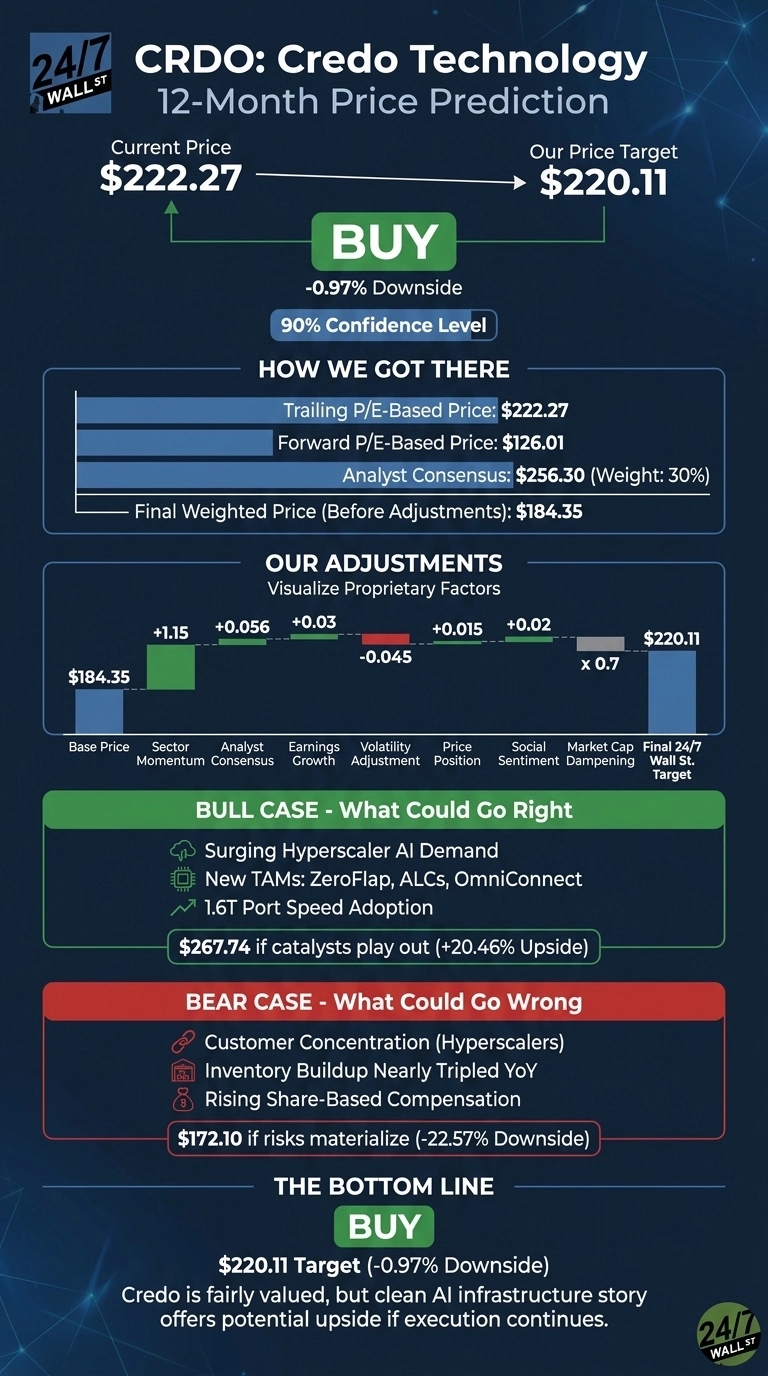

Credo Technology (NASDAQ:CRDO | CRDO Price Prediction) has tripled its revenue in a year, and the stock has followed. Our 24/7 Wall St. price target for Credo is $220.11, essentially flat against a current quote of $222.27. That implies a -0.97% move over the next 12 months, and the proprietary model carries a 90% confidence level. The recommendation is hold.

| Metric | Value |

|---|---|

| Current Price | $222.27 |

| 24/7 Wall St. Price Target | $220.11 |

| Upside/Downside | -0.97% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Our target sits a hair below the current quote, and Credo is one of the cleanest AI infrastructure stories in the market. Real upside could come from another guidance raise driven by 1.6T port adoption, or from the three new TAM categories Credo announced last quarter: ZeroFlap optics, Active Line Cards (ALCs), and OmniConnect. Treat the 24/7 Wall St. price target as one input, and read the bull case below carefully.

A Blowout Year Already Priced In

Credo has returned 204.65% over the past year and 54.47% year to date, trading roughly 4% below the 52-week high of $245.95.

The June 1 earnings report set the tone: Q4 FY2026 revenue of $437 million grew 157% YoY, and non-GAAP EPS of $1.16 beat the $1.03 consensus, the fourth straight EPS beat. Full-year revenue more than tripled to $1.34 billion.

The Case for $267 and Higher

The bull thesis lives in hyperscaler capex. CEO Bill Brennan said Credo’s vertically integrated approach helps customers “accelerate cluster time-to-stability, maximize GPU utilization, improve network reliability, and reduce overall infrastructure power and operating costs.”

Q1 FY2027 guidance of $465M to $475M implies sequential growth continues. The consensus analyst target is $256.30, with 17 buy or strong-buy ratings out of 18 analysts covering the name. Our internal bull scenario projects $267.74 in 12 months, a 20.46% return.

The Risks Worth Watching

Credo trades at a trailing P/E of 122 and a forward P/E near 35. Customer concentration in hyperscalers, inventory that nearly tripled YoY, and rising share-based compensation are real exposures. A beta of 3.229 means any AI capex pause hits hard.

Bears would point to our bear case at $172.10, a -22.57% outcome. The counterfactual: that inventory build often signals customers ramping next-generation deployments, and R&D that nearly doubled YoY to $90.53M funds the next TAM expansion.

Credo Price Prediction 2026-2030

The 24/7 Wall St. price target of $220.11 says Credo is fairly valued today at 90% confidence. The setup to watch: if Q1 FY2027 results come in above the high end of guidance and material contribution from ZeroFlap or OmniConnect would strengthen the bull case. Softer hyperscaler capex commentary or gross margin compression below the guided 67% to 69% band would weaken it.

Looking further ahead, here is where our model projects Credo could trade, assuming current growth trajectories hold and AI infrastructure spending remains durable.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $220.11 |

| 2027 | $213.62 |

| 2028 | $229.94 |

| 2029 | $241.91 |

| 2030 | $245.00 |

These projections assume Credo continues converting hyperscaler relationships into new TAM categories. Significant upside or downside could result from AI capex cycles or a shift in port-speed adoption.

Contact [email protected] for any questions or corrections.