ON Semiconductor (NASDAQ:ON | ON Price Prediction) has staged one of the most aggressive recoveries in the chip sector this year, and our proprietary model still sees room to run.

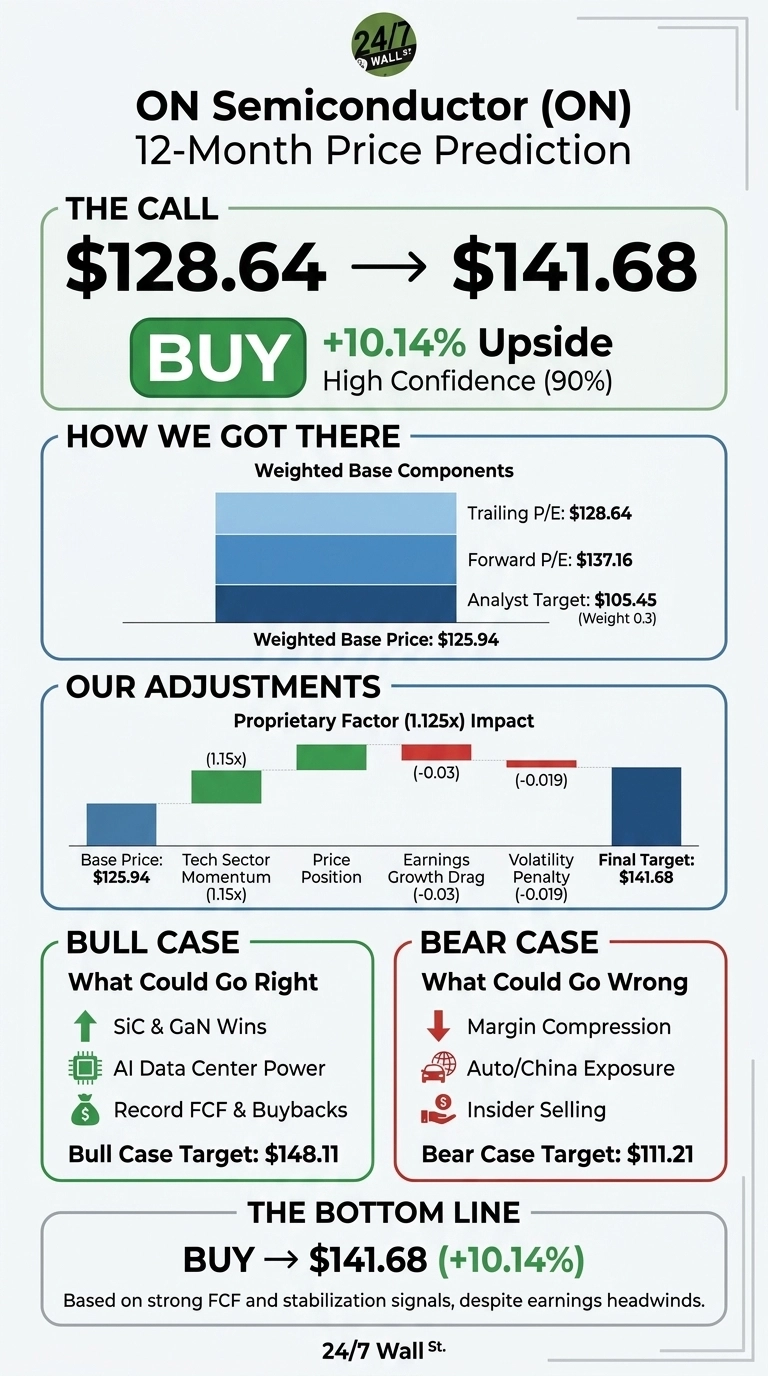

After a vicious 2025 cyclical downturn, shares have rallied 137.56% year to date and now trade just shy of the 52-week high. Our 24/7 Wall St. price target for onsemi is $141.68, implying additional upside even after the run.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $128.64 |

| 24/7 Wall St. Price Target | $141.68 |

| Upside | 10.14% |

| Recommendation | BUY |

| Confidence Level | 90% |

The 24/7 Wall St. price target points to $141.68 over the next 12 months, a constructive view that runs against the Street’s $105.45 consensus. Confidence is high, but with a beta near 1.94, position sizing matters.

A Vertical Rally Out of a Cyclical Trough

ON is up 202.4% over the past year and 24.86% in the past month alone, with shares climbing from $113.11 on May 15 to current levels.

The rally followed Q4 2025 results that beat on the bottom line: revenue of $1.53 billion against $1.54 billion expected, with non-GAAP EPS of $0.64 versus the $0.62 estimate.

CEO Hassane El-Khoury flagged “increasing signs of stabilization in our key markets”, and FY2025 free cash flow hit a record $1.42 billion, fully returned via $1.377 billion in buybacks alongside a fresh $6 billion three-year repurchase authorization.

The Case for $148 and Beyond

The bull thesis rests on operating leverage as the cycle turns. Q4 free cash flow grew 11.6% even on an 11.2% revenue decline, evidence that El-Khoury’s restructuring is sticking.

Growth catalysts are stacking: vertical GaN power semiconductors, the MoU with Innoscience for 200mm GaN-on-silicon, a GlobalFoundries collaboration on 650V GaN, and EliteSiC M3e wins including the Xiaomi EV SUV.

AI data center power is the wild card, and r/stocks chatter framing onsemi as “My most confident ai chip play” hints at retail momentum building. Our bull case puts shares at $148.11.

What Could Go Wrong

The bear case is real. Barclays initiated coverage at equal-weight with a $75 price target, citing automotive and China exposure. FY GAAP gross margin compressed to 33.1% from 45.4%, and the company absorbed $666.9 million in restructuring and impairment charges last year.

Insider activity adds caution: CFO Thad Trent sold 90,000 shares across April at $80 to $100. Bulls would counter that those charges reflect heavy investment in SiC and GaN capacity that should drive future operating leverage, and that the new $6 billion buyback partially offsets the dilution risk. Our bear case lands at $111.21.

ON Semiconductor Price Prediction 2026-2030

Our 24/7 Wall St. price target of $141.68 carries a buy recommendation with 90% confidence. The factor tipping the scale is the combination of record FCF generation through a downturn and a credible 2026 stabilization signal from management.

The bull case strengthens if the Q1 2026 earnings report confirms revenue holding within the $1.435 billion to $1.535 billion guide. The thesis weakens if non-GAAP gross margin slips below the 37.5% guidance floor, since that would signal pricing pressure is outrunning the cost reset.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $141.68 |

| 2027 | $152.00 |

| 2028 | $163.00 |

| 2029 | $173.00 |

| 2030 | $183.45 |

These projections assume onsemi continues executing on its SiC, GaN, and intelligent sensing roadmap while the auto and industrial cycles normalize. Significant upside or downside could result from AI data center power demand inflection or a deeper China automotive correction.

Contact [email protected] for any questions or corrections.