist with 5+ years of experience covering stocks and financial markets. He has published over 250 articles focused on individual stock analysis, helping investors better understand business fundamentals, stock valuations, and long-term opportunities.

Thomas previously served as a Content Lead at TIKR, a stock research platform, where he helped scale the company’s blog to hundreds of articles per month and contributed to a weekly newsletter reaching more than 100,000 investors.

He specializes in breaking down complex companies into clear, actionable insights for everyday investors, with a focus on fundamentals-driven research.

His work has also been featured on platforms including Seeking Alpha and Sure Dividend.

Outside of work, Thomas enjoys weight lifting and soccer.

© 24/7 Wall St.