Super Micro Computer (NASDAQ:SMCI | SMCI Price Prediction) has whipsawed investors over the past year, with the stock down 32.03% over twelve months even as AI server demand has exploded.

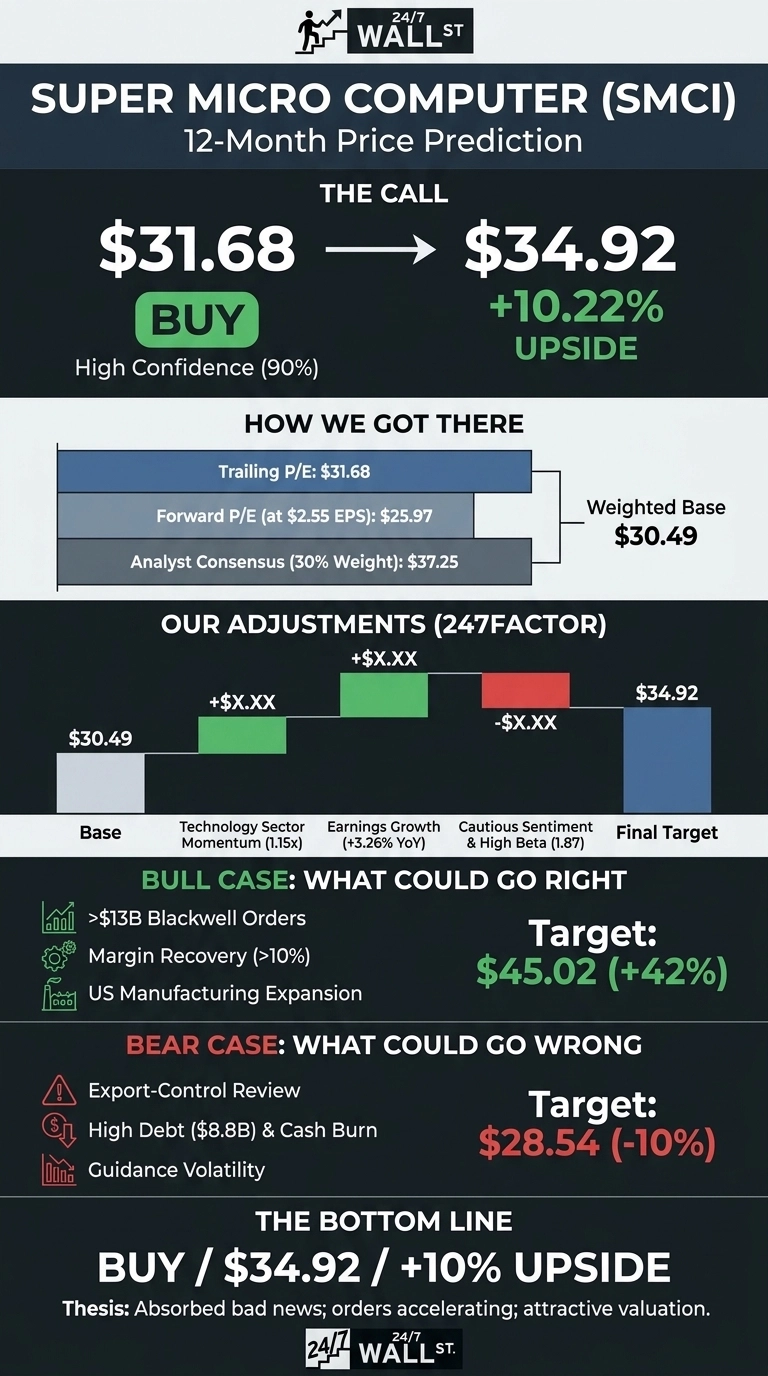

After a brutal repricing, our model now sees value emerging at current levels. Our 24/7 Wall St. price target for Super Micro is $34.92, implying roughly 10.22% upside from $31.68. We rate SMCI a buy with high confidence.

24/7 Wall St. Price Target Summary

| Metric | Value |

|---|---|

| Current Price | $31.68 |

| 24/7 Wall St. Price Target | $34.92 |

| Upside | 10.22% |

| Recommendation | BUY |

| Confidence Level | 90% |

A Brutal Year Sets a New Baseline

SMCI has been one of the most volatile names in AI infrastructure. The stock sits 40% off its 52-week high of $62.36, with a 52-week low of $19.48 in the rearview. Year to date, shares have eked out a 8.23% gain, though the past month is down 14.61% after a $7 billion equity and equity-linked financing announcement on June 10 hammered sentiment.

Fundamentals tell a more constructive story. Q3 FY26 revenue hit $10.24 billion, up 122.7% year over year, and non-GAAP EPS of $0.84 beat consensus by 34.51%. GAAP gross margin recovered to 9.9% from 6.3% the prior quarter. Management guided FY26 revenue to $38.9 billion to $40.4 billion.

Why Bulls See a Breakout Ahead

The bull case starts with the order book. CEO Charles Liang flagged more than $13 billion in Blackwell Ultra orders and is scaling Datacenter Building Block Solutions across new Silicon Valley manufacturing capacity. If margin recovery sustains and FY26 lands at the high end of the $40.4 billion guide, the forward multiple compresses meaningfully.

Liang said “Supermicro’s transformation into a total datacenter infrastructure provider is accelerating.” Our bull scenario puts shares at $45.02 within twelve months, a 42.12% return. Analysts at the high end still see $37.25 consensus with 5 buy ratings.

The Risks Worth Watching

The bear case is real. SMCI carries $8.8 billion in bank debt and convertibles, used $6.6 billion in operating cash in Q3, and cash has fallen to $1.29 billion. Results remain preliminary and unaudited pending an independent board review of export-control matters.

Bulls would counter that the working capital draw funded inventory for the Blackwell ramp, and the $7 billion equity raise directly addresses balance sheet concerns. 3 sell ratings reflect skepticism. Our bear scenario lands at $28.54, a 9.9% decline.

SMCI Price Prediction 2026-2030

The 24/7 Wall St. price target of $34.92 reflects a stock that has already absorbed a year of bad news while orders accelerate. With a forward P/E near 10x and AI server demand intact, I rate SMCI a buy with 90% confidence. Our conviction strengthens if Q4 confirms gross margins stabilizing above 10%, and weakens if the export-control review escalates or guidance is cut again.

| Year | 24/7 Wall St. Price Target |

|---|---|

| 2026 | $32.49 |

| 2027 | $34.92 |

| 2028 | $37.95 |

| 2029 | $41.20 |

| 2030 | $44.10 |

These projections assume Super Micro continues executing on DCBBS adoption and Blackwell Ultra fulfillment. Meaningful upside or downside could come from the resolution of the export-control review and the pace of hyperscaler capex.

Contact [email protected] for any questions or corrections.