Palantir (NASDAQ:PLTR | PLTR Price Prediction) is the rare AI software story where the fundamentals are arguably running ahead of the stock. Palantir just guided 2026 revenue growth to 71% after Q1 came in at 85% YoY, yet shares are down 20.28% year to date.

The stock closed at $141.70 on June 4. So can PLTR reclaim and clear $200 by mid-2027? That is the question I want to answer with actual math, not vibes.

What’s Holding Palantir Back Right Now

The disconnect is brutal. PLTR is up only 4.26% over the past month and down 1.14% on the week despite a guidance raise the company called its largest ever. Two things are weighing on shares. First, valuation gravity: a trailing P/E of 173 invites profit-taking after any wobble.

Second, sentiment. Michael Burry’s widely circulated “sand castle supported only by AI applications narrative” critique has dominated discussion since June 3, and insiders have not helped. CEO Alex Karp, director Stephen Cohen, and CTO Shyam Sankar all executed large coordinated dispositions on May 20 in the $132 to $137 range. With a beta of 1.521, this stock amplifies every headline.

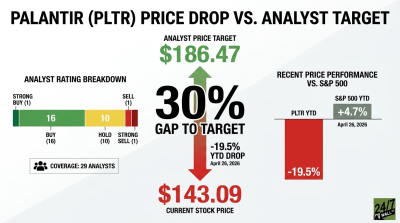

Wall Street Sees 30% Upside. Our Model Says 15%

The Street is more bullish than our base case. The consensus price target sits at $183.73, supported by 1 Strong Buy, 18 Buy, 10 Hold, 1 Sell, and 1 Strong Sell ratings. That is 61% bullish. Our model is more cautious.

Our base case lands at $163.08, implying 15.09% upside, with conviction at a 90% confidence level. Where we diverge from the Street: analyst targets do not yet fully incorporate the post-Q1 guide. With QoQ Rule of 40 expanding to 145, I think consensus is anchored to stale numbers. The bull case may be more credible than analysts currently model.

The Path to $200 Per Share

Here is the math. Reaching $200 from $141.70 requires a gain of 41.1%. With forward EPS of $1.11, $200 implies a forward P/E of 180x. Our base case at $163.08 already carries an implied multiple of 189x, meaning $200 actually requires no additional multiple expansion beyond the base case if you trust the model’s forward EPS path.

That sounds aggressive, but Palantir’s earnings are compounding into the multiple. Q1 2026 adjusted EPS hit $0.33, and management guided full-year adjusted operating income to $4.44 to $4.452 billion.

Karp’s framing matters: “Our biggest problem currently in the U.S. is that we just cannot meet demand.” Named AIP customers including AIG, GE Aerospace, and Freedom Mortgage support that. The primary risk is a defense continuing resolution that slows government bookings into 2027.

Where Palantir Trades Today vs Its Earnings Power

At $141.70, PLTR trades at a current forward P/E of 128x against $1.11 in forward EPS. Expensive by any normal yardstick, but the company is compounding revenue at 71% guided for 2026. Shares sit 11% off the 52-week high of $207.52, well above the $121.92 low. The five-year return is 489.68%, and the ten-year mark stands at 1,391.58%. Earnings power is finally catching the price.

The Bottom Line on $200

Reaching $200 by mid-2027 requires a 41.1% gain and a sustained forward P/E near 180x. Realistic, in my view, but not guaranteed.

Three things need to happen: U.S. commercial revenue must clear the $3.224 billion 2026 bar, Rule of 40 needs to stay above 100, and government bookings cannot stall on a CR. A broader AI sentiment unwind would derail it fastest. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Palantir could reach $200 in 2027.

Contact [email protected] for any questions or corrections.