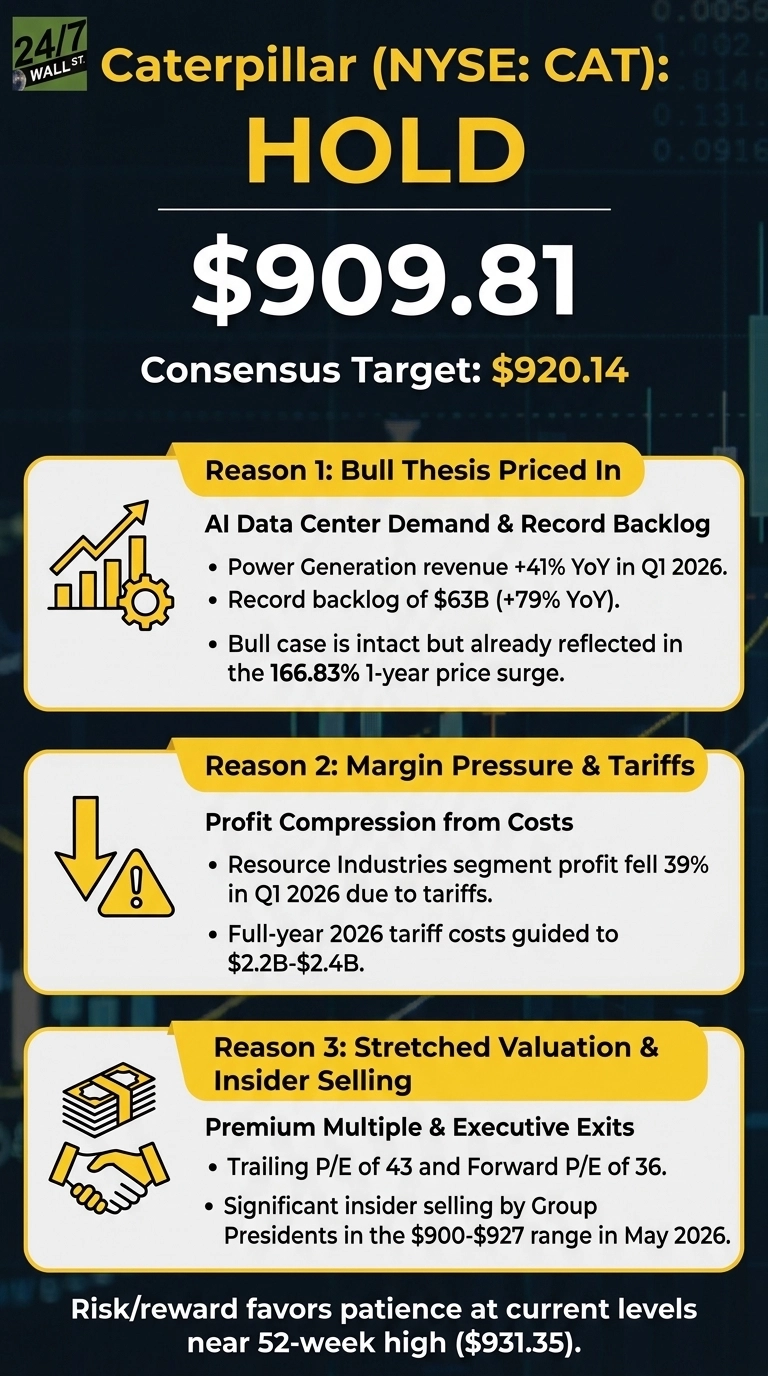

Caterpillar (NYSE:CAT | CAT Price Prediction) at $909.81 is a hold. The stock sits within striking distance of its $931.35 52-week high after a historic run, mixing a real AI-driven growth story with stretched valuation and visible insider selling.

Caterpillar is the world’s largest maker of construction and mining equipment, with a fast-growing Power & Energy arm that sells large reciprocating engines and turbines powering AI data centers. Power Generation revenue rose 41% year over year in Q1 2026 to $2.817 billion, and management is racing to expand capacity.

CAT is up 59.5% year to date and 166.83% over one year, compressing the margin of safety and putting the entry decision under scrutiny.

The Bull Case: Data Center Power With Record Backlog

Q1 2026 showed clean acceleration. EPS came in at $5.54 versus $4.64 expected, a 19.3% beat, on revenue of $17.41 billion that grew 22.2% year over year. Construction Industries grew 30% with segment margin expanding to 21.4%, ending rollover fears.

The bigger prize is power. Backlog hit a record $63 billion, up 79% year over year, and CEO Joe Creed said large reciprocating engine capacity will rise to nearly three times 2024 levels, roughly 15 gigawatts of annual capacity, with six data center agreements of at least one gigawatt each.

Industry research projects roughly 25% annual growth in data center equipment for years. BofA maintains a Buy and a $989 target; Argus is at $990.

The Bear Case: Tariff Drag, Insider Exits, Premium Multiple

Margins are the soft spot. Resource Industries profit fell 39% in Q1 2026, with segment margin down 700 basis points to 10%, largely tariff-driven. Management now guides $2.2 to $2.4 billion in full-year 2026 tariff costs, with about $700 million in Q2 alone. Full-year 2025 net income fell 17.68% even as revenue rose.

Valuation is rich for a cyclical. CAT trades at a trailing P/E of 43 and a forward P/E of 36, with 63 insider transactions skewing toward selling. Group Presidents Denise Johnson, Anthony Fassino, and Bob De Lange each disposed of large common-stock blocks in the $900 to $927 range in May.

The Hold Case: Right Story, Wrong Entry

Fundamentals support the move, but price has done most of the work. Consensus implies almost no upside, and the AI thesis hinges on hyperscaler capex staying near current levels through 2028.

A pullback to the 50-day average near $818 would reset risk/reward. A clean Supreme Court ruling on tariffs or Q2 results showing margin recovery alongside backlog growth would trigger adding. Until then, the risk/reward favors patience over fresh exposure.

The Numbers

At $909.81, CAT sits just below its $931.35 52-week high. The consensus 12-month target is $920.14, implying about 1.1% upside, and analyst targets are just one input among many.

- Strong Buy: 1

- Buy: 14

- Hold: 11

- Sell: 2

CAT has gained 59.5% year to date and 166.83% over the past year, dramatically outpacing the S&P 500, which posted only mid-single-digit returns year-to-date. EBITDA stands at $14.56 billion, with a 0.69% dividend yield and a 1.625 beta.

The Verdict

At $909.81, Caterpillar is a hold. The bull thesis is intact but already priced in. Consensus sees roughly 1% upside, and the stock trades at 36 times forward earnings while absorbing more than $2 billion in tariff costs this year. Buying near a 52-week high into a cyclical with compressing margins bets the next twelve months exceed an already raised bar.

A meaningful pullback toward the 50-day average, tariff resolution dropping to the guided range floor, and Q2 results confirming margin recovery would each tilt risk/reward back toward owners. Hyperscaler capex cuts, order cancellations inside the $63 billion backlog, or a step-down in Power Generation growth from the current 40%-plus pace would flip it to a Sell.

Existing holders may find the next quarter clarifies whether this is a $1,000 stock or a $750 stock, with position sizing a key consideration for those sitting on outsized gains. Patience costs little; chasing risks paying full price for a story the market has already discovered.

Contact [email protected] for any questions or corrections.