Webull (NASDAQ:BULL | BULL Price Prediction) is the digital brokerage Wall Street struggles to value. The platform posted 26 million registered users, $24.6 billion in customer assets, and Q4 revenue growth of 53.4% year over year.

Yet shares trade at $7, down 41.23% over the past year. CEO Anthony Denier launched proprietary AI engine Vega, expanded into Hong Kong and Korea, and approved a buyback. Can BULL triple to $25 by 2027?

What’s Holding Webull Back

The stock is down 9.91% year to date and off 0.28% over the past week, even after a 4.17% bounce in the last month. Short interest jumped 15.3% month over month to roughly 19.9 million shares, and one April note pointed out that BULL stock pulled back 7.39% amid regulatory scrutiny concerns.

Investors worry about payment for order flow exposure, China-connection scrutiny, and Q4 net income that fell 72% year over year as marketing spend more than doubled. Beta of 0.604 understates volatility: shares have ranged from $4.50 to $18.32 in 52 weeks.

Wall Street Sees 67% Upside

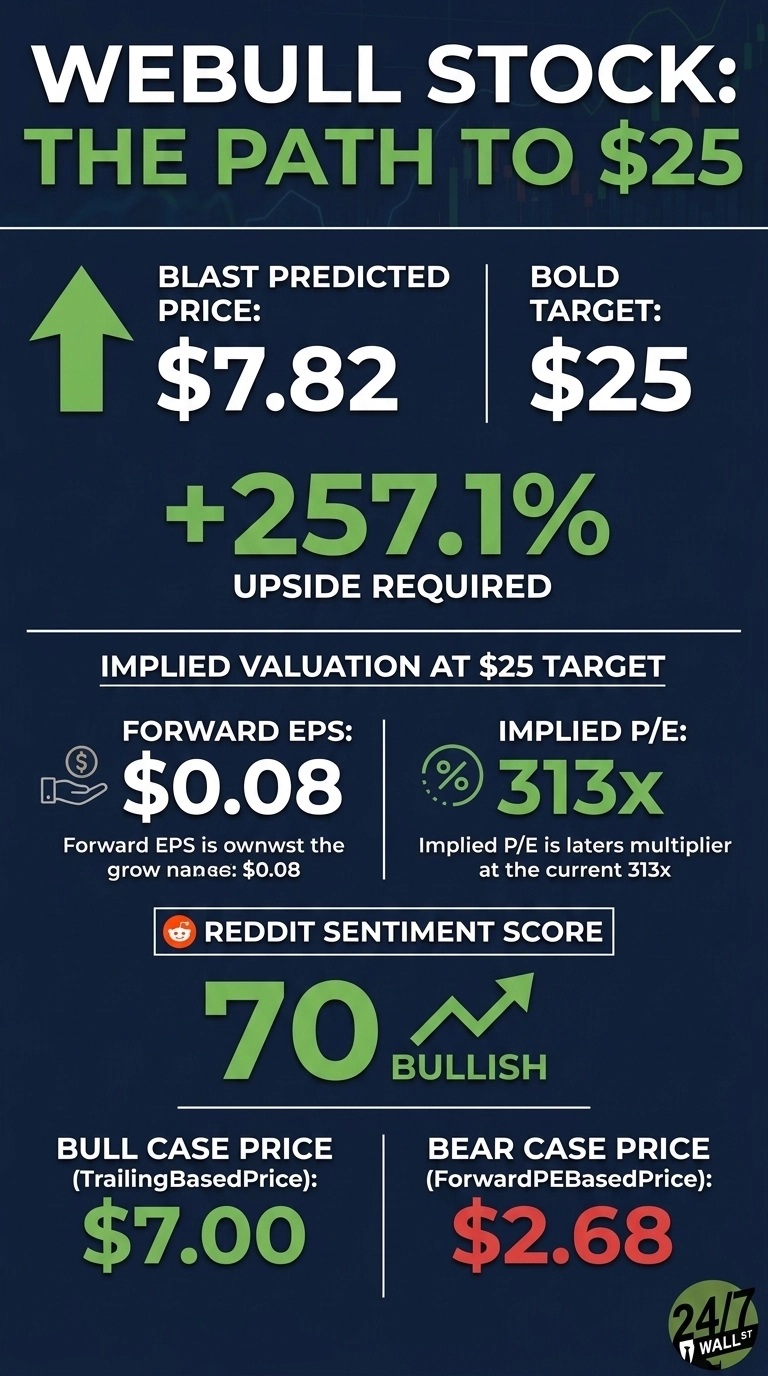

The analyst target sits at $11.67, with 3 Buy ratings, 0 Holds, and 0 Sells. That is 100% bullish coverage, yet implied upside is just 66.71%. Our 24/7 Wall St. model lands at $7.82, an 11.66% upside with 90% confidence.

The bull scenario reaches $20.15 by May 2027, while the bear case sits at $6.69. With every analyst rating BULL a Buy and earnings inflecting hard, consensus anchors too closely to today’s depressed multiple.

The Path to $25 Per Share

Reaching $25 from $7 requires a gain of 257.1%. With forward EPS of $0.08, a price of $25 implies a forward P/E of 313x. Our base case of $7.82 already implies 88x, meaning the bold target requires 225x additional multiple expansion. That works only if EPS grows much faster than the Street models, compressing the forward P/E into something rational.

The setup exists. Operating income jumped 507% in fiscal 2025, the SEC removed the Pattern Day Trader minimum (a 0.727 sentiment score, highest in the dataset), and the board authorized a $100 million buyback.

Denier said Vega will “help investors navigate the growing complexity of market data by providing personalized, AI-generated research”, and roughly 1 in 8 users already consults it pre-trade. The 247Factor adjustment of 1.252 reflects strong technology sector momentum and that 100% bullish analyst consensus. The clear risk is regulatory: any PFOF or prediction-market crackdown caps the multiple immediately.

Where Webull Trades Today vs Its Earnings Power

The stock sits at 88x forward earnings on the model’s $0.08 forecast, or 32x using the Street’s estimate. Shares are 36% off the 52-week high of $18.32 and well above the $4.50 low.

As a recent IPO from April 2025, BULL has no 10-year history, but trailing revenue of $564 million against a $3.75 billion market cap gives a price-to-sales of 6.65. That is reasonable for a brokerage growing the top line 46% with operating income up triple digits.

Is $25 Realistic?

Reaching $25 from $7 means a 257.1% gain. For it to happen, Vega adoption must drive measurable lifts in DARTs and Premium subscribers, international expansion in Hong Kong, Korea, and the Netherlands must scale revenue meaningfully, and the buyback must shrink the float into a re-rating.

Regulatory action on PFOF or prediction markets would derail it. We’ve outlined the blueprint for how Webull could reach $25 in 2027.

Contact [email protected] for any questions or corrections.