Spotify (NYSE:SPOT | SPOT Price Prediction) just delivered a quarter that should have settled the bear case. Premium subscribers hit 293 million, free cash flow surged 54.6% to $824 million, and operating income climbed 40.47%. Yet shares trade at $507.76, down 12.56% year to date.

The streaming leader is firing on every operational cylinder, but the stock keeps slipping. Can Spotify reach $900 in 2027?

Why Spotify Is Down This Year

Management guided Q1 operating income to €660 million against a baked-in 670 bps FX headwind, and Wall Street rejected it. The stock has dropped 23.66% over the past year and slid another 2.33% in the past week, despite a 15.01% bounce off the May low. With a beta of 1.554, this stock amplifies sentiment shifts.

Add the €410 million MLC lawsuit overhang, the €975 million TME fair-value decline, and a -5% drop in Ad-Supported revenue, and the market wants to punish non-operational noise. Premium ARPU growth of just 1% in euros hasn’t helped.

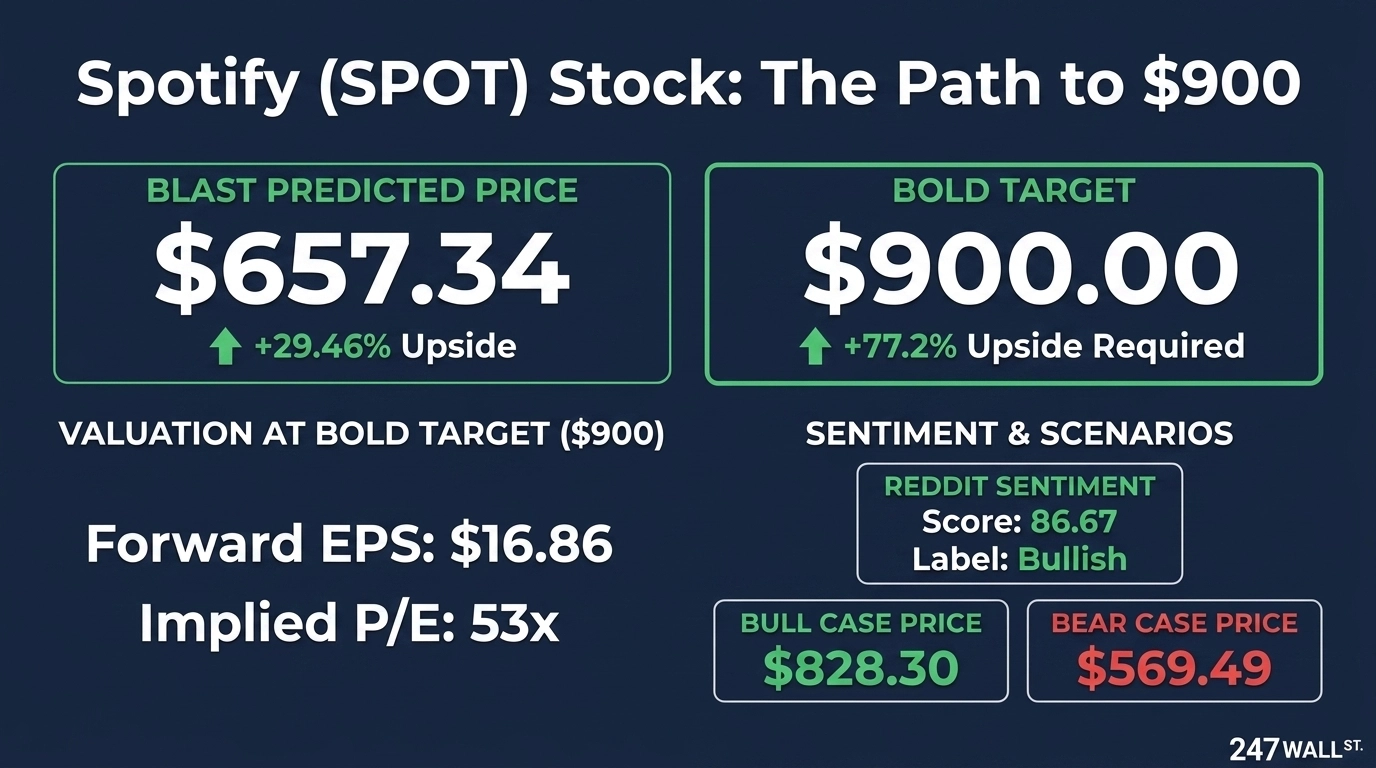

Wall Street Sees 20% Upside. Our Model Says 29%.

The Street has a consensus target of $609.02, supported by 10 Strong Buy, 24 Buy, 7 Hold, and zero Sell ratings. That is 83% bullish. Our base case is $657.34, implying 29.46% upside with 90% confidence. Our bull case stretches to $828.30, the bear case to $569.49.

Analysts are anchoring to FX-distorted euro guidance and ignoring that quarterly earnings grew 222.4% YoY. When a business compounds operating income and FCF at 40%-plus and the multiple keeps compressing, consensus is too conservative. The Street is fighting the last quarter rather than the next four.

The Path to $900 Per Share

Reaching $900 from today’s price of $507.76 would require a gain of 77.2%. With forward EPS of $16.86, a price of $900 implies a forward P/E of 53. Our base case of $657.34 already implies 36x, meaning the bold target requires roughly 17x of additional multiple expansion.

The building blocks exist. The 247Factor lands at 1.157, lifted by strong analyst consensus and strong earnings acceleration. AI features (Taste Profile, Prompted Playlist, SongDNA) give Spotify a credible ARPU story.

The $2 billion buyback (with $1.024 billion remaining) tightens the float. Q4 2025 showed operating leverage with record gross margin of 33.1% and EPS of $4.43 against a $2.85 estimate. If FY 2027 EPS approaches $22, a 40x multiple gets you to $880, and any sentiment shift carries it further. The primary risk is a punitive MLC ruling that forces a structural royalty reset.

Where Spotify Trades Today vs Its Earnings Power

At $507.76 on forward EPS of $16.86, Spotify trades at roughly 30x forward. Against earnings growth of 222.4% YoY and FCF growth of 54.6%, it is the most reasonable multiple this stock has carried in years. Shares sit 22% below the 52-week high of $785 and well off the $405 low. Over the last ten years, SPOT has delivered 240.76%. The earnings power is real.

Is $900 Realistic?

Reaching $900 by 2027 requires a 77.2% gain. That is a stretch well above our base case.

Three things need to go right: FY 2027 EPS needs to push toward $22 on Premium ARPU re-acceleration, the MLC liability needs to settle below the headline number, and Ad-Supported revenue needs to inflect positive as the Partner Program scales. A deeper FX hit or punitive royalty ruling derails it. We’ve outlined the blueprint for how Spotify could reach $900 in 2027.

Contact [email protected] for any questions or corrections.