Broadcom (NASDAQ:AVGO | AVGO Price Prediction) and Qualcomm (NASDAQ:QCOM) just gave investors two different reads on the AI chip economy. Broadcom posted a record quarter driven by custom AI silicon for hyperscalers.

Qualcomm beat estimates while nursing a handset slump, leaning on automotive growth and a fresh data center engagement. Both stocks fell last week, making the $25,000 question worth asking now.

AI Silicon Carries Broadcom. Cars and Licensing Carry Qualcomm.

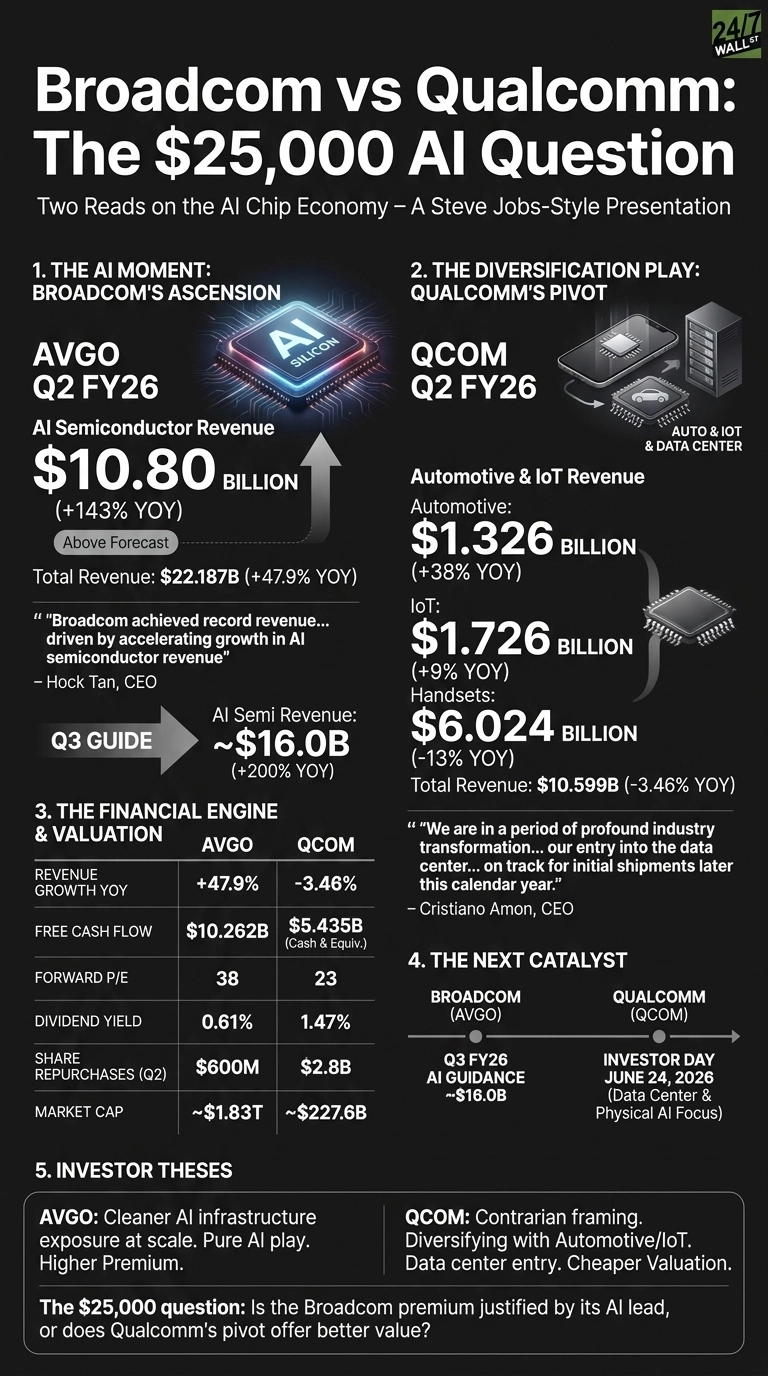

Broadcom’s Q2 FY26 revenue hit $22.187 billion, up 47.9% year over year, with AI semiconductor revenue alone at $10.80 billion, up 143%. That is a staggering mix shift toward custom accelerators and AI networking silicon for cloud giants.

CEO Hock Tan told investors the company expects AI semi revenue to grow “over 200 percent year-over-year to $16 billion” in Q3. Free cash flow of $10.262 billion shows the operating leverage is real.

Qualcomm’s quarter looked smaller and bumpier. Revenue of $10.59 billion slipped 3.46%, dragged down by handsets falling 13% to $6.024 billion on memory shortages and weak Chinese OEM demand.

Automotive hit a record $1.326 billion, up 38%, and licensing kept printing a 72% EBT margin. The bigger story sits in a single CEO line: a “leading hyperscaler custom silicon engagement is on track for initial shipments later this calendar year.”

| Business Driver | Broadcom | Qualcomm |

| Revenue growth YoY | +47.9% | -3.46% |

| Growth engine | Custom AI accelerators, networking | Automotive, IoT, licensing |

| Forward P/E | 38 | 23 |

| Dividend yield | 0.61% | 1.47% |

Entrenched Hyperscaler Supplier vs. New Entrant With a Mobile Cushion

Broadcom is already inside the AI buildout. Hock Tan’s team is shipping silicon to cloud titans today, and the $7.178 billion Infrastructure Software unit, anchored by VMware, throws off subscription cash to fund it. The risk is concentration. A few customers drive the AI line, and the stock’s 13.66% one-week drop after a strong print tells you how much air is in valuation.

Qualcomm is the cheaper, messier story. CEO Cristiano Amon framed the moment as “a period of profound industry transformation“, and a new $20 billion buyback plus $2.8 billion in Q2 repurchases signals conviction.

Snapdragon and Dragonwing still depend on a Chinese handset market that management expects to bottom in Q3 before recovering. Trading at roughly 23 times earnings against Broadcom’s 64, the gap is wide for a reason.

How Broadcom and Qualcomm Map to Different Investor Theses

I want to hear specifics at Qualcomm’s June 24 Investor Day, especially on data center economics and Physical AI. For Broadcom, I am keeping an eye on whether the $16 billion Q3 AI guide lands, and how much is concentrated in one or two hyperscalers.

Broadcom offers the cleaner AI infrastructure exposure at scale, with the post-earnings slide to $385.73 putting shares below last month’s levels.

Qualcomm fits a more contrarian framing. The stock has already run 45.62% since its April earnings report, and the June 24 Investor Day stands as the next major catalyst. Memory pricing trends into the fall remain a key variable for QCOM, while hyperscaler order book trajectory remains the central question for Broadcom.

Contact [email protected] for any questions or corrections.