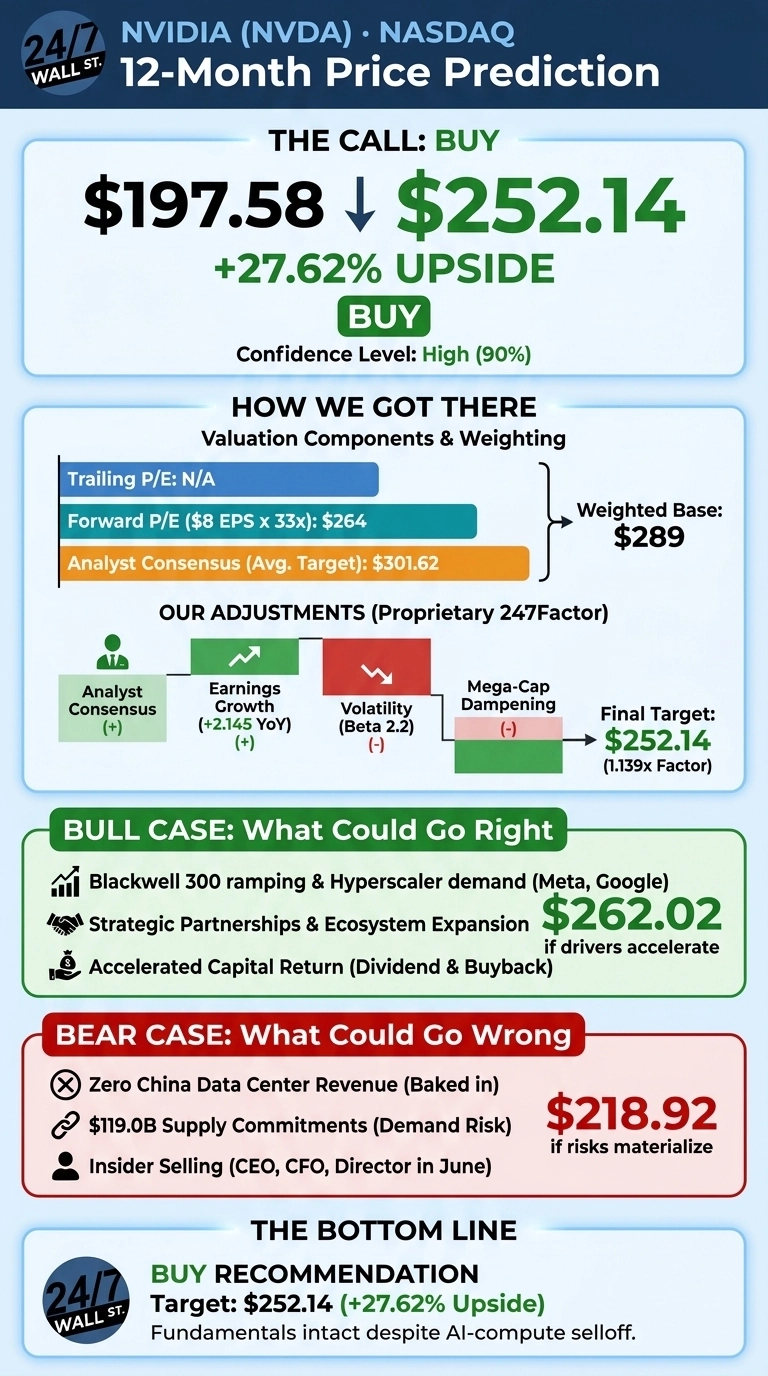

Our NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) 24/7 Wall St. price target for the next 12 months is $252.14, implying 27.62% upside from the current price of $197.58. NVIDIA has slipped hard in the recent AI-compute selloff, but the fundamentals under the hood have not cracked. Our recommendation is buy, with a high confidence level of 90%.

| Metric | Value |

|---|---|

| Current Price | $197.58 |

| 24/7 Wall St. Price Target | $252.14 |

| Upside | 27.62% |

| Recommendation | BUY |

| Confidence Level | 90% |

How NVIDIA Got Caught in a Sector-Wide Reset

NVIDIA is down 11.84% over the past month, retreating from a mid-May peak near $225.32. Even after the pullback, shares are still up 6.07% year-to-date and 29.05% over the past year, with the stock currently sitting between a 52-week low of $157.13 and a high of $236.26. The July 1 semiconductor session was ugly, with KLA down 12.3%, Micron down 8%, and AMD down 5.73% as institutions rotated out of chips.

Q1 FY2027 revenue hit $81.615 billion, up 85.23% year-over-year, with non-GAAP EPS of $1.87 beating consensus by 5.42%, the fourth straight beat. Data Center revenue reached $75.246 billion (up 92% YoY), and management guided Q2 to $91 billion, again excluding any China Data Center compute.

The Case for $262 and Higher

Our bull case points to $262.02 over the next year. The driver is Blackwell 300 ramping into insatiable hyperscaler demand, with 54 research firms carrying a Buy consensus and an average target of $303.84.

Strategic wins keep piling up: the Vera Rubin A5X instances on Google Cloud, a Marvell NVLink Fusion tie-up, the OpenAI 10GW deployment, and a multi-generational Meta agreement spanning millions of Blackwell and Rubin GPUs. Networking revenue tripled to $14.8 billion (up 199% YoY), showing that InfiniBand, NVLink, and Spectrum-X are becoming their own business.

Capital return has finally arrived, with the dividend lifted from $0.01 to $0.25 per share and a new $80 billion buyback approved.

The Risks Worth Watching

Our bear case lands at $218.92, roughly 10.8% above today. Zero China Data Center revenue is baked into guidance, and $119 billion in supply commitments creates real downside if hyperscaler capex ever cools.

Michael Burry is short NVDA, and insiders including CEO Jensen Huang and CFO Colette Kress sold shares on June 17 at $207.41, with Director Mark Stevens disposing of over 2 million shares in June.

The executive sales were coordinated on a single day at an identical price, consistent with pre-scheduled 10b5-1 plans rather than a panic exit. Free cash flow of $48.554 billion in a single quarter tells you demand is real.

I’d Buy It Here

Our 24/7 Wall St. Price Target is $252.14, our recommendation is buy, and our confidence is 90%. The tipping factor is the collision between an 85% revenue growth rate and a 12% one-month drawdown. I’d be a buyer here if hyperscaler capex commentary holds firm into the next earnings report. I’d stay on the sidelines if China export policy tightens further or Q2 guidance disappoints.

Looking further out, here is where our model projects NVIDIA could trade, assuming Blackwell and Rubin adoption continue on their current arc.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $252 |

| 2027 | $291 |

| 2028 | $328 |

| 2029 | $365 |

| 2030 | $401 |

These projections assume NVIDIA continues executing on the Vera Rubin roadmap and agentic AI adoption scales as forecast. Meaningful upside or downside could come from China policy shifts, custom ASIC competition from Broadcom and AMD, or a step-change in hyperscaler capex.

Contact [email protected] for any questions or corrections.