From Defense Contractor Curiosity to AI Poster Child

When Palantir (NASDAQ:PLTR | PLTR Price Prediction) went public via direct listing on September 30, 2020, most investors saw a slow-growth government data shop with messy stock-based comp. Gotham powered defense and intel work, Foundry served a handful of commercial clients, and the stock drifted for years with an “overhyped” label glued to it.

Then 2023 happened. The launch of AIP (Artificial Intelligence Platform) plugged Palantir straight into the generative AI gold rush. The stock joined the S&P 500 in September 2024, CEO Alex Karp became the loudest voice in enterprise AI, and the commercial book exploded. Q4 2025 revenue grew 70% year over year, U.S. commercial revenue surged 137%, and the Rule of 40 score hit 127. Karp’s verdict on the call: “We are an n of one category of our own.”

What $1,000 at IPO Actually Became

Palantir has only traded since 2020, so a true 10-year window does not exist. Here is how $1,000 held up across the periods that do.

Since IPO (September 30, 2020)

- Initial Investment: $1,000

- Current Value: $14,266

- Total Return: 1,326.63%

- S&P 500 (same period): $2,377 (137.65%)

5-Year Return

- Initial Investment: $1,000

- Current Value: $5,640

- Total Return: 464%

- S&P 500 (same period): $1,745 (74.53%)

1-Year Return

- Initial Investment: $1,000

- Current Value: $1,130

- Total Return: 13.03%

- S&P 500 (same period): $1,244 (24.37%)

Almost the entire return came in a narrow window. Shares hugged the IPO reference price for years before AIP and index inclusion drove the rerating. Holding through those drawdowns took real conviction, and the recent action is a reminder of how violent the swings can be. PLTR is down 23.75% year to date and lost 13.42% in the past week alone. On a 1-year basis, it now trails the S&P 500.

I’d Buy Here, But Only on My Terms

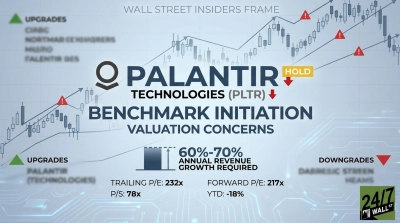

I’d put $1,000 into Palantir today if I believe U.S. commercial growth holds near management’s guided 61% FY 2026 revenue target and AIP keeps cementing customer lock-in. The underlying math is striking: a 46.2% operating margin, $5.22 billion in trailing revenue, and an analyst target of $183.73 against today’s $135.53.

I’d avoid it if valuation rattles me, which it sometimes does. A 152x trailing P/E and 97x forward earnings price in near-flawless execution. Michael Burry’s recent “sand castle” critique gained traction on Reddit for a reason, and Polymarket traders now pin an 84% probability on shares touching $132 this month.

I’d nibble with $1,000 rather than size it as a core position. The story is real, the math is demanding, and any deceleration in commercial growth could compress this multiple in a hurry.

Contact [email protected] for any questions or corrections.