A dollar in First Trust NASDAQ Cybersecurity ETF (NASDAQ:CIBR) on the last trading day of 2025 was worth about $1.22 by the close on June 5, 2026, while the same dollar in the S&P 500 was worth about $1.08. That is the headline making the rounds, and the shorthand version of it (cybersecurity beat the broad market by three to one) is close enough to true that it is worth taking apart carefully, because the mechanism behind the gap is also the thing that tells you whether the next six months look anything like the last six.

The Arithmetic, Without the Spin

CIBR opened the year at $71 and closed June 5, 2026 at $87, a 22% year-to-date gain. The S&P 500, via SPY, went from $682 to $738, an 8% gain. The actual ratio is closer to 2.6 to 1 rather than a clean 3 to 1, and the bulk of CIBR’s move happened in a single month. The fund was up 24% in the thirty days ending June 5, which means that without May, the year-to-date story would read like an ordinary tech-adjacent fund nudging ahead of the index.

Total return matters less than usual here. CIBR is not an income product, distributions are small, and the price-only number captures essentially the whole picture. Over five years the fund is up about 101%, against about 75% for SPY, so the long-run edge is real but modest. The 2026 outperformance is the kind of jolt that pulls a decade’s worth of structural alpha into half a year, and that is the part that needs explaining.

What Actually Did the Work

CIBR is concentrated by design. The March 31, 2026 NPORT filing shows $9.49 billion in net assets across 44 positions, with Palo Alto Networks at 8.46%, CrowdStrike at 8.25%, Cisco at 7.67%, Broadcom at 7.61%, and Fortinet at 7.40%. The top five alone carry more than a third of the fund. When a handful of names rerate together, this ETF moves like a single stock with a slightly muted volatility profile.

That is what happened among the fund’s largest cybersecurity holdings — Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction), CrowdStrike (NASDAQ:CRWD), and Fortinet (NASDAQ:FTNT) — each of which posted accelerating numbers tied to the same AI-security narrative.

Fortinet is up 82% year-to-date after a Q1 2026 print on May 6 that put non-GAAP EPS at $0.82 against a $0.62 consensus, a 33% beat, with revenue of $1.85 billion (+20.1% YoY), product revenue up 41%, and billings up 31%. CEO Ken Xie attributed the demand to "an increasingly complex threat environment that is being intensified by AI", and the firm raised full-year 2026 revenue guidance to $7.71 billion to $7.87 billion.

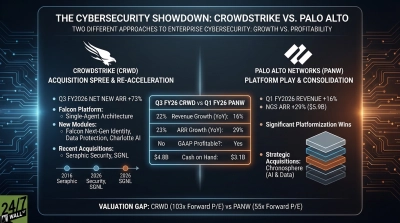

Palo Alto Networks is up 48% year-to-date, and the June 2 report supplied the catalyst. Q3 FY26 revenue hit $3.00 billion, up 31.1% year-over-year, with Next-Generation Security ARR of $8.10 billion growing 60%. The CyberArk and Chronosphere deals contributed $388 million in the quarter, which is meaningful but not the whole story. CEO Nikesh Arora’s framing was that "customers turn to us to secure their AI deployments at scale", and the company is now targeting a 40% adjusted free cash flow margin by FY28.

CrowdStrike is up 43% year-to-date, despite a sharp 8% pullback the week of the print. Q1 FY27 revenue grew 25.6% to $1.39 billion, net new ARR hit a Q1 record of $255.8 million, and total ARR reached $5.51 billion. George Kurtz called it the "Mythos moment" and said "CrowdStrike is AI security infrastructure, critical to successful AI adoption." The company also announced a four-for-one stock split, with split-adjusted trading beginning July 2, 2026.

Even Okta (NASDAQ:OKTA), which sits at 2.70% of the fund and grows more slowly than the platform leaders, is up 37% year-to-date. CEO Todd McKinnon’s pitch is that "AI agents are rapidly becoming a new workforce inside every organization, creating a wave of identities that must be secured and governed", which is the same thesis Arora, Xie, and Kurtz are selling under different brand names.

The mechanism is therefore one trade. Every meaningful CIBR overweight is pricing in an AI-driven step-change in enterprise security demand, and every CEO is saying so explicitly. Platform consolidation (Palo Alto’s NGS ARR accelerating from 29% to 33% to 60% growth across Q1 to Q3 FY26, CrowdStrike’s Falcon Flex ARR up more than 120% to $1.69 billion) is the structural piece. The AI-spend story is the cyclical piece sitting on top of it. They are working together right now, which is why the holdings did not just beat the market, they beat the ETF that holds them, because dead weight in older infrastructure names muted what would otherwise have been a 40%-plus year-to-date number.

The Setup Sitting Underneath

The 2026 capex backdrop is the part that is not in dispute. Vanguard’s baseline forecast pegs US capital expenditure growth at 7.0% versus a 2023-2024 pace of 3.8%, with AI as the explicit driver. Goldman Sachs frames AI capex as still in "the early innings" and notes that enterprise adoption is broadening into efforts to "clean, structure, and secure data so it can be used effectively by AI systems." That last clause is the cybersecurity sector’s entire 2026 thesis condensed into a single line in a buyside outlook.

Valuations reflect this. Palo Alto trades at roughly 196 times trailing earnings, an extreme multiple that only makes sense if NGS ARR keeps compounding well above 30%. Fortinet sits near 57 times, which is rich for a hardware-anchored business and assumes the product cycle keeps running. CrowdStrike’s prediction-market and analyst consensus puts a target of $707 against a $671 close, with 43 buys, 11 holds, and 1 sell, which implies single-digit upside on consensus from here even with the AI tailwind fully priced in.

What To Actually Watch

The honest read is that CIBR’s three-to-one moment is the result of a specific quarter in which every large holding posted accelerating numbers tied to the same narrative, against a market that is being asked to digest tariffs, a wobbling labor market, and the question of whether AI capex can keep compensating for weaker parts of the economy. The setup that produced the gain is intact. The valuation it produced is not the same starting point you had in January.

Three indicators will tell you whether the trade still works. Palo Alto’s NGS ARR growth rate is the cleanest read on platform consolidation momentum, and Q4 FY26 guidance calls for $8.90 to $8.95 billion, 59 to 60% growth. Anything that comes in with a five-handle on growth is the regime continuing. CrowdStrike’s net new ARR is the second, and management raised the FY27 net new ARR growth guide by 520 basis points to roughly 27.7% at the midpoint. A miss there breaks the "AI security infrastructure" framing in a way that no marketing language can repair. Fortinet’s billings growth is the third, because product revenue and billings are the leading indicators of the hardware refresh cycle that drove the 31% Q1 billings number. Watch for that to hold above 25%.

What you would not want to do is read the year-to-date gap as a free signal. The Reddit tape around CrowdStrike turned bearish to neutral immediately after the print despite the beat and the split announcement, with the dominant narrative shifting from "SaaSpocalypse canceled?" in mid-May to "CrowdStrike reports higher operating expenses as AI investments gain pace" by early June. That is the texture of a crowded trade where the next move depends less on whether the story is right and more on whether the next data point clears a much higher bar. The 2026 run was real, the mechanism is durable enough to take seriously, and the price you would pay to ride the next leg is now the open variable.

Contact [email protected] for any questions or corrections.