Palantir (NASDAQ:PLTR | PLTR Price Prediction) just dropped a quarter that should have ended the debate. The company posted 70% revenue growth in Q4 2025, with US commercial revenue exploding 137% year-over-year.

CEO Alex Karp called the company “an n of 1”, and the Rule of 40 score hit 127%. Yet shares sit at $160.65, down 9.62% year to date. So can this stock hit $250 by 2028? Here is what would have to go right.

What’s Holding Palantir Back Right Now

The disconnect between fundamentals and price is simple to name. Valuation. PLTR trades at a trailing P/E of 176 and a price-to-sales ratio of 71.83. Those numbers leave no margin for error. After ripping from $24.45 to $207.52 over the past five years (a 557.06% gain), the stock peaked in December at $183.25 and slid to a February low of $133.02.

A beta of 1.521 means every market wobble hits PLTR harder. The recent bounce is real (up 17.37% over the past week and 11.51% over the past month), but the YTD hole reflects multiple compression.

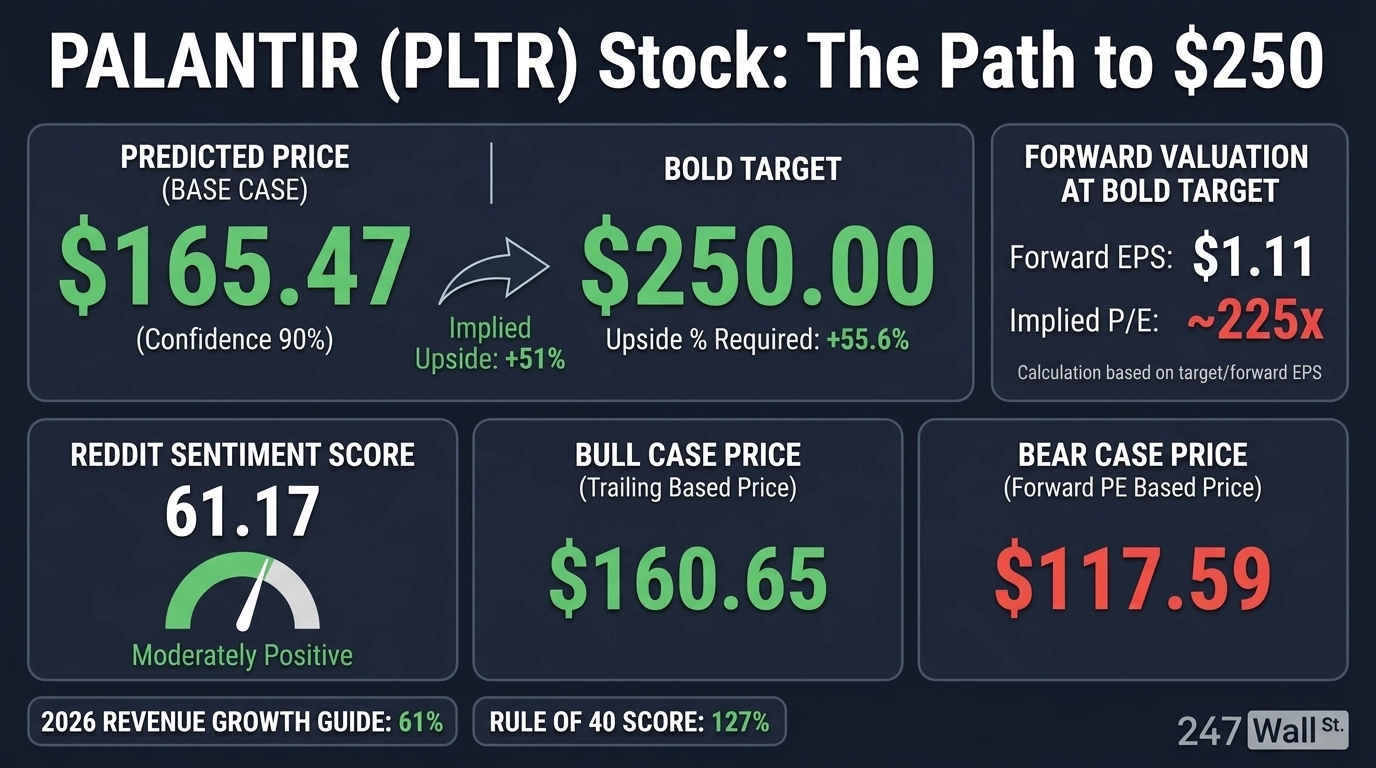

Wall Street Sees Upside. I Think They’re Underestimating

The Street’s consensus target sits at $183.73, with 1 Strong Buy, 18 Buy, 10 Hold, 1 Sell, and 1 Strong Sell ratings. Bullish sentiment runs at 61%. Our model’s base case lands at $165.47 with a high-confidence 90% score, framed by a bull case of $203.96 and a bear case of $147.94.

Here is my pushback. Analysts are anchoring on next-twelve-month earnings while underweighting the second-derivative story: a company guiding to 61% revenue growth in 2026 with adjusted free cash flow of $3.925 to $4.125 billion. That cash machine is the part the consensus underweights.

The Path to $250 Per Share

Reaching $250 from today’s price of $160.65 would require a gain of 55.6%. With forward EPS of $1.11, a price of $250 implies a forward P/E of 225x. Our base case of $165.47 already implies 214x, meaning the bold target requires roughly 11x of additional multiple expansion.

That sounds extreme until you look at the earnings ramp. If FY 2026 revenue lands at the guided $7.198 billion and adjusted operating income hits $4.142 billion, forward EPS estimates get rerated higher through 2027.

That is the compression story: the multiple stays elevated while earnings catch up. Karp’s framing of “commodity cognition” and AIP-driven enterprise adoption is the engine. The risk: any AI spending slowdown or contract termination shock could break the narrative fast.

Where Palantir Trades Today vs Its Earnings Power

At $160.65 against forward EPS of $1.11, PLTR carries a forward P/E of 145x. Expensive on any traditional screen. But the 52-week range of $118.93 to $207.52 shows the market has already paid up for this growth.

Over the last ten years, shares have returned 1,591.05%. The multiple is a function of scarcity. Palantir is the only public pure-play scaling AI operational software at this margin profile.

$250 Is a Stretch, But Here’s Why It’s Possible

Hitting $250 by 2028 requires that 55.6% gain. Honest take: it is a stretch, but it is achievable.

Three things need to go right. US commercial growth has to stay above 100% through 2026. Adjusted FCF needs to land at the high end of guidance. And the AI software premium has to hold across the sector.

The derailer is a single quarter where US government revenue slows and the multiple finally compresses. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how Palantir could reach $250 in 2028.

Contact [email protected] for any questions or corrections.