The AI trade in 2026 has splintered into four very different tapes. NVIDIA (NASDAQ:NVDA | NVDA Price Prediction) is grinding higher. AMD (NASDAQ:AMD) is on a tear. Palantir (NASDAQ:PLTR) has given back a chunk of last year’s move. And Tesla (NASDAQ:TSLA) is stuck near its 200-day. I want to lay out what each of these four needs to do to hit my stretch 2029 targets, and where I think the math actually works.

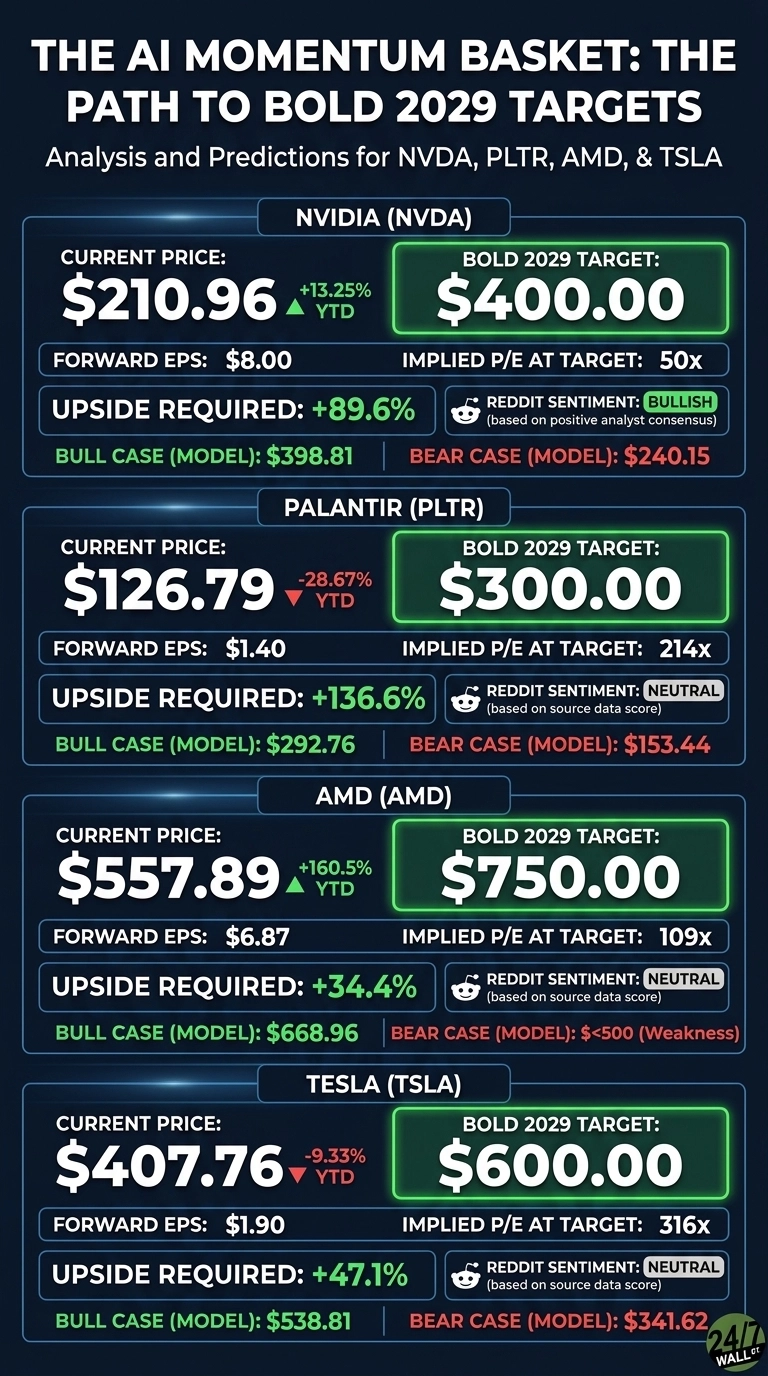

NVIDIA: The Path to $400 by 2029

NVIDIA is up 13.25% YTD and 955.75% over five years. Q1 FY27 revenue hit $81.61 billion, +85.2% YoY, with Data Center at $75.25 billion. Jensen Huang called the AI factory buildout “the largest infrastructure expansion in human history.” My bold 2029 target is $400, above the model’s bull case of $398.81 for July 2029.

Reaching $400 from $210.96 requires a gain of 89.6%. Forward EPS of $8 puts $400 at a forward P/E of 50x, above the 36x implied by my base case of $260.92. Consensus sits at $301.62 with 58 buys and 1 sell. Multiple expansion above 40x is credible if data-center dominance holds.

Palantir: The Case for $300

Palantir is down 28.67% YTD, but Q1 2026 revenue was $1.63 billion, +84.7% YoY, with U.S. commercial up 133%. Alex Karp said “Palantir’s Rule of 40 score has soared to 145%. We have shattered the metric.” My 2029 bold target is $300, above the model’s bull case of $292.76.

$300 from $126.79 is a gain of 136.6%. Forward EPS of $1.40 implies a forward P/E of 214x at $300, versus the 133x already priced into my base case of $159.66. This is the hardest of the four to justify on multiples. It only works if U.S. commercial ARR keeps compounding above 100% and FY29 EPS runs materially higher.

AMD: The Path to $750

AMD has ripped 160.5% YTD. Q1 2026 Data Center revenue hit $5.78 billion, +57% YoY. Lisa Su noted MI450 customer forecasts are “exceeding our initial expectations,” and the 6 GW Meta Instinct deployment is now the anchor. My 2029 bold target is $750.

That is a gain of 34.4% from $557.89. Forward EPS of $6.87 puts $750 at a forward P/E of 109x. Stretched, but EPS is on a steep ramp with 42 buy ratings and zero sells. If you want the deeper picks-and-shovels lens on this cycle, our Next Nvidia Playbook maps how successor names typically re-rate.

Tesla: The Path to $600

Tesla is down 9.33% YTD. Robotaxi launched in Dallas and Houston. FSD subs hit 1.28 million, +51% YoY. My 2029 bold target is $600, above the model bull case of $538.81.

That is a gain of 47.1% from $407.76. Forward EPS of $1.90 implies a forward P/E of 316x at $600. That only works if Optimus and Robotaxi actually contribute meaningful EPS by 2029, and auto gross margin holds above 20%. The consensus target of $424.56 tells you Wall Street is not there yet.

The Bottom Line

Four names, four paths. NVDA to $400 is a gain of 89.6% and the highest-conviction of the bunch. AMD to $750 needs 34.4% and looks achievable if MI450 execution lands. TSLA to $600 needs 47.1% and real autonomy monetization. PLTR to $300 needs 136.6% and remains a stretch.

What derails all four together is an AI capex reset. Returns at this level shouldn’t be expected every year, but we’ve outlined the blueprint for how the AI Momentum Basket could reach $400, $300, $750, and $600 in 2029.

Contact [email protected] for any questions or corrections.