After a 89% year-to-date rally that has taken shares from $143.89 to $271.95, Credo Technology Group (NASDAQ: CRDO | CRDO Price Prediction) has become one of the most talked-about AI infrastructure plays on the market.

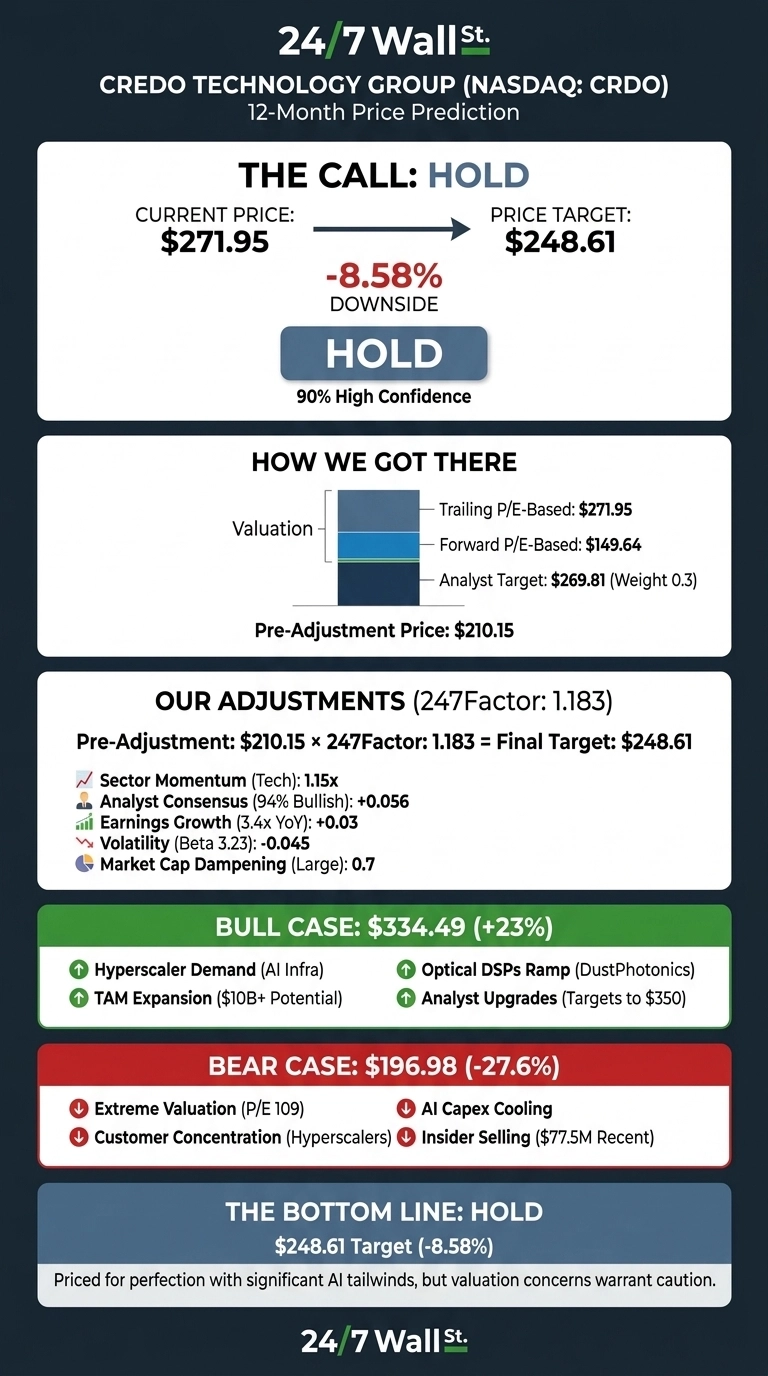

Our 24/7 Wall St. price target for Credo is $248.61, implying -8.58% downside over the next 12 months. Our recommendation is hold, with a high 90% confidence level.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $271.95 |

| 24/7 Wall St. Price Target | $248.61 |

| Upside/Downside | -8.58% |

| Recommendation | HOLD |

| Confidence Level | 90% |

A Note Before We Begin

Our 24/7 Wall St. price target of $248.61 sits modestly below where Credo trades today. Credo is one of the purest AI connectivity plays in the market, and real upside could come from the recently announced ZeroFlap optics ramp or the DustPhotonics acquisition unlocking silicon photonics revenue. Treat our target as one datapoint among many. A detailed bull case follows.

The Rally Behind a 193% One-Year Gain

Credo is up 15.22% over the past month and 193.71% over the past year, sitting 13% below its 52-week high of $308.67. The most recent surge came on June 30, when shares jumped 10.69% following Credo’s reclassification from the Russell 2000 into the Russell 1000 and Russell Midcap indices.

Fundamentally, the story is loud. Q4 FY2026 revenue landed at $437 million, up 157.0% year over year, and non-GAAP EPS of $1.16 beat consensus by 12.17%, marking four consecutive quarters of EPS beats. Full-year revenue more than tripled to $1.34 billion.

Why Bulls See a Breakout Ahead

The bull case rests on TAM. BNP Paribas initiated coverage with a $275 target, arguing Credo’s addressable market could exceed $10 billion with 5 of 6 hyperscalers already customers. Evercore ISI initiated Outperform at $325, citing optical DSPs via DustPhotonics.

Stifel reiterated Buy and raised its target to $350 from $250. CEO Bill Brennan noted, “Fiscal 2026 marked another defining year for Credo. For the year, revenue more than tripled to $1.3 billion, and non-GAAP net income increased more than five times to $662 million.” Our bull-case 1-year target is $334.49.

The Risks Worth Watching

Credo trades at a trailing P/E of 109 and a forward P/E of 42. Simply Wall St pegs fair value at $130, implying the stock is roughly 100% above intrinsic value.

Insider selling reached $77.5 million in the recent period, though bulls fairly note these sales occurred under pre-arranged Rule 10b5-1 trading plans and reflect tax obligations rather than conviction changes. Customer concentration among hyperscalers remains a real risk if AI capex cools. Our bear-case 1-year target is $196.98.

Hold for Now, Watch for a Pullback

Our 24/7 Wall St. price target remains $248.61 with a hold recommendation and 90% confidence. The scale tipper is valuation: at an implied P/E near 80, Credo is priced for flawless execution.

A pullback into the low $200s with hyperscaler AEC bookings intact would improve the risk/reward. Conversely, slipping optical DSP ramps or softer hyperscale capex guidance into calendar 2027 would weaken the setup.

Looking further out, here is where our model projects Credo could trade, assuming current AI infrastructure growth trajectories hold.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $248.61 |

| 2027 | $268.00 |

| 2028 | $285.00 |

| 2029 | $305.00 |

| 2030 | $254.00 |

These projections assume Credo continues executing on its 1.6T connectivity roadmap and successfully integrates optical acquisitions. Significant upside could result from broader hyperscaler adoption; significant downside could follow an AI capex slowdown.

Contact [email protected] for any questions or corrections.