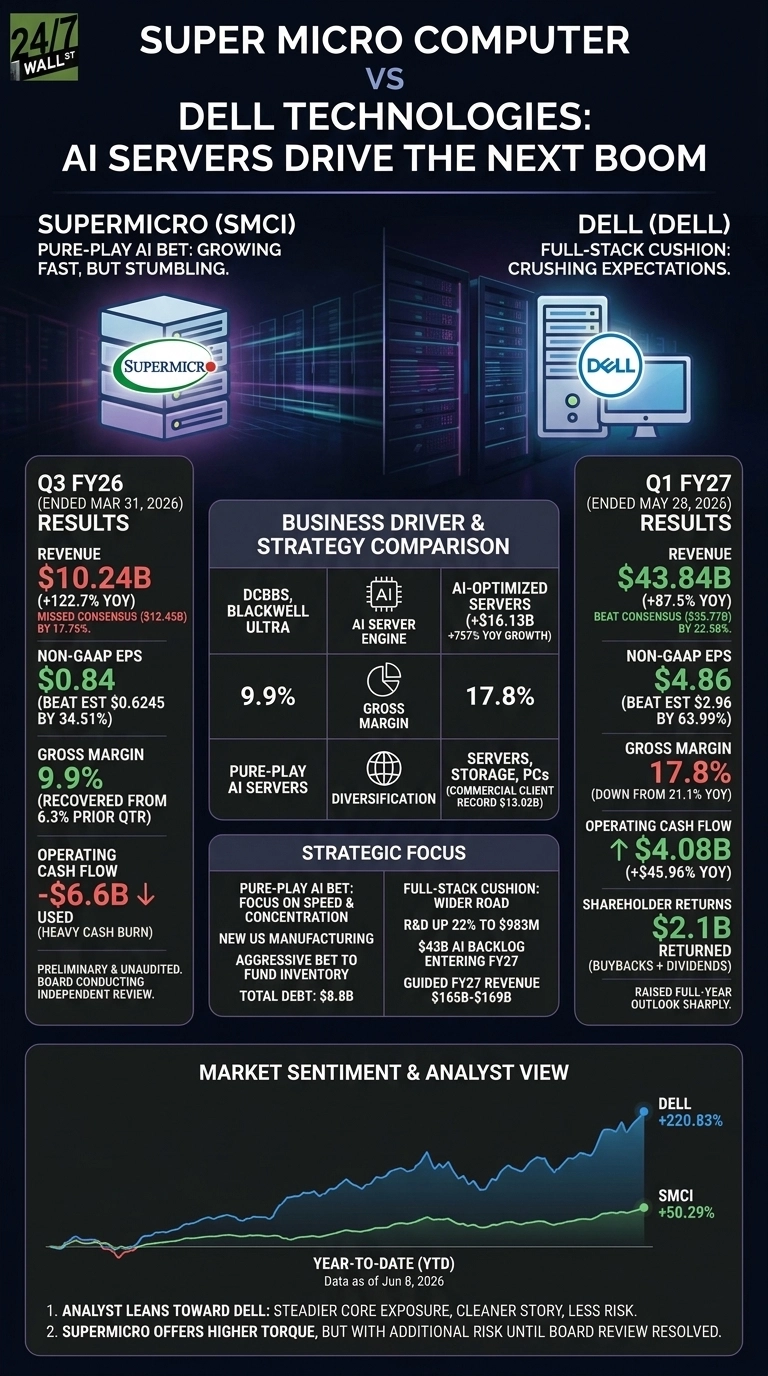

Super Micro Computer (NASDAQ: SMCI | SMCI Price Prediction) and Dell Technologies (NYSE: DELL) just reported quarters that tell opposite stories about the AI server boom.

Dell crushed expectations with $43.84 billion in Q1 FY27 revenue and raised its full-year outlook sharply. Supermicro grew fast but missed consensus expectations while a board review hangs overhead. Two AI server leaders, two very different quarters.

Dell Lands the Bigger Punch. Supermicro Stumbles on the Top Line.

Dell’s Infrastructure Solutions Group did the heavy lifting. ISG hit $29.01 billion (+181% YoY), with AI-Optimized Servers alone at $16.13 billion (+757% YoY). That growth rate is not a typo, and it reflects a deep enterprise channel translating GPU orders into shipments. Commercial PCs added a quieter $13.02 billion record, the kind of ballast Supermicro simply does not have.

Supermicro’s Q3 FY26 told a messier tale. Revenue of $10.24 billion grew 122.7% YoY but fell short of the $12.45 billion the Street wanted.

Non-GAAP EPS of $0.84 beat expectations, and gross margin recovered to 9.9% from 6.3%. CEO Charles Liang framed it as progress: “Supermicro’s transformation into a total datacenter infrastructure provider is accelerating.” The catch: results are preliminary and unaudited, with an independent board review tied to export-control matters.

| Business Driver | Supermicro | Dell |

| AI server engine | DCBBS, Blackwell Ultra systems | AI-Optimized Servers (+757% YoY) |

| Gross margin | 9.9% | 17.8% |

| Diversification | Pure-play AI servers | Servers, storage, PCs |

Pure-Play AI Bet vs. Full-Stack Cushion

Supermicro is doubling down on one thing: building the densest, fastest liquid-cooled AI racks money can buy. New Silicon Valley manufacturing, a Taiwan footprint, and Netherlands capacity all feed the DCBBS model. The reward is speed. The cost is concentration.

Operating cash flow ran negative $6.6 billion in the quarter, and total bank debt and convertibles sit at $8.8 billion. That is an aggressive bet to fund inventory for hyperscale orders.

Dell takes the wider road. R&D rose 22% YoY to $983 million, AI orders booked in the quarter hit $24.4 billion, and management returned $2.1 billion through buybacks and dividends.

Full-year guidance moved up to $165 billion to $169 billion, with AI servers alone guided to roughly $60 billion (+144% YoY). Negative book value of -$1.4 billion is the asterisk, though strong cash generation softens that concern.

What I Want to See Next

For Supermicro, the export-control review needs resolution. Until then, every number carries a footnote. I will be watching whether margin recovery sticks above 10% as Blackwell Ultra shipments scale and whether the cash burn reverses once inventory clears.

Dell’s path is simpler: keep converting that $43 billion AI backlog without further margin slippage. Q2 guidance of $44 billion to $45 billion already implies a 49% jump, so execution risk is real.

Why I Lean Toward Dell Right Now

If you want clean exposure to the AI server cycle, I lean Dell. The full-stack model, the cash returns, and a guidance raise of that magnitude make the story easier to underwrite.

Supermicro is more interesting if you want torque. Reddit sentiment hit 82, very bullish, on May 20, and SMCI is up 50.29% year to date. Dell, meanwhile, has run 220.83% YTD, so the easy money is already in the rearview. For investors weighing the two, Dell offers the steadier core exposure, while Supermicro carries higher torque and additional risk until the board review closes cleanly.

Contact [email protected] for any questions or corrections.