Pfizer (NYSE:PFE | PFE Price Prediction) trades at $25.62, pays a 6.7% dividend yield, and just posted five straight quarterly EPS beats before stumbling in Q1. Yet the stock is up only 6.37% YTD this year. Can Pfizer shares double to $50 by 2031?

What’s Holding Pfizer Back

Pfizer is down 0.23% over the past month and essentially flat over the past week. Over five years, holders face a 16.77% loss.

The COVID cliff is the culprit. Comirnaty revenue fell 59% in Q1 2026 and Paxlovid dropped 63%, masking strong growth elsewhere. Add the $1.5 billion generic and biosimilar headwind expected this year, plus Barclays maintaining a Sell rating with a $25 price target, and the market refuses to re-rate the stock. With a beta of just 0.295, Pfizer needs proof, not hope.

Wall Street Sees 14% Upside. The Real Number Is Bigger

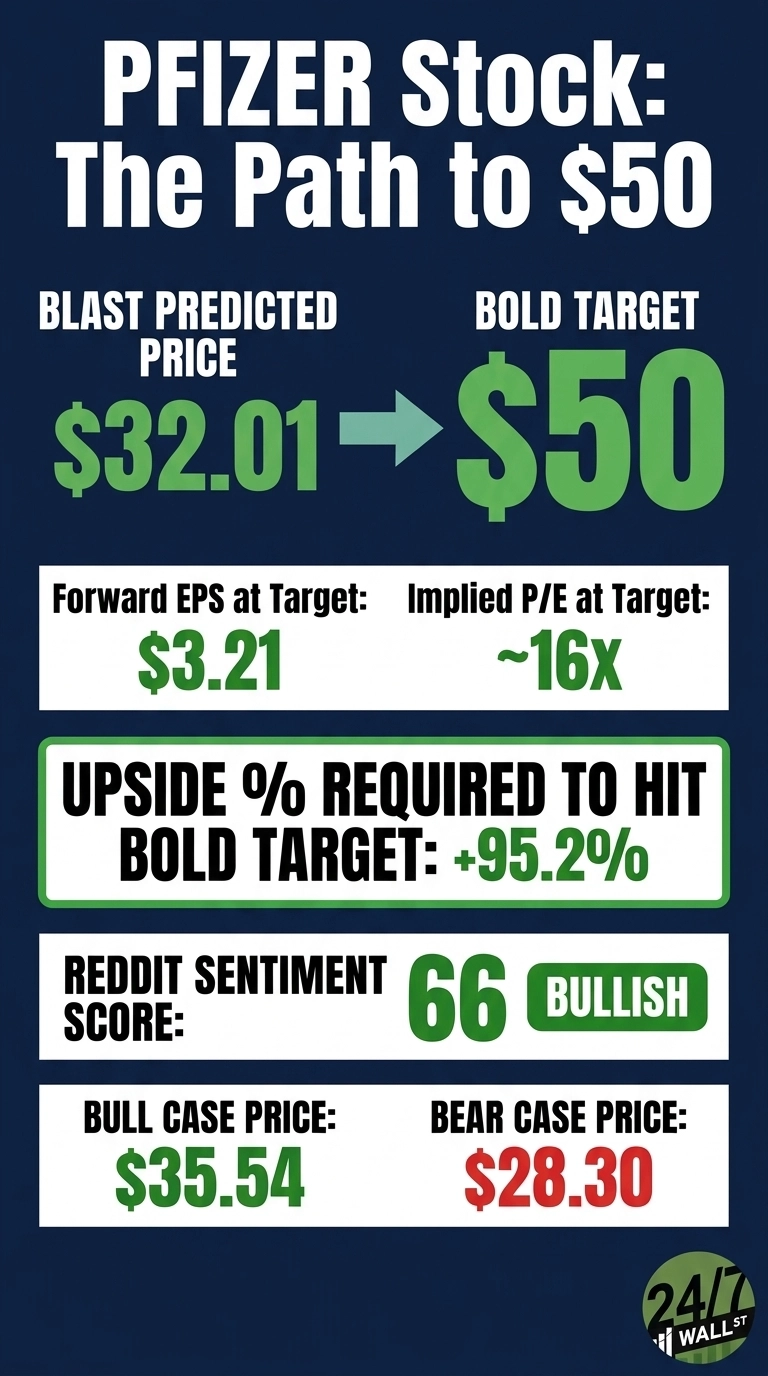

The consensus target sits at $29.19, with 2 Strong Buys, 9 Buys, 15 Holds, 1 Sell, and 2 Strong Sells. That works out to a 38% bullish camp, missing the obesity and oncology pipeline.

My model points to $32.01 in 12 months, roughly 24.95% upside, with a bull case at $35.54 and a bear case at $28.30. Confidence on that base case is high. The Street has not priced in the pipeline’s potential and will play catch-up by 2027.

The Path to $50

Reaching $50 from today’s price of $25.62 requires a gain of 95.2%. With forward EPS of $3.21, a price of $50 implies a forward P/E of roughly 16x. My base case of $32.01 already embeds 8x, meaning the target needs about 7x of multiple expansion.

That sounds aggressive until you examine what is brewing. Berobenatide, Pfizer’s monthly GLP-1, posted 15.9% weight loss at 32 weeks with no plateau, with 10 Phase 3 studies planned this year.

HYMPAVZI won expanded FDA approval for pediatric hemophilia patients. The Lyme disease vaccine showed 73.2% efficacy in Phase 3. Jefferies reaffirmed a Buy rating with a $35 target.

CEO Albert Bourla said on the Q1 call: “I’m particularly encouraged by what we’re seeing in oncology and obesity, two areas where I believe Pfizer is positioned to lead.” A successful obesity launch could re-rate this stock toward Eli Lilly (NYSE:LLY) territory. The biggest risk is patent cliff erosion outpacing new launch revenue.

Valuation vs. Earnings Power

At $25.62, Pfizer trades at roughly 8x forward earnings against guidance of $2.80 to $3 in adjusted EPS for 2026. Shares sit between a 52-week high of $28.28 and a low of $21.97. Ten-year total return is just 19.62%, brutal for a Dow component. That low multiple is the entire bull case. Re-rating a single-digit P/E stock paying a near 7% yield just takes the pipeline working.

Is $50 Realistic?

$50 by 2031 requires a 95.2% gain. My five-year base case lands at $49.39, with a bull case of $55.47.

Three things must go right: Berobenatide must deliver in Phase 3 and commercialize cleanly. The oncology franchise (Padcev, Lorbrena, Talzenna) must keep compounding. Management must defend Vyndamax through the 2031 patent extension without margin damage. A Most-Favored-Nation pricing regime that caps US drug economics would derail it. We’ve outlined the blueprint for how Pfizer could reach $50 in 2031.