I am opening with the verdict because the setup matters. Credo Technology (NASDAQ:CRDO | CRDO Price Prediction) has staged one of the most explosive rallies in the AI infrastructure complex, but our proprietary model suggests the run has gotten ahead of fundamentals.

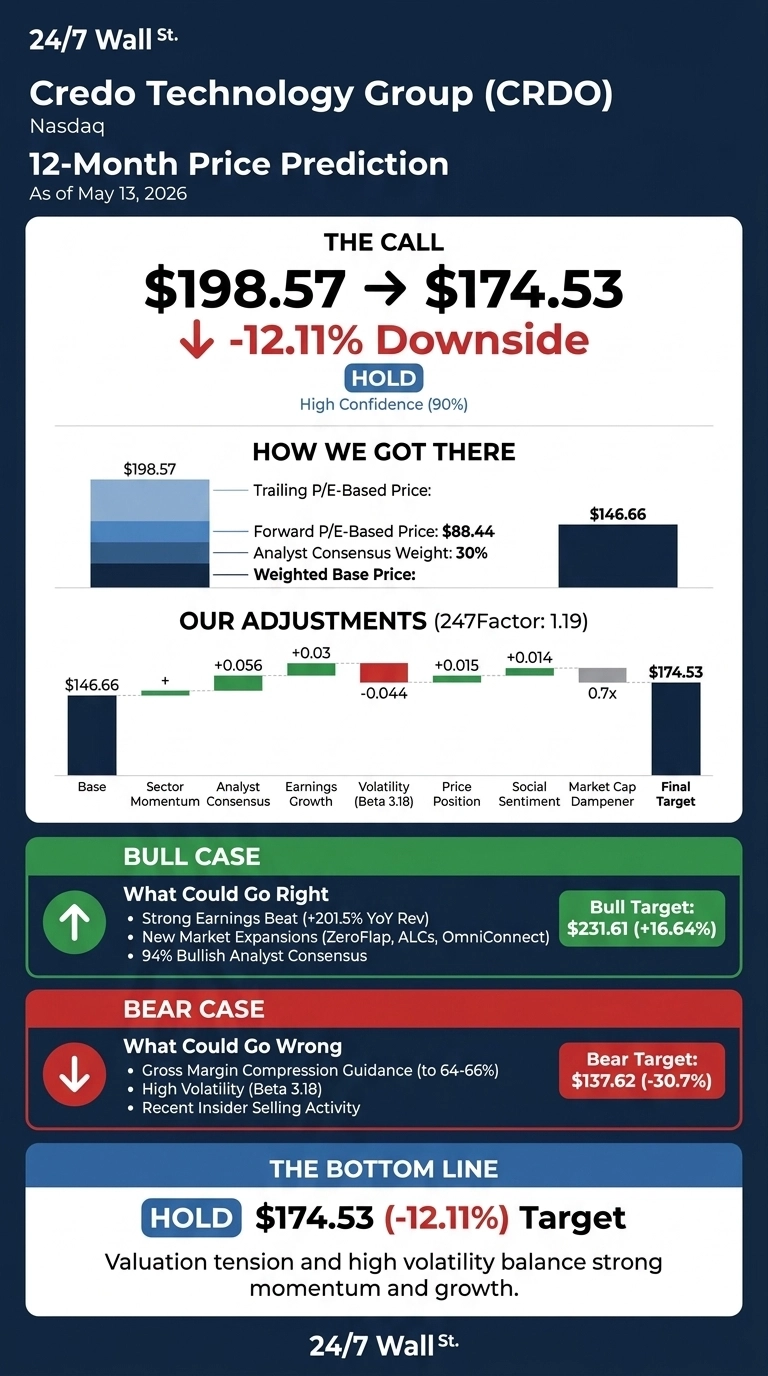

Our 24/7 Wall St. price target for Credo is $174.53, against a current price of $198.57. That implies -12.11% downside over the next 12 months, and we rate the stock a hold with high confidence at 90%.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $198.57 |

| 24/7 Wall St. Price Target | $174.53 |

| Upside/Downside | -12.11% |

| Recommendation | HOLD |

| Confidence Level | 90% |

Why We Could Be Wrong

Credo is one of the most divisive names in the AI connectivity trade, and our 24/7 Wall St. price target of $174.53 sits below where shares trade today. Real upside could come from accelerating adoption of ZeroFlap optics, Active Line Cards, and OmniConnect memory solutions, or from a second hyperscaler design win that re-rates forward estimates. Treat our target as one datapoint among many. A full bull case appears below.

A 260% Year and a Blowout Quarter

Credo is up 259.53% over the past year, 66.04% in the last month alone, and 38% year to date. Shares trade 2% below the 52-week high of $213.80 and well above the $57.21 low.

The Q3 FY2026 report delivered revenue of $407.01 million, up 201.5% year over year, with non-GAAP EPS of $1.07 beating consensus by 13.75%. Reddit sentiment turned very bullish around April 22, coinciding with the latest leg higher.

The Case for $230+

Bulls have a credible playbook. Wall Street’s consensus price target sits at $209.09, with 4 strong buys and 12 buys against a single hold. Credo announced three new multi-billion-dollar TAM expansions in ZeroFlap optics, Active Line Cards, and OmniConnect, alongside a fresh collaboration with AI cloud provider TensorWave.

CEO Bill Brennan said the company is delivering “record results with revenue of $407.0 million, an increase of more than 50% sequentially and 200% year over year.” Q4 guidance of $425 million to $435 million implies continued acceleration. Our bull case price target stretches to $231.61, a 16.64% gain.

The Risks Worth Watching

Valuation is the loudest concern. Credo trades at a trailing P/E of 115 and a forward P/E of 38, with implied multiples near 91x on current EPS. Q4 guidance points to non-GAAP gross margin compression to 64% to 66% from 68.6% in Q3, while inventory ballooned to $207.9 million.

Insider activity has been heavy, with executives including the CTO and CEO disposing of shares at prices ranging up to $190.50. That said, bulls would argue the inventory build reflects positioning for the Q4 revenue ramp, and most insider sales appear tied to scheduled 10b5-1 plans rather than a thesis change. Our bear case lands at $137.62, a 30.7% drawdown.

Hold for Now

Our price target is $174.53 with a hold rating and 90% confidence. The tipping factor is valuation: at 38x forward earnings on a stock with beta of 3.18, near-term reward looks asymmetric. The key variables to watch are whether Credo prints another quarter materially above the $435 million high end of guide with gross margins holding above 66%, or whether Q4 margins compress as guided and hyperscaler order patterns turn lumpy.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $174.53 |

| 2030 | $170.17 |

These projections assume Credo continues executing on its AEC and optics roadmap while navigating gradual multiple compression. Significant upside or downside could result from a major hyperscaler design loss or, conversely, faster ramps on ZeroFlap optics and OmniConnect.

Contact [email protected] for any questions or corrections.