I’m initiating coverage on Credo Technology (NASDAQ:CRDO | CRDO Price Prediction) after one of the wildest weeks in the AI connectivity trade. Shares fell 25.66% over the past five sessions, yet the stock is still up 159.89% over the past year. With Q3 FY2026 revenue growing 201.5% YoY and three new multi-billion-dollar TAM expansions on the table, the question is whether the recent selloff is a gift or a warning. Our model points to a modest reset.

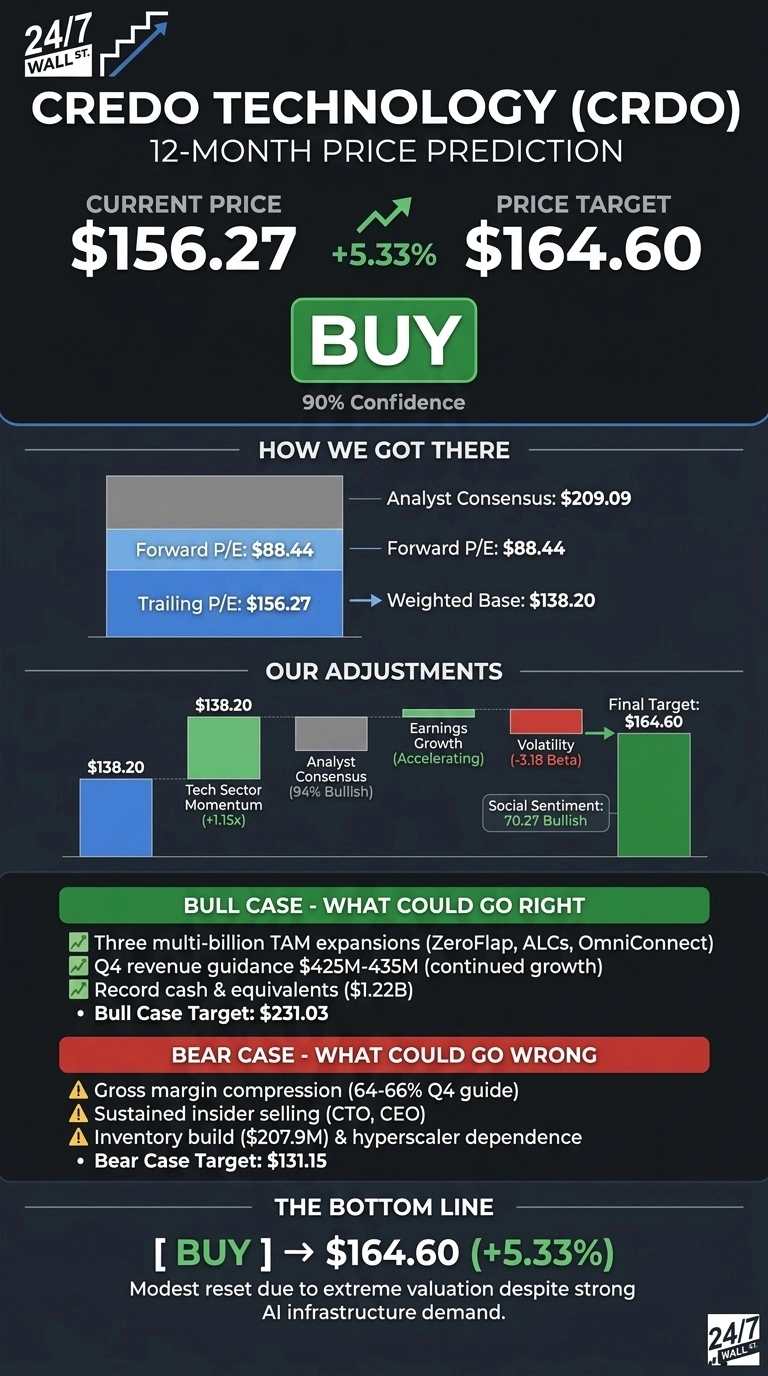

Our 24/7 Wall St. price target for Credo is $164.60, implying 5.33% upside from the current $156.27. The recommendation is buy with high confidence of 90%, reflecting strong analyst alignment and durable AI infrastructure demand offset by extreme valuation.

| Metric | Value |

|---|---|

| Current Price | $156.27 |

| 24/7 Wall St. Price Target | $164.60 |

| Upside | 5.33% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Week After a Stellar Earnings Report

Credo’s most recent trading day delivered a 9.24% drop, retreating from a 52-week high of $213.80 to $156.27. YTD, shares are still up 8.60%. The Q3 FY2026 report on March 2, 2026 was a blowout: revenue of $407.01 million beat the $387.62 million consensus, non-GAAP EPS of $1.07 against $0.94, and non-GAAP operating margin of 49.6%.

What spooked traders was the Q4 guide. Management projected non-GAAP gross margin of 64% to 66%, compression from Q3’s 68.6%. Inventory swelled to $207.9 million, and insider activity skewed heavily to sales, with CTO Chi Fung Cheng leading disposals through spring.

The Case for $230 and Higher

Bulls have plenty to point to. The analyst panel includes 4 Strong Buy and 12 Buy ratings against just 1 Hold, with a consensus target of $209.09. Our bull case scenario puts shares at $231.03 over the next 12 months, a 47.84% return.

The growth narrative is real. CEO Bill Brennan flagged “three new multi-billion dollar TAM expansions through ZeroFlap optics, ALCs, and OmniConnect”, layering optionality on top of Active Electrical Cables that already drive hyperscaler revenue. Q4 revenue guidance of $425 to $435 million implies continued sequential growth, and the balance sheet holds $1.22 billion in cash.

What Could Go Wrong

The bear case lands at $131.15, a 16.07% drop. CRDO trades at a P/E of 94x and a P/S of 30x. Any slip in hyperscaler capex would compress the multiple violently given the 3.18 beta.

Sustained insider selling adds friction. CTO Cheng disposed of shares across March and April, and CEO Brennan unloaded roughly 59,836 shares on March 11. Bulls argue the cadence and identical pricing across executives on April 2 and April 5 point to scheduled 10b5-1 trading plans rather than conviction selling.

The inventory build to $207.9 million could reflect supply-chain positioning for booked demand rather than softness, and the gross margin guide reflects mix shift into newer products that should normalize as volumes scale.

Credo Price Prediction 2026-2030

The 24/7 Wall St. price target is $164.60, the recommendation is buy, and confidence is 90%. The factor tipping the scale is the gap between the forward P/E-implied price of $88.44 and the analyst target of $209.09.

That spread suggests consensus expects the AI cycle to fund Credo’s earnings ramp longer than a textbook multiple would suggest. I’d be a buyer here if Q4 lands inside guidance and margin compression stops at 64%. I’d stay on the sidelines if hyperscaler capex commentary cools or inventory keeps climbing without matching revenue.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $164.60 |

| 2027 | $170.59 |

| 2028 | $180.00 |

| 2029 | $190.35 |

| 2030 | $200.90 |

These projections assume Credo converts its AEC, optics, and OmniConnect roadmap into revenue and hyperscaler AI spend remains intact. Significant upside or downside could result from a meaningful shift in the AI capex cycle or new ASIC entrants competing in high-speed connectivity.

Contact [email protected] for any questions or corrections.