Shares of Palo Alto Networks (NASDAQ:PANW | PANW Price Prediction) are climbing again Thursday, up 5% in midday trading to $337 as the broader cybersecurity sector rebounds. The move caps a powerful rally that has Palo Alto Networks stock up 28% over the past month, making it the standout of the group.

The rally extends across the sector. CrowdStrike (NASDAQ:CRWD) shares have added 22% over the same stretch, while Fortinet (NASDAQ:FTNT) stock has climbed 18%, with all three trading higher again today alongside the broader tech tape.

That leaves investors with a familiar question. After a run like Palo Alto’s, does it make sense to book the gain and rotate into CrowdStrike or Fortinet, or is the whole cybersecurity cohort simply riding the same AI-driven wave?

The Why: Platformization and AI Security Demand

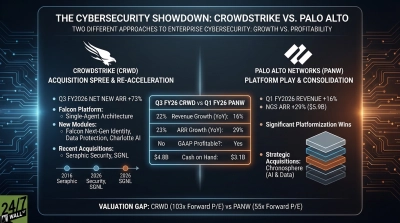

Palo Alto Networks reported a strong Q3 FY2026 on June 2, with revenue of $3 billion, up 31% year over year (YoY), and non-GAAP EPS of $0.85 against a $0.797 consensus. Next-Generation Security ARR jumped to $8.1 billion, up 60% YoY, aided by the CyberArk and Chronosphere acquisitions.

Moreover, Palo Alto Networks CEO Nikesh Arora framed the quarter as “a standout quarter for Palo Alto Networks, with accelerating organic bookings growth as customers turn to us to secure their AI deployments at scale.” That AI-security narrative is exactly what’s lifting CrowdStrike and Fortinet shares as well.

The Valuation Problem

Palo Alto Networks stock trades at a trailing P/E ratio of 291x, an extreme multiple that leaves little margin for error. CrowdStrike stock doesn’t even carry a trailing P/E ratio, because CrowdStrike’s TTM EPS sits at -$0.04, meaning the company is unprofitable on a trailing basis despite delivering 26% revenue growth in its most recent quarter.

Fortinet is the relatively cheapest of the trio at a trailing P/E ratio of 63x, and it’s the most profitable, with a TTM operating margin of 31% and net margin of 28%. Yet, even Fortinet stock isn’t necessarily cheap in absolute terms, and it has lagged Palo Alto and CrowdStrike this past month.

It appears, then, that rotating out of Palo Alto Networks into CrowdStrike or Fortinet doesn’t meaningfully reduce valuation risk. The entire cohort is richly valued after strong runs, and none of these names screens as a compelling bargain today.

The Sector Signal

The First Trust NASDAQ Cybersecurity ETF (NASDAQ:CIBR) confirms how tightly these cybersecurity sector stocks trade together. Palo Alto Networks, CrowdStrike, and Fortinet combined account for 24% of the fund’s net assets, with peers Zscaler (NASDAQ:ZS) and SentinelOne (NYSE:S) are also among the fund’s top holdings.

That concentration cuts both ways for CIBR investors. The ETF captures the sector’s AI-driven tailwind, though it doesn’t hedge against the group’s rich multiples. It’s an unleveraged, diversified expression of the theme, but a single-name blowup in the top three could drag the fund down.

What to Watch Now

Palo Alto Networks stock pulled back before today’s bounce, serving as a reminder that pricey assets can cut both ways. Investors sitting on outsized gains in PANW stock may consider keeping their position sizes modest rather than pressing their luck, since CrowdStrike and Fortinet carry their own valuation risks and correlated drawdowns are the norm across cybersecurity names.

For fresh capital, Fortinet offers the most defensible profile on profitability and valuation. CrowdStrike remains the purest growth play if trailing GAAP losses don’t bother you. Palo Alto’s category leadership and platformization momentum still look durable, just fully priced.

The next catalyst is Palo Alto’s Q4 FY2026 report, where management guided to revenue of $3.345 billion to $3.355 billion and EPS of $0.96 to $0.98. That print, plus the price action into next week, could set the tone for the next share-price moves in the group.

Contact [email protected] for any questions or corrections.