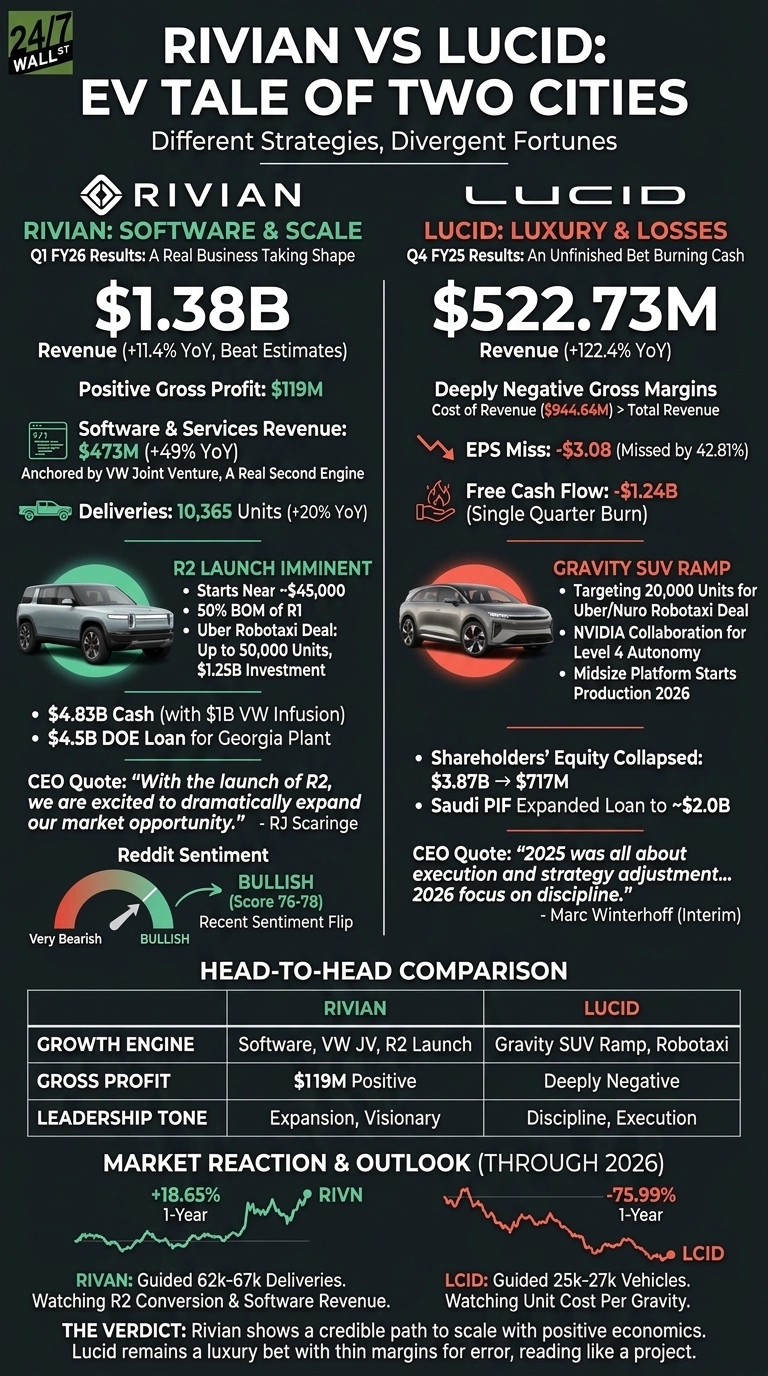

Rivian (NASDAQ:RIVN | RIVN Price Prediction) and Lucid (NASDAQ:LCID) just gave us two very different EV stories. Rivian’s Q1 FY26 showed a real business taking shape, with software pulling weight while the R2 launch begins. Lucid’s Q4 FY25 revealed an unfinished luxury bet still burning cash faster than it can sell cars.

Software Saves Rivian. Luxury Still Costs Lucid

Rivian delivered 10,365 vehicles last quarter, a 20% YoY gain, and posted $1.381 billion in revenue. The story underneath matters more. Automotive revenue slipped 2% YoY to $908 million as regulatory credits fell by $100 million, yet Software and Services grew 49% to $473 million, fueled by the Volkswagen joint venture. That is a real second engine.

Lucid sold 5,345 vehicles and grew revenue 122.39% YoY to $522.73 million, but cost of revenue hit $944.64 million. Building a Lucid Air or Gravity still costs nearly twice what it earns. The EPS loss of -$3.08 missed estimates by 42.81%, and free cash flow was -$1.24 billion in a single quarter. Shareholders’ equity collapsed from $3.87 billion to $717 million over the year.

Mass Market Truck Maker vs. Luxury Holdout

CEO RJ Scaringe framed the moment plainly: “With the launch of R2, we are excited to dramatically expand our market opportunity and have more people driving Rivians.” The R2 starts near $45,000 with a bill of materials around 50% of R1, and Uber committed up to $1.25 billion for as many as 50,000 robotaxi R2s. A $4.5 billion DOE loan backs the Georgia plant.

Lucid’s interim CEO Marc Winterhoff took a humbler tone: “2025 was all about execution and strategy adjustment to set Lucid up for long-term success.” The Midsize platform begins production this year, the NVIDIA and Uber/Nuro robotaxi deal targets 20,000 Gravity units, and Saudi PIF expanded its facility to roughly $2 billion. Useful lifelines, but the unit economics need to change.

| Business Driver | Rivian | Lucid |

| Growth Engine | Software, VW JV | Gravity SUV ramp |

| Gross Profit | $119M positive | Deeply negative |

| Tone From the Top | Expansion | Discipline |

What I’m Watching Through 2026

Rivian guided to 62,000 to 67,000 deliveries with adjusted EBITDA between -$2.10 billion and -$1.80 billion. I want to see R2 conversion from R1 shoppers and whether the VW software stream keeps compounding.

Lucid targets 25,000 to 27,000 vehicles, and I am watching unit cost per Gravity above all else. Reddit sentiment captured the divergence neatly, with RIVN flipping from very bearish to bullish 76 to 78.

Why I Lean Toward Rivian Today

If you want a credible path to scale, Rivian fits me better right now. Positive consolidated gross profit, $4.83 billion in cash, and a mass-market product entering showrooms beats a story still searching for unit economics.

Lucid could reward a patient turnaround investor if Midsize lands and robotaxis deploy on time, but with shares down 75.99% over a year and a Polymarket bankruptcy odds line still at 4%, the margin for error is thin. I would change my view on Lucid the moment cost of revenue dips below revenue. Until then, Rivian’s quarter reads like a company. Lucid’s reads like a project.

Contact [email protected] for any questions or corrections.